Consensus Earnings Growth Doesn't Justify Share Price For Some Tech Bellwether Stocks

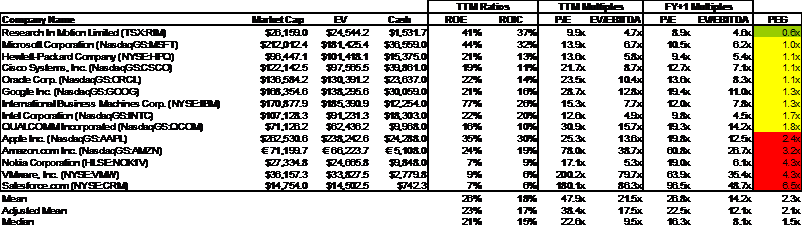

We have been seeing a lot of price justification related to Apple’s (NASDAQ:AAPL) recent climb to near the $300 level. Arguments abound that despite trading at a P/E multiple of 25.3x, AAPL is cheap on a fundamental basis due to its growth trajectory and its cash position. Based on comparative multiples, this may be a flawed argument. A classic method to test whether the market is pricing appropriately for future growth is to calculate the PEG ratio (price-to-earnings-growth). If a stock had a PEG ratio of 1.0x, investors should consider future earnings growth to be fully priced into the stock, and that its growth trajectory is “fairly valued”. Below 1.0x, there is a gap between the stock price and future earnings, and there is a buying opportunity. A PEG ratio above 1.0x infers that the market is overpaying for earnings growth.

We have ordered some technology bellwether stocks, based on the results of a PEG calculation using Capital IQ data from Friday. The only outright BUY based on earnings growth is Research In Motion (RIMM). A group of stocks including Microsoft (NASDAQ:MSFT), Hewlett Packard (NYSE:HPQ), Cisco (NASDAQ:CSCO), Oracle (NASDAQ:ORCL), Google (NASDAQ:GOOG), and IBM appear fairly priced, to slightly overvalued. Intel (NASDAQ:INTC), and Qualcomm (NASDAQ:QCOM) should be viewed more cautiously.

A group of stocks including Apple (AAPL), Amazon (NASDAQ:AMZN), Nokia (NYSE:NOK), VMware (NYSE:VMW) and Salesforce.com (NYSE:CRM) appear to priced well ahead of their future potential earnings growth capabilities, which suggests that the market appears to be ignoring the consensus estimates for FYE+1 earnings related to these stocks. A plausible argument could be that the market is expecting significant “surprise upside” to consensus earnings estimates.

With respect to a recent common argument that AAPL is undervalued if the cash balance is removed from P/E estimate, we calculated an EV/EBITDA multiple which excludes cash, debt and non-operating/non-cash expenses. In comparison to other bellwethers, AAPL could be considered overvalued at 13.6x EV/EBITDA versus the median among peer bellwethers, calculated at 9.5x. The median calculation removes mean skewing caused by outlying stocks like VMW and CRM.

The bottom line is that AAPL should be considered “toppy” at these levels because a lot of “surprise upside” to earnings is baked into the price based on the PEG ratio calculation. Often AMZN is used by people as a comparison to justify AAPL’s current share price. Comparing “toppy” to “toppier” is probably a risky proposition. In comparison to the median EV/EBITDA multiples, AAPL should be considered expensive by investors, along with CRM, VMW, and AMZN.

Global technology companies that derive most of their business from the enterprise such as ORCL, IBM, MSFT, HP, RIMM and CSCO, should be attractive at current multiples as they benefit from corporate investment in productivity, and natural replacement cycles. Although VMW and CRM fit into this category, there is a lot of speculation priced into these stocks.

AAPL is entering the realm of “cultural zeitgeist” where the share price trades on reputation, not on fundamentals. It could be a great time for savvy long investors to lock in some profits and sell their shares to hardcore AAPL fans. AAPL should not be compared favorably to AMZN, CRM, or VMW because these stocks are even more overbought based on typical earnings growth measurements like PEG ratio and EV/EBITDA multiples.

Companies that have a broad global client base within the enterprise sector look pretty good. RIMM is a fractured stock because of the incessant comparison of Blackberry to iPhone. To put it into car terms, it's like comparing Ford trucks to Porsche 911s. They are both very good products, but with different functionality for different markets. Despite some forays into consumer devices, RIMM is an enterprise solution, while iPhone is a consumer solution. And I haven't forgotten about GOOG's Android - which could ultimately become dominant as the engine and drivechain for a hundred other vehicles.

Disclosure: I do not own any shares discussed in this article.