The Risk Of Confusing Inflation Frames

People who look at and talk about inflation are always having to move between multiple frames. There is the macro versus the micro, the theoretical versus experiential, and of course the short term, medium term, and long term. I spend a lot of time talking about the macroeconomic backdrop (27% money growth, weak velocity that should be recovering), and mostly address the short-term effects when I do the monthly CPI analysis on Twitter (and summarized here, for example this one from last month). And occasionally I do a one-off piece about more lasting effects (e.g. inventories).

But I rarely tie these things together, except quarterly for clients in our Quarterly Inflation Outlook. Right now, though, this is an exquisitely confusing time where all of these frames are colliding and making it difficult to make a simple, clear argument about where inflation is headed and when. So in this column I want to briefly touch on a number of these effects and tie the story together.

Short-term Effects

There are a bunch of short-term effects, or ones that are at least mostly short-term. We recognize that these are unusual movements in costs and prices, and expect them to pass in either a defined period (e.g. base effects) or over some reasonably near-term horizon. This makes them fairly easy to dismiss, and in fact these are not reasons to be fearful of inflation. They will affect CPI, and therefore they will affect how TIPS carry, but they should not change your view of what medium-to-long-term inflation looks like.

- Base effects – We know that last March, April, and May’s CPI reports were incredibly weak, as things like airfare and hotels and used cars absolutely collapsed. Core CPI declined -0.10% in March 2020, -0.45% in April 2020, and -0.06% in May 2020. These were followed by rebounds in some of those categories and in others, with June, July, and August core CPI at +0.24%, +0.62%, and +0.39%. What this means is that if core CPI comes in at 0.20% per month from here, then year/year core CPI will rise to 1.85% in April (when March 2020 rolls off), 2.52% in May, and 2.78% in June. But then it would fall to 2.32% in August (when July 2020 rolls off) and 2.13% in September. You’re supposed to look through base effects like that, and economists will. The Fed will say they’re not concerned, because the rise is mainly base effects – even if other things are going on too. Behaviorally, we know that some investors will react because they fear what they don’t know that is behind the curtain. And that’s not entirely wrong. But in any event this isn’t a reason to be concerned about long-term inflation.

- Measurement things, like rents – Quite apart from the question of whether COVID has caused inflation (or disinflation) is the question of what COVID has done to the measurement of inflation. For example, in the early months of the pandemic the BLS made an effort to not try too hard to get doctors and hospitals to respond to their surveys. Not only were many surveyed procedures not actually happening, but also the doctors and hospitals were clearly in crisis and the BLS figured that the last thing they needed was to respond to surveys, so the measurement of medical care data was sketchy at least early on in the pandemic. And there were many other establishments that were simply closed and could not be sampled. Most of those issues are past, and the echo of them will be past once the March-August period is out of the data. But there are some that persist and the timing of the resolution of which remains uncertain. The most important of these is the measurement of rents, both primary rents (“Rent of Primary Residence”) and the related Owners’-Equivalent Rent. In measuring rent, the BLS adjusts the quoted “asking” rent on an apartment unit by the landlord’s assessment of what proportion of the rent will eventually be collected. So, even if a renter is late on the rent, a landlord who expects to eventually expects to receive 100% of the rent due will cause that unit to be recorded at the full rent.

During the pandemic, of course, many renters lost their incomes and many others recognized that eviction moratoria made it feasible to defer rent payments and conserve cash. As a consequence, measured rents have been decelerating as landlords are decreasing their expectations of eventual receipt, even as asking rents have been rising rapidly along with home prices. The chart below (Source: Pantheon Macroeconomics, from the Daily Shot) illustrates this point. The divergence is explained by the increase in expected renter defaults – and it is temporary. Indeed, if the federal government succeeds in dropping more cash into people’s bank accounts, it will likely help decrease those defaults and we could see a quick catch-up. (That’s actually a near-term upward risk to core inflation, in fact). But in any event this isn’t a reason to be concerned about long-run inflation or disinflation…although the boom in home prices, perhaps, is.

- Shipping Containers – Another item that is related to COVID is that shipping costs are skyrocketing. Partly, this is because shipping containers are in the wrong places (a problem which eventually solves itself); partly, it is because the stock of shipping containers is too small to handle the sudden surge in demand as businesses reopen and not only re-build inventories but also build them beyond what they were pre-COVID (see my article about inventories for why). Deutsche Bank had a note out yesterday opining that while this spike in shipping costs – see the chart of the Shanghei (Export) Containerized Freight Index, source Bloomberg, below – will eventually ebb, it may not go down to its long-term average. But, still, the majority of this spike in costs, which is felt up and down the supply chain and drives higher near-term inflation for everything from apparel to pharmaceuticals, will ebb and isn’t a reason to be concerned about long-run inflation.

