The One Lesson Investors Should Have Learned From Pension Funds

Just recently I ran a 3-part series on the variety of things individuals believe about saving and investment which is either erroneous or misunderstood. (Part 1, Part 2, Part 3)

The feedback I get when challenging some of the more commonly held beliefs is always interesting. In almost every single case, the arguments against “mathematical realities” comes down to either:

- An inability, or unwillingness, to sacrifice today to save more for the future, or;

- A “hope” that markets will continue to create returns which will offset the lack of savings.

Okay, it is just a reality that most people don’t want to sacrifice today, for the future tomorrow.

“Live like no one else today, so that you can live like no one else tomorrow.” – Dave Ramsey

Unfortunately, that is the same problem that plagues pension funds all across America today.

As I discussed in “Pension Crisis Is Worse Than You Think,” it has been unrealistic return assumptions used by pension managers over the last 30-years, which has become problematic.

“Pension computations are performed by actuaries using assumptions regarding current and future demographics, life expectancy, investment returns, levels of contributions or taxation, and payouts to beneficiaries, among other variables. The biggest problem, following two major bear markets, and sub-par annualized returns since the turn of the century, is the expected investment return rate.

Using faulty assumptions is the linchpin to the inability to meet future obligations. By over-estimating returns, it has artificially inflated future pension values and reduced the required contribution amounts by individuals and governments paying into the pension system

Pensions STILL have annual investment return assumptions ranging between 7–8% even after years of underperformance.”

However, why do pension funds continue to have high investment return assumptions despite years of underperformance? It is only for one reason:

To reduce the contribution (savings) requirement by their members.

As I explained previously:

“However, the reason assumptions remain high is simple. If these rates were lowered 1–2 percentage points, the required pension contributions from salaries, or via taxation, would increase dramatically. For each point of reduction in the assumed rate of return, it would require roughly a 10% increase in contributions.

For example, if a pension program reduced its investment return rate assumption from 8% to 7%, a person contributing $100 per month to their pension would be required to contribute $110. Since, for many plan participants, particularly unionized workers, increases in contributions are a hard thing to obtain. Therefore, pension managers are pushed to sustain better-than-market return assumptions, which requires them to take on more risk.

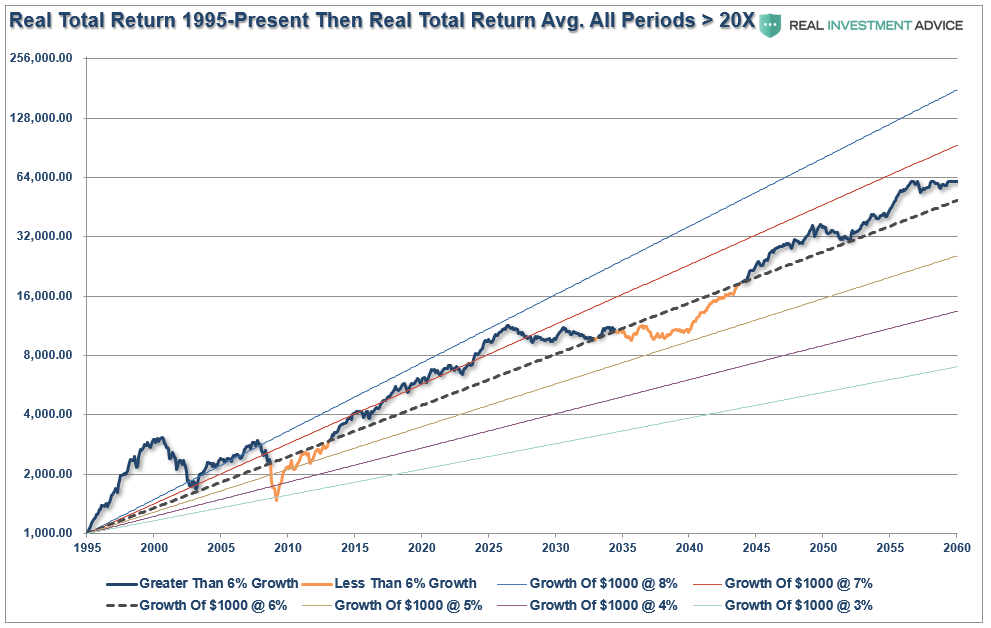

The chart below is the S&P 500 TOTAL REAL return from 1995 to the present. I have projected an average return of every period in history where the market peaked following P/E’s exceeding 20x earnings. This provides for variable rates of market returns with cycling bull and bear markets out to 2060. I have also projected “average” returns from 3% to 8% from 1995 to 2060. (The average real total return for the entire period is 6.56% which is likely higher than what current valuation and demographic trends suggest it should be.)”

