The Post-Pandemic Retirement Survival Guide - Part 1

Consider the post-pandemic retirement survival guide an awakening—a way to look at your retirement plan with a fresh perspective. At the least, I hope it serves as a reminder of how fragile a retirement planning strategy can be, and the ability to remain flexible in thought is so important.

Perhaps you’re one of the fortunate people not concerned about the viability of your retirement strategy. After all, markets predict that ‘normal’ is a quarter away (whatever normal happens to be). But be assured, the pundits say it’ll be magic.

They say that the pandemic and its after-effects will be poof: Gone. It’ll be like the global economies never experienced economically devastating lockdowns, a spike in mental health obstacles, and substance abuse. Also, let’s not forget the mind-blowing increase in extreme poverty.

I mean, just like that, the world’s economies will recover from the strange global quarantine of healthy people (never happened before). Oh, the lofty, idealistic haze of markets and its prognosticators drunk on fiscal and monetary stimulus.

What does post-pandemic financial recovery mean to you?

So, whatever ‘post’ pandemic means to you, keep in mind, retirees or those looking to retire anytime in the future, perceive economic recovery through a darker lens. In other words, a post-pandemic retirement may be a ‘no retirement.’ Due to personal financial setbacks, more retirees than ever are deciding never to retire.

“With the present economy due to Covid, I am afraid it will take several years to recover and for our retirement savings and investments to be enough for us to retire the way we originally set it up.”

National Institute of Retirement Security, February 2021.

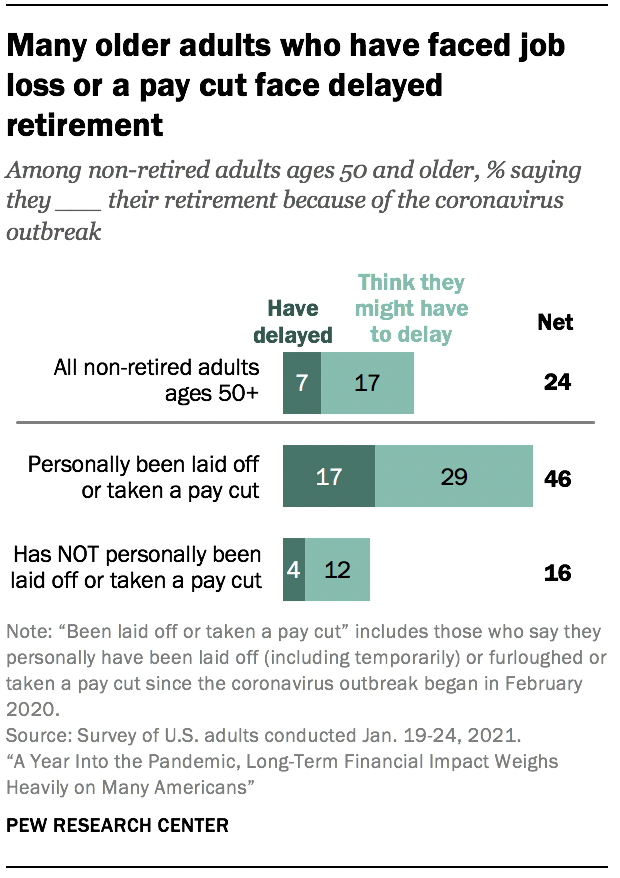

Pew Research, a bipartisan research think tank, conducted a study of 10,334 adults in January 2021 and discovered that a quarter of adults 50 and older who have not yet retired, expect the coronavirus outbreak to affect their ability to retire.This includes 7% who say they have already delayed their retirement and an additional 17% think they might have to delay it.

Don’t worry. We can work together to make sense of it all.

I truly hope your household possesses the resiliency to meet financial goals in a timely manner post-pandemic.

As part of a comprehensive Post-Pandemic Survival Guide, these three actions would be on the top of my list. My next three will appear in part 2.

Action #1: Be open to creating your own pension.

Dave Ramsey, the guru of debt management, penned a piece (or somebody did) for his blog in February 2021 titled Why a 401(k) is Better Than a Pension. Please read it for yourself. What do you think? Frankly, I found the information disingenuous, somewhat tone-deaf, and replete with paragraphs of incomplete information. It appears some staffer with limited knowledge or study of retirement trends cobbled it together.