- Raw Materials – The same picture we see in the Shipping Containers chart is evident in lots of other raw materials markets. I’m not speaking here as much about the large commodities complexes like Copper, Lead, Oil, and so on but about certain less-widely followed but no less important markets. One you may have seen is steel (see chart, below, of front Hot Rolled Steel futures), which have nearly tripled since the summer and are about 30% above 2018’s highs with no end apparent.

Closer to my heart, and one you’re less likely to have seen, is the chart of resin futures. This is polymer grade propylene, which is a precursor to polypropylene. PP is used in all sorts of applications, from clothing and other fabrics to packaging (soda bottles!) of all kinds. And North American supplies of PP are under what can only be called severe pressure. Front PGP has more than quadrupled since the spring, and is at multi-year highs (if you can find an offer at all). It’s up 142% since mid-December! And PP is up even more, as producer margins have widened. Folks who want to track this and related markets might start by visiting theplasticsexchange. The reasons for this spike are part technical, although caused by the sudden re-start of the global economies, and will eventually pass. As with shipping, it may not go back to what was “normal,” but in any case movements like this, or those with steel or other raw materials, are not reasons to be concerned about long-run inflation. However, they likely will affect CPI prints as these are inputs into all sorts of goods.

That is a non-exhaustive list of some of the short-term effects that are directly or indirectly related to the stop-start of the COVID economy. They will pass, but they add a tremendous amount of sturm und drang to the price system and can confuse the medium and longer-term impacts.

Medium-term Effects

Some of the medium-term things that are happening, and that matter, and that will last, will be missed. Here are a few on my list:

- Pharmaceutical prices – One of the really fascinating things we have seen over the last few years has been the slow deceleration in inflation of medical care commodities, specifically drugs. The chart below (source Bloomberg) shows the y/y change in the CPI for Medicinal Drugs. In late 2019, after slipping into deflation, drug prices appeared to find a footing and to be recovering. But even before COVID, this jump was starting to ebb and in the most-recent 12 months pharmaceuticals prices experienced their largest decline in decades. Why?

One reason this happened is because the Trump Administration threatened drug companies with a “Most Favored Nation” clause. This means that the drug companies would not be allowed to sell their products in the United States at a higher price than the lowest price they charged overseas. The Trump Administration said that this would cause massive decreases in drug costs; this clearly wasn’t true (for reasons I discussed here last August) but it would tend to cause drug prices to decline in the US at least a little, especially relative to other countries’ costs. Faced with this, drug companies played nice…until Mr. Biden won the Presidency, in at least small part because some of the large vaccine developers slow-rolled their vaccine announcement until after the election. In January, they started moving prices higher again. This may hit the CPI as early as this month. But unlike with the short-term effects listed above, this is not a response to COVID or its ebbing, and it isn’t something that is likely to change. The Biden Administration is much less antagonistic towards drug companies than the Trump Administration was. And by the way, it isn’t just the drug companies that fall in this category. (Insert snarky comment about Trump here.)

- I mentioned earlier my article about how inventory management is going to change as a result of COVID. Indeed, the fact that it is already changing is one reason that the supply/demand imbalance is so bad in the short run: as I have already said, companies are building back inventories and adding additional safety stock, and that is stressing production of all sorts of goods. That was a short-term effect but the more-lasting effect is that carrying larger inventories is itself more expensive. Inventory carrying costs increase the costs of goods sold (which is the main reason managers have been pushing them down for decades). Carry more inventory, prices go up more. I don’t think this trend will ebb.

- Another trend I’ve seen directly, and am comfortable generalizing, is a movement among manufacturers towards shortening supply chains. The problems with production during COVID, along with the aforementioned shipping tie-ups, argues for shorter supply chains and diversified country sources (don’t get everything from India, for example, in case India as a whole shuts down). Also, shortening supply chains means that inventories (see #2) can be a little lower (or rather, safer at any given level of inventory) since one of the drivers of inventory size is lead time. Customers seem willing, at least today, to pay up to get suppliers in the same hemisphere and even more to get them in the same country. Every purchasing manager noticed that in the depths of the COVID shutdown many countries toyed with the idea of completely closing borders; some countries required container ships to ‘quarantine’ offshore for a time before they could unload. No one expects another COVID, but the -19 version reminded everyone of how the fragility of the supply chain increases with distance. Because in this country, shorter supply chains imply higher costs (since production is still generally cheaper overseas, though that differential has shrunk a lot), this is a short-term level adjustment followed by a lasting upward trend pressure on pricing. It’s essentially a partial reversal of the globalization trend, which reversal had already begun in little ways under the Trump Administration.

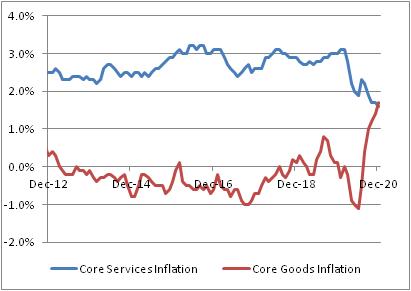

Granted, much of this is manufacturing-focused and most of the consumption basket (thanks mostly to rents) is services. But for many years it had been goods inflation holding down overall inflation, until recently. In the last CPI report, Core Goods inflation moved above Core Services inflation for the first time in a long, long time. That looks more like the inflation we remember from the ‘70s and ‘80s, with a much broader set of services and goods inflating.

