5 Companies With The Biggest Revisions Heading Into Earnings This Week

This week, 110 S&P 500 companies are scheduled to report Q3 earnings results. Heading into those reports a number of names have seen large revisions on both the top and bottom-line. These are the companies with the most revision activity over the past month.

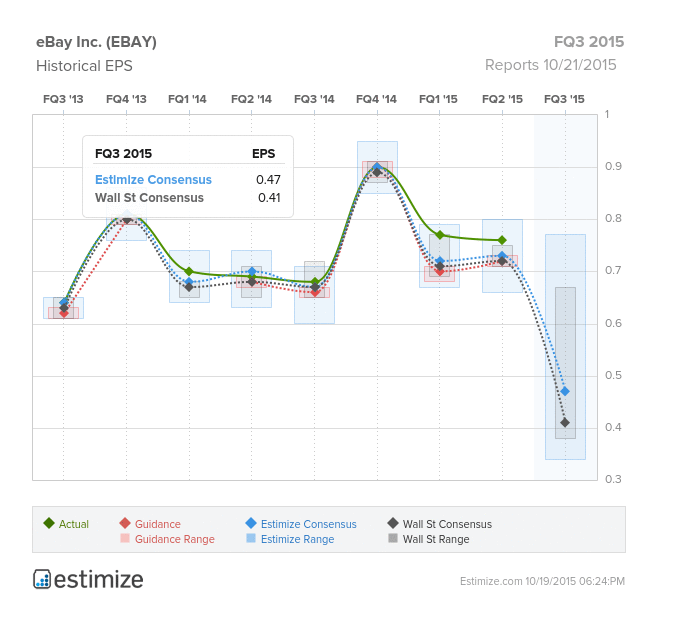

eBay (EBAY)

Information Technology - Internet Software & Services | Reports October 21 after the close.

The Estimize consensus calls for EPS of $0.48, an 11 cent decrease in the last month, yet still 7 cents above the Wall Street estimate. Revenues estimates have also been revised downward, to $2.413B from $2.913B, and the Street is calling for $2.100B.

What to watch: This will be eBay’s first quarterly report since the spinoff of its digital payment arm, PayPal, and it looks like analysts are doubting its strength as a standalone service. It certainly doesn’t help that the retail space in general has been challenged recently, a concern that hit a fever pitch this week after Wal-Mart issued lower than expected guidance for the rest of the year, and into next year, as well as a warning from the National Retail Federation that holiday sales will be weaker this year. We already have July and August numbers from eBay, and they aren’t looking good. US multi-platform unique visitor growth increased 11% YoY in July and August, down from 23% in Q2; it seems doubtful September numbers will be able to make up that difference. Another metric that is always key for retailers is same store sales, which only came in at 5% in July and August, down from 7% in Q2. Gross merchandise volume is expected to fall 6% YoY.

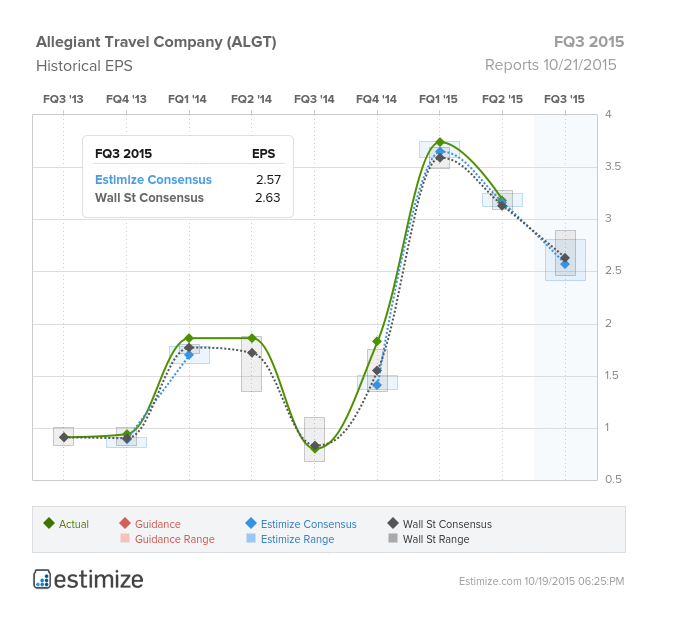

Allegiant Travel Company (ALGT)

Industrials - Airlines | Reports October 21, after the close

The Estimize consensus calls for EPS of $2.56, an uptick of 6 cents from September 22, still below Wall Street’s estimate for $2.60. Revenues have risen only slightly, to $300.1M from $299.4, just above the Street’s consensus for $299.1M.