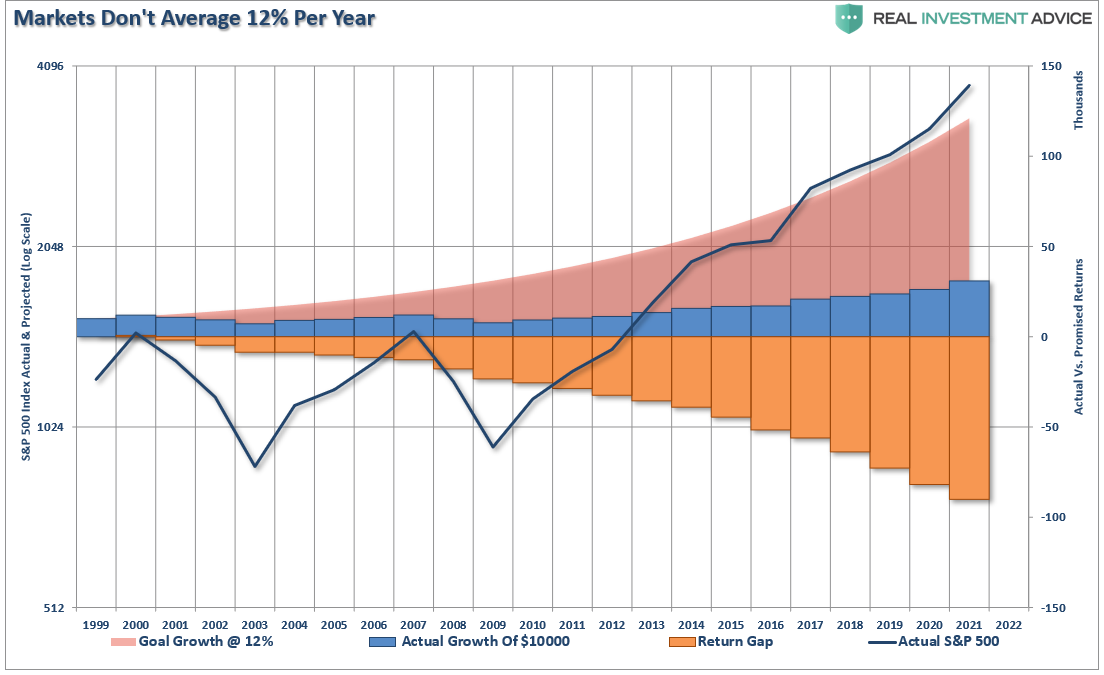

For example, the post indicates the ‘average rate of return’ for a 401k is 12% and 7% for a pension without reference to how these numbers are derived. Seemingly, I assume that 12% is comprised of an all-equity portfolio that most investors could not stomach emotionally long-term. But, let’s say an aggressive investor does ride out the volatility and emotions are not an issue.

Are you the SPOCK of investing?

In other words, let’s imagine Science and First Officer, the highly logical, unemotional SPOCK stationed on the USS Enterprise, is a champ at socking part of his salary away in a 401k.Even if he were an above-average investment picker (and we’re not even going to tackle 401k choices), a 12% average annual return is more science fiction than reality.

Per the chart below by Lance Roberts, markets don’t average 12% a year. Most retirement reality lies in the orange zone or gap between Dave Ramsey’s fantasy and actual portfolio returns.

(Click on image to enlarge)

Per the article’s table, one main difference between a 401k and a pension (true but vague) is the former creates an income ‘as ‘until the money is gone,’ vs. ‘your lifetime.‘When it comes to retirement, we should seek to have the money last as long as we do! Lifetime vs. ‘until the money is gone’ sort of sums up the variability and unpredictability of a consistent stream of income from volatile assets such as stocks and bonds (unless you’ve been earning 12% a year over a lifetime). In that case, I’d like to interview or nominate you for an award!

Some investors can indeed retire comfortably on stock and bond portfolios. The maximization of Social Security (that lifetime income again), enhances the lifestyle spending of even the best of savers and investors. I know. We witness it all the time in our financial planning process.Those fortunate enough to have pensions are able to consider retirement as early as age 55 and not be concerned about longevity risk. In other words, lifetime income options allow retirees to run out of life before they run out of money!

Dave Ramsey is out of touch.

It appears Dave is a bit out of touch with mainstream America. I understand. He’s a money celebrity. In all fairness, why would he understand the damage that has been done to retirement security due to the loss of pensions even though there are reams of studies making the case for them?

Per the National Institute on Retirement Security in a recent survey, When it comes to pensions, Americans have highly favorable views about their role in the retirement equation and see these plans as better than 401(k) savings accounts.

Seventy-six percent of Americans have a favorable view of defined benefit pensions. Seventy-five percent say that all workers should have access to a pension plan to be independent and self-reliant in retirement. Sixty-five percent agree that pensions are better than 401(k) accounts for providing retirement security.