This is also the same problem for the average American faces when planning for 6-8% annual returns on their investment strategy.

Clearly, there is no reason you should save money if the market can do the work for you? Right?

This is a common theme in much of the mainstream advice. To wit:

“Suze Orman explained that if a 25-year-old puts $100 into a Roth IRA each month, they could have $1 million by retirement.”

Ms. Orman’s statement, while very optimistic, requires the 25-year old to achieve an 11.25% annual rate of return (adjusting for inflation) every single year for the next 40-years.

That certainly isn’t very realistic.

More importantly, as I explained previously, $1 million today, and $1 million in 30-years, are two very different issues due to a rising cost of living over time (a.k.a. inflation.)

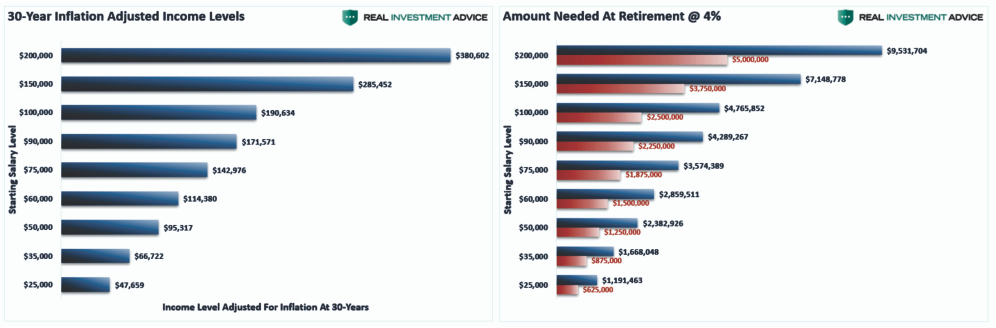

Pick a current income level on the left chart, the number on the right is the current income inflated at 2.1% (average inflation rate) over 30-years. Then pick that level of income on the right chart to see how much is needed to fund that amount annually in retirement at 4% (projected withdrawal rate.) Click to enlarge

What pension funds have now discovered, and unfortunately it is far too late, is that using faulty assumptions, and not requiring higher contributions, has led to an inability to meet future obligations.

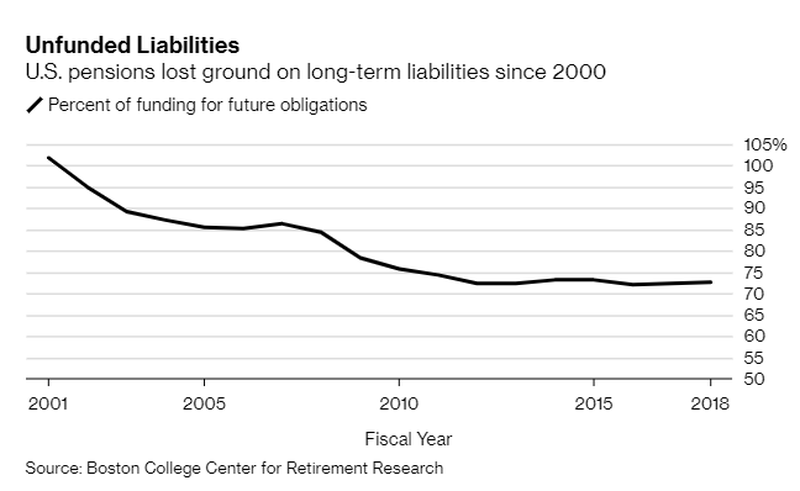

“Pensions across the U.S. are falling deeper into a crisis, as the gap between their assets and liabilities widens at the same time that investment returns are falling, according to Bloomberg.

The average U.S. plan has only 72.5% of its future obligations in 2018, compared to more than 100% in 2001. The Center for Retirement Research at Boston College attributes the deficit to recessions, insufficient government contributions, and generous benefit guarantees. Importantly, the underfunded status is still based on 7% annual return assumptions.

