Actinium Offers Shareholders Several Interesting Near-Term Catalysts

TM editors' note: This article discusses a penny stock and/or microcap. Such stocks are easily manipulated; do your own careful due diligence.

Shares of Actinium Pharmaceuticals (ATNM) have performed nicely over the past month, driven by the achievement of several milestones, including the hiring of a new Chief Medical Officer and initiation of a new clinical trial with Actimab-M for multiple ATNMmyeloma. The company is executing well, and the upswing is likely to continue given the strong cash balance and incredible value at this level, along with several important catalysts on the near-term horizon. Cash and Catalysts, along with Credibility, are part of my 5 C's of Biotech Investing™.

In the article below, I take a look at some pending catalysts for Actinium in 2017.

Actimab-M Enters The Clinic

Earlier in February 2017, Actinium announced an exciting expansion of the pipeline by moving Actimab-M into a in Phase 1 proof-of-concept program in patients with multiple myeloma (MM). MM represents an interesting and sizable opportunity for Actinium. MM is incurable and has a 5-year survival rate less than 50%.

Actinium seems to have a strong scientific rationale with Actimab-M as it targets CD33, which has been found to be expressed in 25-35% of MM patients. This program builds on the company’s experience in the CD33 space from its Phase 2 Actimab-A program in AML. By targeting CD33, Actimab-M may be effective against mutated plasma cells resistant to standard-of-care chemotherapy. Independent work shows that CD33 positive expression is a predictor of poor response and lower overall survival.

Management believes that Actimab-M has the potential to improve outcomes for relapsed or refractory MM patients with limited treatment options available today. This is a very exciting opportunity for the company given the low response rates for existing medications like daratumumab and elotuzumab. It also presents Actinium with the opportunity to develop Actimab-M as both a monotherapy and combination therapy.

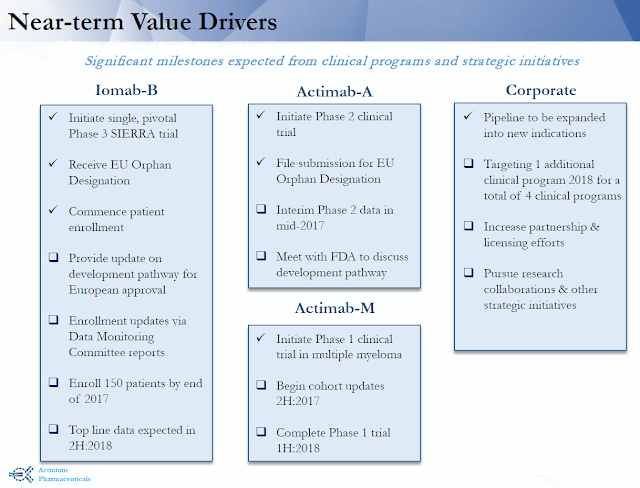

Updates from the recently initiated Phase 1 trial are expected during the second half of 2017. Complete data are expected during the first half of 2018. Management also plans to pursue Orphan Drug designation for Actimab-M in both the U.S. and EU.

Iomab-B Update

The Phase 3 SIERRA trial initiated in July 2016. SIERRA is a randomized, controlled, multi-center study with a target enrollment of 150 patients with refractory or relapsed AML over the age of 55. Enrollment is ongoing right now. Patients are being split equally between Iomab-B and (physician's choice) conventional conditioning prior to allogeneic hematopoietic stem cell transplantation, also known as bone marrow transplant (BMT). The primary endpoint of SIERRA is durable complete response (dCR) at six months post BMT. Secondary outcome measures include safety and overall survival (OS) at one-year.

An important aspect of the trial is that conventional chemotherapy failures (i.e. no CR) subjects can crossover back to Iomab-B. It provides investigators and patients an attractive option for enrollment. By enrolling in the trial, patients know they will either get the best available standard-of-care today or a potentially new breakthrough investigational medicine, and standard-of-care failures get to try the investigational medicine as a second-line option. Keep in mind, Iomab-B is both an induction and conditioning regimen all-in-one, which should be very attractive to physicians and patients alike.

There are several important updates from SIERRA expected in 2017. An independent Data Monitoring Committee (DMC) is watching the trial with an eye on safety. This is important because patients undergoing conditioning prior to BMT are often very sick and at elevated risk for treatment-related serious adverse events (TRAEs). Just recently, Seattle Genetics (SGEN) had to halt several early-stage programs in similar patients because their drug, CD-33A, was causing severe hepatotoxicity, including some incidence of fatal veno-occlusive disease (VOD).

To date, Actinium has not seen any incidence of VOD during its clinical studies in over 400 leukemia and lymphoma patients. Actinium management expects that the first DMC update from SIERRA will happen around the middle of the year once 25% of the patients are treated. A second DMC update at 50% completion is expected late 2017 / early 2018. There will be a third update once 75% of the target population has completed, and top-line safety and efficacy data are expected during the second half of 2018.