Also, women are more receptive to guaranteed income solutions. Over 59% of women in another study, stated they would feel more secure with a portion of their portfolios invested in annuity structures that protect against market risks. It makes sense as outliving their nest eggs is a formidable concern.

Please understand, I’m a huge advocate for stock investing. I started at age 13 and never looked back. However, stocks are part of an overall retirement income plan. A variable portfolio is designed to supplement and guard a retirement income stream against inflation long-term. It’s never an all or none situation. For some, rolling over a pension to an IRA is the optimum choice. For others, it’s to take the pension to protect against longevity risk. It takes formal financial planning to decide the proper, personal path to follow.

Americans overall are finally beginning to understand how important guaranteed income is to a secure retirement future.

The NIRS study showcases the importance of Social Security to working-age people:

Americans are highly supportive of Social Security, and there is some support for expanding the program. The vast majority of Americans (79 percent) agree that Social Security should remain a priority of the nation no matter the state of budget deficits, with nearly half (49 percent) in strong agreement. Most Americans (60 percent) agree that it makes sense to increase the amount that workers and employers contribute to Social Security to ensure it will be around for future generations. And half support expanding Social Security, with 25 percent saying it should be expanded for all Americans and 25 percent saying it should be expanded except for wealthier households.

I suspect the popularity of guaranteed income options like single-premium immediate annuities will continue to grow.Overall, investors purchase annuities without truly understanding how they work, or even if they do, they’re purchased without a plan to determine: when to buy, which to buy, how much to buy.

Do you have a retirement income strategy?

Work with an objective financial partner to determine if a guaranteed income product can augment your retirement income strategy. Be open to it, especially if there’s a shortfall based on you and your spouse’s life expectancy.

Dave Ramsey’s debt-management messages are honorable. His understanding of how guaranteed income can save a retirement is disappointing, to say the least. He’s talented and smart. He can do better.

Be open to creating your own pension if it’s necessary. The only way to find out is to complete a holistic financial plan.

Action #2: Hit the mental refresh.

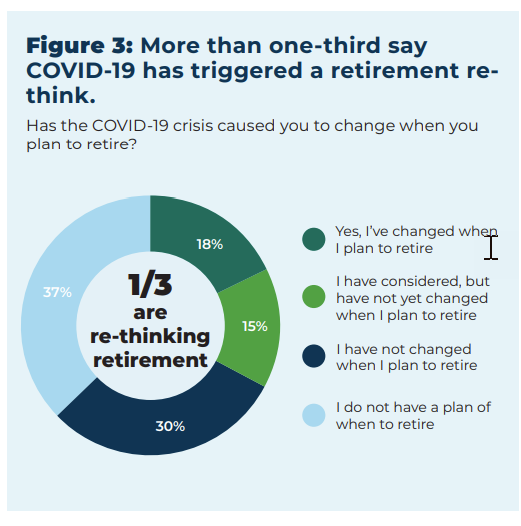

According to the Retirement Insecurity Report 2021 from the NIRS, a third of workers polled believe the pandemic has compelled rethink retirement timing. Close to 18 percent have changed when they plan to retire, and 15 percent have considered a change. Close to 70 percent say they will retire later than expected. At our Retirement Right Lane class, we hear consistently from attendees who were forced to return to the ‘highway of work’ and postpone retirement due to an adverse economic event.

I’m not saying it’s easy to scrutinize your retirement plans with fresh eyes or start one. It can be a formidable mental challenge. However, after what we’ve all been through over the last year, it’s worth the effort to review goals, stress-test your retirement date and undertake an overall assessment of your household’s possible financial vulnerability in light of unprecedented fiscal and monetary stimulus that has greatly distorted the valuation of stock investments.

Psychological vs. financial. They both count!

This is as much a psychological event as it is financial, which is why most respondents in the illustration above don’t have a plan of when to retire. Why bother if it feels hopeless? Why consider a plan when retirement is a pipedream or it’ll require a household to greatly curtail a lifestyle?

It’s sort of similar to how I used to feel about annual physicals. Years ago, I believed ignorance was bliss. I knew I was eating badly and required vigorous exercise but candidly, I didn’t want to face the truth, expose my weaknesses and correct them.

I had to jump a hurdle and forge ahead mentally. Today, I complete blood diagnostics every three months and never miss my physical. I work out hard and four years ago completely changed my eating habits. In other words, I look forward to understanding what’s going on with my body because I’ve made changes to improve and expose my weakest links.

Formal financial planning sometimes doesn’t feel good.

For many, formal retirement planning equates to feeling financially vulnerable. However, a comprehensive plan and a bit of ‘soul searching’ over what’s truly important can lead to constructive results and a reasonable action plan of improvement.