What to watch: Allegiant is a domestic low cost carrier that has successfully been stealing market share from its larger competitors, something that has lead to double digit EPS growth in the first two quarters this year, and 10% revenue growth in the first half. The company’s value proposition is that it links travelers in small cities to world class travel destinations. While it’s been putting up great fundamentals, and reported a record number of passengers in the latest quarter, revenue per available seat growth has begun to flatten out.

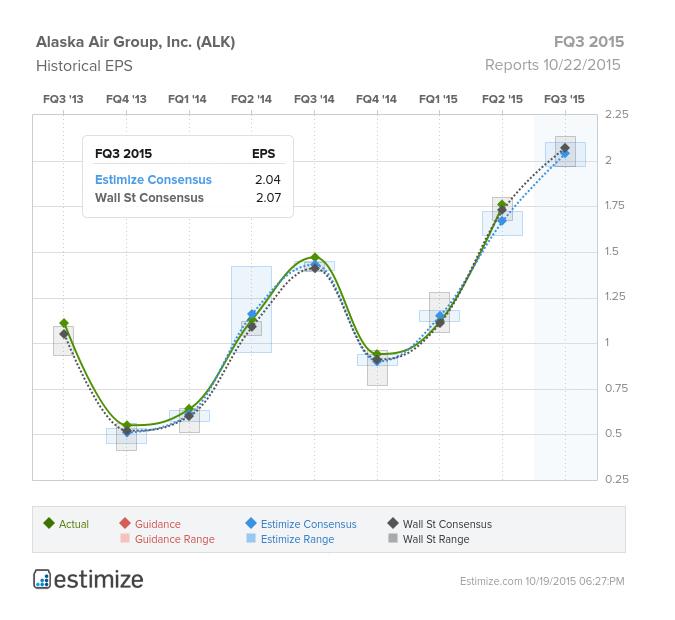

Alaska Air Group (ALK)

Industrials - Airlines | Reports October 22 before the open

The Estimize consensus for ALK stands at $2.03, a nickel better than what was expected at the end of last month, and 4 cents lower than the Street. Revenues have improved slightly to $1.515B, up from $1.508B vs. Wall Street’s $1.512B.

What to watch: The airline results have been mixed this year, with many of the large carriers losing out due to currency headwinds, forcing them to cut down on international flights, and double down on domestic trips. Lower oil has no doubt been beneficial for airlines, but instead of returning fuel savings to the consumer, many airlines have actually been increasing prices this year. Alaska Airlines is a low cost carrier that operates domestically and has been putting up great fundamentals, growing EPS by double or even triple digits for the past 7 quarters, while revenue growth has been more modest in the mid to high single digits. One of the most important metrics for airlines is passenger revenue per available seat mile (PRASM) which has been underwhelming this year to say the least. Even ALK saw a decline in PRASM of 5.3% last quarter. However, Alaska Air is still a relatively small airline with plenty of room to grow. YTD the airline increased capacity by 10%.

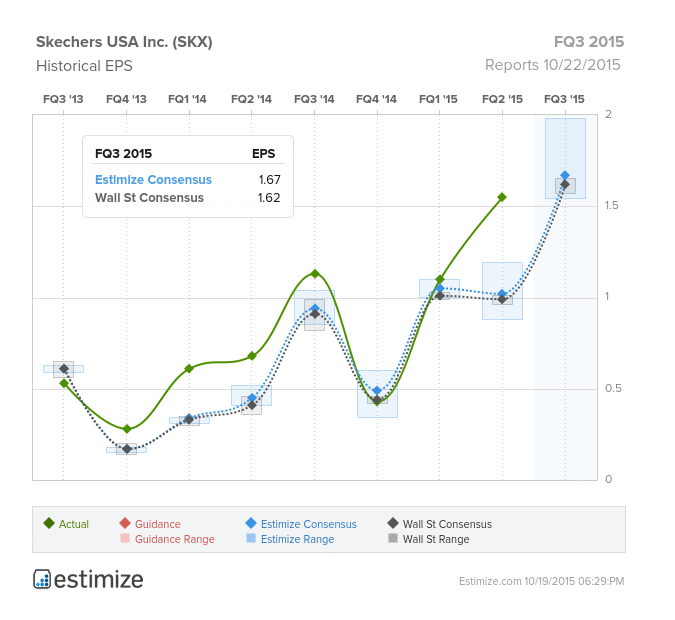

Skechers USA (SKX)

Consumer Discretionary - Textiles, Apparel & Luxury Goods | Reports October 22, after the close.