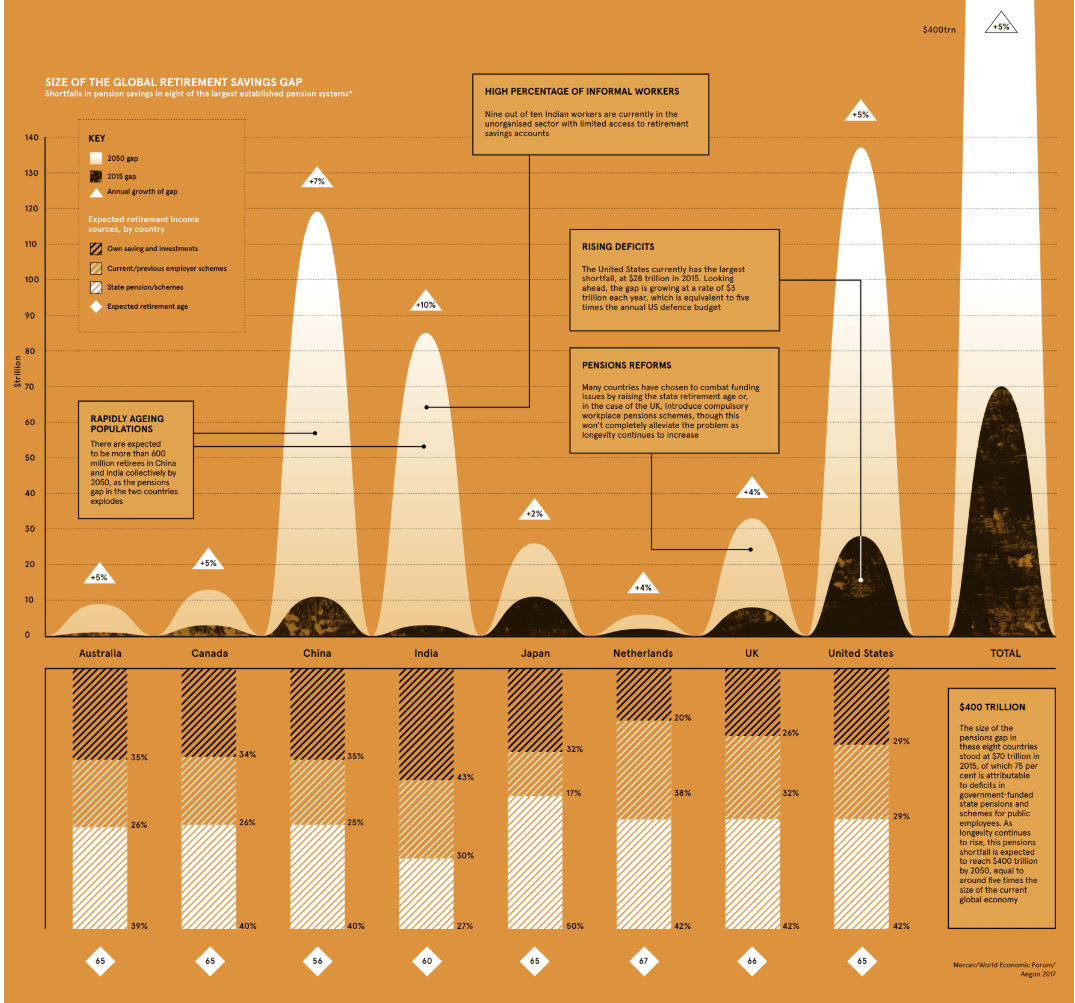

Unfortunately, the problem will only get worse between now and 2050, according to Visual Capitalist:

“According to an analysis by the World Economic Forum (WEF), there was a combined retirement savings gap in excess of $70 trillion in 2015, spread between eight major economies…The WEF says the deficit is growing by $28 billion every 24 hours – and if nothing is done to slow the growth rate, the deficit will reach $400 trillion by 2050, or about five times the size of the global economy today.”

It isn’t just Pension Funds

Importantly, this is the same trap that individual investors have fallen into as well. By over-estimating future returns, future retirement values are artificially inflated, which reduces the required savings rates. Such also explains why 8-out-of-10 American’s are woefully underfunded for retirement currently.

Using the long-term, total return, inflation-adjusted chart of the S&P 500 above, the chart below compares $1000 compounded at 7% annually to the variable-rate of return model above. The bottom part of the chart shows the difference between actual and compounded rates of return.

This is the “pension problem” the majority of individuals have gotten themselves into currently.

As I wrote previously:

“When imputing volatility into returns, the differential between what individuals are promised (and this is a huge flaw in financial planning) and what actually happens to their money is substantial over the accumulation phase of individuals. Furthermore, most of the average return calculations are based on more than 100-years of data. So, it is quite likely YOU DIED long before you realizing the long-term average rate of return.”

Excuses Will Leave You Short

I get it.

I am an average American too.

Here are the most common excuses I hear:

- I “need” to be able to enjoy my life today.

- I have “plenty of time” to save up for retirement.

- “Budget,” what ‘s that?