Most likely, the pandemic has positively changed your habits, especially around spending and debt. Perhaps you run a tighter fiscal ship. Can you keep it up? The long-term change can help set more realistic lifestyle expectations in the future.

Now is a good time to micro-budget.Micro-budgeting is a solid way to understand where household cash goes on a deeper level. Spend twenty minutes at the end of the day to inventory your spending. Don’t use tech either. Use pen and paper. I really like the Clever Fox Budget Book. It’s a compact notebook for expense tracking and organizing. Oh, another thing: Don’t have retail receipts e-mailed to you. Ask for them, store them in the notebook, total them at the end of the day.

Visualize how your life will look in retirement.

Visualize the smallest you could live in retirement. What would it look like? Document what you see. Then with the help of a financial planner help to translate the lifestyle to concrete, attainable goals.

It’s no longer a time to hide from retirement planning. No retirement is perfect. Believe me, it’s a liberating experience to get started.

Action #3: Understand what drives the tailwinds to your portfolio gains.

Sorry. That wind in your investment sails isn’t investment prowess. It’s eye-popping, unimaginable monetary, and now, fiscal stimulus (and more is coming evidently)! Also, stocks are in demand, and investors are using credit to purchase them! Investors have borrowed a record $814 billion on margin to fuel the stock market rally.

So, valuations don’t matter. For now, anyway. I can show you years where stocks were cheap, and nobody wanted them. You see, stocks are the product investors want (until they don’t).

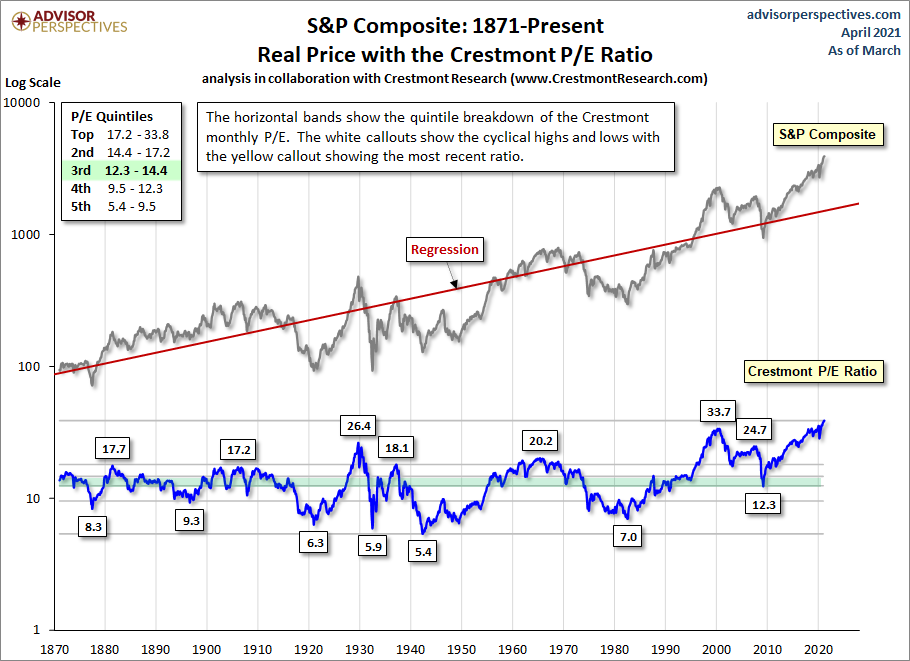

Speaking of valuations (just trying to keep your head out of the clouds, that’s all), here’s the latest update from Crestmont Research with analysis from Advisor Perspectives.

(Click on image to enlarge)

The Crestmont P/E 10 now stands at 38.8 or 166% above its long-term average. It’s now exceeded tech-bubble levels. I know. BORING. Nobody cares about valuations anymore (again, until they do). However, valuations eventually do matter, and regression to the mean does occur. I mean, unless it’s ‘different this time, and we all know it’s never truly different.

What should investors expect from stocks as we advance?

All I want readers to understand, especially pre-retirees, retirees, is that returns on risk assets may need to moderate or be reduced to account for euphoria witnessed today over the next ten to fifteen years. This means that paying attention to profit-taking, monitoring risk, along with portfolio withdrawal rates, remain important.

Don’t allow your emotions to become your investment or portfolio strategy. Remaining level-headed and humble in the face of massive liquidity assures you’ll still respect the risk that comes along with stock investing.

Disclosure: Real Investment Advice is powered by RIA Advisors, an investment advisory firm located in Houston, Texas with more than $800 million under management. As a team of certified and ...

more