Macro-level Effects

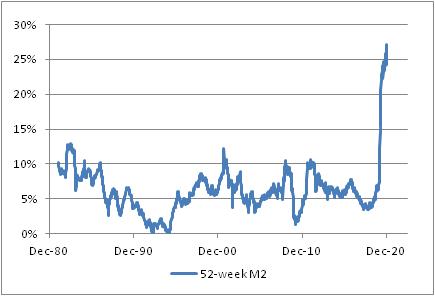

The last frame I want to touch on is the macro, top-down inflation concern. I won’t spend much time arguing whether output-gap models are working…if they were, then we would be in heavy deflation right now and there would be no signs of inflation anywhere, so clearly that’s the wrong model…and merely point briefly to the now-well-documented surge in M2 money supply growth (see chart, source Bloomberg), which is currently 27% y/y in the US, 11% y/y in Europe, 14% y/y in the UK, and even 9.2% in Japan. The increase in the transactional money supply in the US is twice as large as anything we have ever seen in this country, aside perhaps from the very early days when “not worth a Continental” became a term of opprobrium. Some people have argued that since money growth in 2008-9 didn’t produce much inflation, we oughtn’t worry about it this time either. But the last crisis really was different, as it was a banking crisis (I wrote about this almost a year ago).

So, unless central banks have been doing it all wrong for a hundred years, the bare intuition is that this much money supply growth probably won’t be a non-event. Money velocity, in the short term, plunged because (a) mechanically, cash dropped into bank accounts by a generous government takes some time to spend, and (b) understandably, the demand for precautionary cash balances got super high during COVID. Both of these are passing issues, and it takes some heroic assumptions to argue why money velocity should continue to decline. Not merely stay low: if money growth continues at the 27% pace of the last year or even just the 13%-16% pace of the last quarter, even stable money velocity would produce much higher prices.

Over time, the relationship of money to GDP is a great proxy for the price level. That model has been powerful for a hundred years, and it makes sense: increasing the money supply 25% doesn’t increase wealth 25%. The amount of things you can buy with that money doesn’t change very much. So the value of the measuring stick, the dollar itself, must be weakening since 25% more dollars buys the same amount of stuff. To be sure, that’s only if people spend the new dollars as fast as they spent the old dollars, so if there’s a permanent change in velocity this won’t be true. But it needs to be a permanent change in velocity, and outside of lowering interest rates we don’t have a great way to induce permanently lower velocity.

[As an aside, the same reasoning applies to asset markets rather than consumables. Because the real output of businesses, and the stock of physical assets, don’t change very fast, a large increase in money must increase the nominal price of those things (or, more accurately, decrease the value of the measuring stick). But how to account for a decline of the value of the dollar in purchasing financial assets, but no big decline in the value of the dollar for purchasing goods and services? This implies a change in the exchange rate between real goods and financial assets. That is, a person can exchange a Tesla for fewer shares of TSLA. But unless markets are permanently valued at higher multiples when the economy is flooded with cash (and there’s no sign that has happened before in the long sweep of history with episodes of rising money supply), eventually the price of shares must decline or the price of consumption goods rises, or both. Essentially, money illusion is operating in one sphere, but not in the other, and I think that’s unsustainable. Maybe I’ll write more about this another time.]

On the macro front, the alarm bells should be ringing very loudly.

So in the three frames above we have some effects that are easy to look through, and to ignore as temporary. We have some effects that are more subtle, but long-lasting. And we have some effects that are potentially huge, and haven’t come to the fore yet at least in the consumption basket. On the whole, the signs are compelling that inflation is very, very likely to rise in a way that is not just temporary. But, because these frames are confusing, and because the Fed (and others) will easily dismiss some of the one-off effects as temporary COVID effects – which they are – this is actually an acutely dangerous time for investors. The fog of war, provided by these short-term effects, will obfuscate some of the longer-term effects and ensure that policymaker response is late, halting, and inadequate. Markets, though, will be reacting in what some will call an exaggerated reaction. Indeed, some already believe that the rise of 10-year breakevens to near-two-year highs, at 2.17% today, is an overreaction.

I don’t think it is. We are going to see core inflation rise on base effects and one-offs, then decline on base effects, but probably not as much as people expect right now. That’s when the fog will begin to clear, and we will see inflation accelerating from a level that’s already higher than it is now. By the time the fog of war clears in late 2021 or early 2022, it will be late to start planning for inflation. Maybe not too late, but late. By the time everyone agrees inflation is a problem, the price of inflation protection will have moved a lot.