- I have social security (or a pension plan), so I don’t really need to save much.

Let’s talk about that last point.

If you have a public pension plan, congratulations, you are in the 15% of workers that do. Future generations won’t be as fortunate. Moreover, with the underfunded status of pensions funds running between $4-5 Trillion, this may not be a “safety net” to bet your entire retirement on.

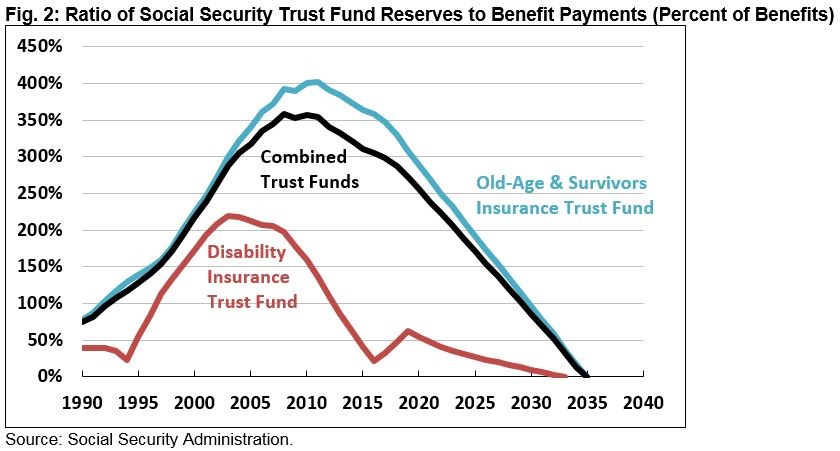

Social security is also underfunded and payout cuts are expected by 2025 if actions are taken to resolve its issue. The same demographic trends which are plaguing pension funds also weigh heavily on the social security system.

As stated above, the biggest problem for Social Security is that it has already begun to pay out more in benefits than it receives in taxes. As the cash surplus is depleted, which is primarily government I.O.U.’s, Social Security will not be able to pay full benefits from its tax revenues alone. It will then need to consume ever-growing amounts of general revenue dollars to meet its obligations–money that now pays for everything from environmental programs to highway construction to defense. Eventually, either benefits will have to be slashed or the rest of the government will have to shrink to accommodate the “welfare state.”

It is highly unlikely the latter will happen.

Demographic trends are fairly easy to forecast and predict. Each year from now until 2025, we will see successive rounds of boomers reach the 62-year-old threshold.

Excuses aside, continuing to under-save, and counting on social security and a pension fund to make up the difference, may have very different outcomes than many are currently planning on.

Simple Is Not Always Better

“All you have to do is buy an index fund, dollar cost average into it, and in 30-years you will be set.”

See, it’s simple.

It is why our world has been reduced to sound bytes and 280-character compositions. Financial, retirement, and investment planning, while complicated issues, in reality, have become “clickbait.”

But a “simple and optimistic” answer belies the hard-truths of investing and market dynamics.

It’s what Pension Funds banked on.

Simple isn’t always better.

Currently, 75.4 million Baby Boomers in America—about 26% of the U.S. population—have reached, or will reach, retirement age by 2030. Unfortunately, the majority of these individuals are woefully under saved for retirement and are “hoping” for compounded annual rates of return to bail them out.

It hasn’t happened, it isn’t going to happen, and the next “bear market” will wipe most of them out permanently.

The analysis above reveals the important lessons individuals should have learned from the failure of pension funds:

- Lower expectations for future returns and withdrawal rates due to current valuations, interest rates, and long-run economic growth forecasts.

- With higher rates of returns going forward unlikely, increase savings rates.

- The impact of taxation must be considered in the planned withdrawal rate.

- Future inflation expectations must be carefully considered; it’s better to overestimate.

- Drawdowns from portfolios during declining market environments accelerates the principal bleed. Plans should be made during up years to harbor capital for reduced portfolio withdrawals during adverse market conditions.

- Future income planning must be done carefully with default risk carefully considered.

- Most importantly, drop compounded, or average, annual rates of return for plans using variable rates of future returns.

The myriad of advice suggesting one can undersave and invest their way into retirement has a long and brutal history of leaving individuals short of their goals.

If even half of the mainstream commentary on investing were true, wouldn’t there be a large majority of individuals well saved for retirement? Instead, there are mountains of statistical data which show the majority of American’s don’t even have one-year’s salary saved for retirement, much less $1 million.

Yes, please be optimistic about your future and “hope for the best.”

However, if you plan for the “worst,” the odds of success become much higher.

It’s a lesson we can all learn from Pension Funds.