The market opportunity with Iomab-B is significant. According to the American Cancer Society, there will be an estimated 21,380 new cases of AML in the U.S. in 2017. Another 27,500 new cases arise in Europe each year. The U.S. NCI estimated 73% of newly diagnosed AML patients are over the age of 55 and there are no currently approved treatment options for these elderly patients with relapsed or refractory disease. It's an estimated patient population of approximately 15,000 individuals, the majority of which cannot tolerate standard conditioning regimens that allow them to progress to a BMT. By offering a more effective and more tolerable solution to these elderly r/r AML patients, Actinium is sitting on a sizable market opportunity with Iomab-B. Standard conditioning regimens cost between $50,000 and $200,000. They can also take as long as 28 to 42 days. At $75,000 for a course of treatment over only six days, Iomab-B targets a $1.15 billion opportunity.

My market opportunity forecast includes both the U.S. and Europe. I'm expecting that Actinium will provide an update on the regulatory pathway in Europe during the second quarter 2017. Given that the U.S. FDA has already signed-off on SIERRA, the EMA can essentially come back with three pathways for Actinium. The first, and most bullish, would be for the EMA to simply accept the data from SIERRA as registration-quality for Europe. The second, also positive outcome would be for the agency to accept SIERRA but asked for supplemental data from the company. This is not likely to be terribly involved. The third option is that the EMA wants to see a full-scale Phase 3 on par with SIERRA in Europe. Odds are hard to assign; but, given that the EMA has already granted Iomab-B Orphan Drug designation in the EU, its seems highly plausible that a positive response is coming.

Actimab-A Update

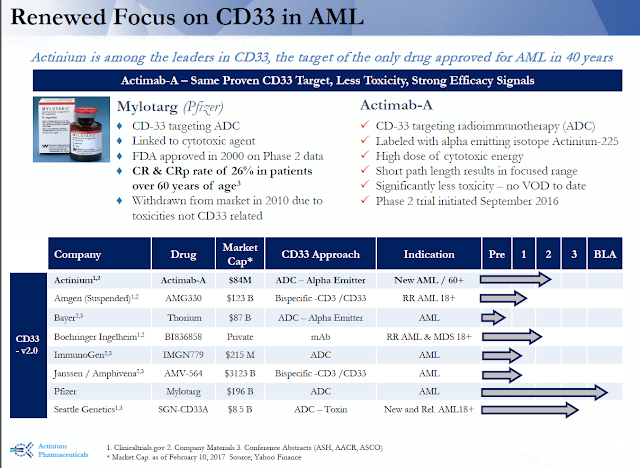

With respect to Actimab-A, a next-generation monoclonal antibody targeting CD33 linked to radioactive actinium-225 (Ac-225), the Phase 2 trial is currently ongoing. The company presented Phase 1 data in December 2016 at the American Society of Hematology (ASH) annual meeting. Investors can read my update following the release of the ASH abstract for more detail on the data. For Actimab-A, interim results from the ongoing Phase 2 trial are expected around the middle of 2017.

CD33 is a clinically and commercially validated target. Actinium is one of the major players in this market, with Seattle Genetics perhaps in the lead. Although, given the safety issues that Seattle Genetics saw recently with CD33A in its transplant trials, Actinium may have the better asset. Pfizer is attempting to resurrect the previously withdrawn Mylotarg®, although it is certainly worth noting that Dr. Mark Berger, who presented the original BLA application to ODAC for the drug while at Wyeth, joined Actinium as Chief Medical Officer (CMO) in January 2017.

Over the next few months, management should be providing updates on the Phase 2 trial. We should get a good sense of the pace of enrollment and whether the protocol changes instituted for Phase 2, including the removal of the LDAC and the inclusion of hydroxyurea to lower peripheral blast count prior to Actimab-A dosing, are having a positive effect. As noted above, top-line data around the middle of the year are incredibly important and could be a game-changer for the company.

Increased Potential For Business Development

With interim Phase 2 data expected from Actimab-A in 2017 and Phase 1 data from Actimab-M expected in early 2018, Actinium’s CD33 pipeline could be of interest to potential partners, especially given the recent activity by several large pharmaceutical and biotech companies in the CD33 field where Actinium remains the most advanced small-cap company. Larger like Pfizer, Seattle Genetics, Amgen, Bayer, and Boehringer Ingelheim are likely keeping a close eye on Actinium's recent success. An alliance around Actimab-A or Actimab-M would likely bring in non-dilutive capital and allow for more aggressive pipeline expansion.

Investors should also be looking for updates from the company’s interactions with EU regulators and how that will impact the development pathway for Iomab-B. A clear development pathway could reduce the costs to access the EU market and set the stage for partnering discussions for Iomab-B in Europe. This is another potential source of non-dilutive capital.

Conclusion

Actinium is well-positioned for continued better stock price performance in 2017. The company has plenty of Cash and lots of pending Catalysts that should work to attract shareholders and drive the stock higher with positive updates. As the stock price moves higher and management continues to deliver on these clinical milestone, Credibility is also likely to rise, giving the company further momentum for out-performance.

Disclosure: BioNap is party to a services agreement with the company that is the subject of this report pursuant to which BioNap is paid twenty-five hundred dollars per month by the company in ...

more