The Estimize consensus calls for EPS of $1.71, a decrease of 6 cents since the end of September, and still much higher than Wall Street’s consensus of $1.62. Revenues on the other hand have actually increased over that time, to $879.1M vs. $872.9M as compared to the Street’s consensus of $868.4M.

What to Watch: It’s no secret that Skechers is loved by investors who have nearly doubled its value in the past year despite an uncertain and volatile market environment. Fundamentals have been strong this year as well, with the company surpassing the Estimize consensus on the top and bottom-line in Q1 and Q2, and by a sizeable amount. In fact, the Q2 EPS actual beat the higher Estimize consensus by 52%, a 128% YoY growth rate. Despite a decrease in expectations, SKX estimates are still well above the Street and are anticipated to benefit from the back-to-school shopping season. Not only has the company been doing well domestically, but also internationally despite currency headwinds. The athleisure trend has been a large boon for Skechers which is now taking on the bigger athletic brands such as Nike and Under Armour, offering stylish options at more compelling prices. They are slowly starting to steal market share from those names as US consumers begins to pull back on how much of their discretionary income they are willing to allocate to apparel and accessories.

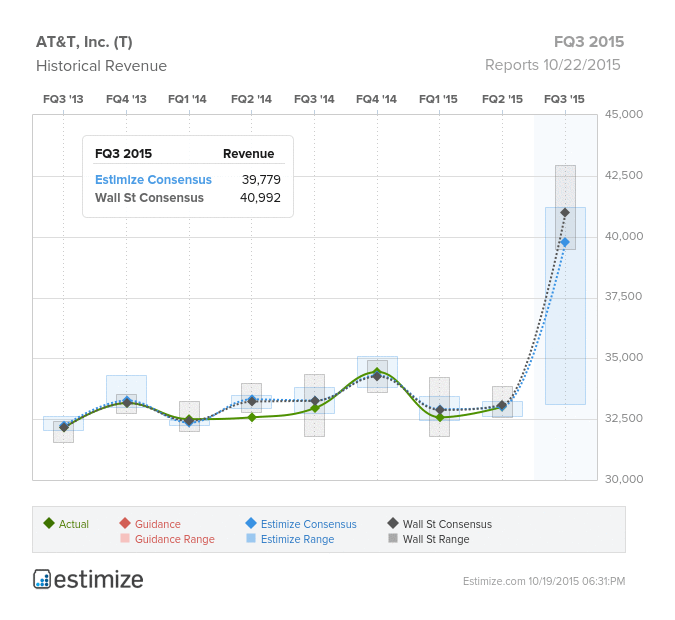

AT&T (T)

Telecommunication Services - Diversified Telecommunications | Reports October 22, after the close

The Estimize community expects EPS of $0.68, in-line with Wall Street, and only increasing 2 pennies over the past two months. Revenues, however, have seen more substantial revisions. Initially expected to come in at $34.529B at the end of August, those estimates have crept up to $39.143B, still below Wall Street’s estimate for $40.99B.

What to watch: AT&T has been scooping up companies left and right this year, starting with its acquisition of Iusacell in January, Nextel Mexico in April, and it’s largest, DIRECTV, in July. That latest acquisition makes the newly combined company the largest pay TV provider in the world, making it a formidable opponent in the streaming video space which is getting increasingly more crowded. The telecom giant also solidified an agreement with Viacom to continue providing Viacom’s media networks, earning rights to distribute Viacom content across its own satellite and internet TV platforms. They also expanded the availability of “U-Verse” with AT&T Gigapower which gives customers the fastest speeds of internet (e.g., the ability to download 25 songs in 1 second). A move into cybersecurity is progressing via a partnership with IBM. The struggle for AT&T is going to be the massive competition in each of the areas where it operates.

Disclosure: There can be no assurance that the information we considered is accurate or complete, nor can there be any assurance that our assumptions are correct.