Time To Take A Ride With TripAdvisor?

TripAdvisor (NASDAQ:TRIP) has a loyal base of 390 million monthly unique visitors who submit 280 contributions per minute (hotel/travel reviews). This treasure trove of user-generated content has enabled the company to build a high-margin, defensible business. There are three key pillars of our investment thesis on TRIP (which we will dive into in greater detail in our upcoming Company Scenarios and Research report):

- The secular trend of hotel reservations moving online;

- The high-margin potential of TRIP's business model; and

- An impending return to y/y revenue growth as we lap the Instant Book rollout.

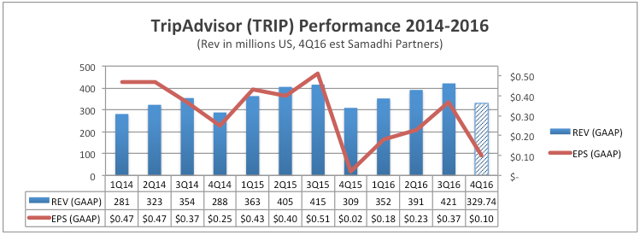

TripAdvisor's results have been significantly impacted by its business model transition. Starting in 2014 with mobile and mid-2015 on desktop, the company rolled out Instant Booking globally. Instant Booking provides (per TRIP) "hotels and B&Bs a powerful new booking channel enabling travelers to easily 'Book on TripAdvisor'" directly through the company website.

As a result, revenue growth decelerated to 19.7% in FY2015 (from 31.9% in FY2014), and continued to decelerate through 2016 (with a significant impact on EPS).

As shown in the chart below, TRIP's hotel segment revenue and margin profile have clearly been impacted since the transition started.

While Instant Book has impacted the company's business results, we believe this setback is temporary in nature. This is evidenced by data from its 3Q16 earnings report, where management noted positive y/y trends in the U.S. in each month throughout the quarter (September was the first full month of y/y Instant Booking comparison in the U.S.).

We believe TRIP is starting to see the light at the end of the tunnel, and the significant stock pullback in 2016 offers a compelling entry point for long-term investors who want to own one of the best assets in online travel.

Could TRIP be an acquisition target?

We also see the company as a potential acquisition target, presently ranked #7 on our 2017 Top 10 M&A Picks. TRIP itself has been through its share of M&A/divestiture activity since its founding in 2000, being acquired by IAC/Interactive (NASDAQ:IAC) in 2004, before spinning out from the Expedia (NASDAQ:EXPE) brand in 2011.

Who are the likely candidates? TRIP has a solid brand and fleet of partners that, we feel, make it an attractive property. From a slightly defensive perspective, Priceline (NASDAQ:PCLN) could be a likely contender, while from an expansion perspective, both Alphabet/Google (GOOG, GOOGL) and Amazon (NASDAQ:AMZN) could find substantial value.

For additional insight into our perspective on TRIP's acquisition value, see our Samadhi Brief discussion below:

Our Samadhi Index Ratings for TRIP are as follows (an explanation of the Samadhi Index Ratings can be found here):

- MLX (Moore's Law Index): 7.3 out of 10

- SMX (Samadhi Management Index): 6.6 out of 10

- BMX (Business Model Index): 6.5 out of 10

- CMX (Competitive Market Index): 7.7 out of 10

TRIP presently trades at $51.61 (52-week range: $45.63-71.69), with a market cap of $7.52 billion (a significant pullback off its highs of $108.66/share and $15.59 billion in 2014). The company is expected to report its 4Q 2016 earnings after the close on February 15, 2017.

Contributing Authors: Fred McClimans, more