You Were Warned: MLP’s & “I Bought It For The Dividend”

In early 2016, I warned investors about the dangers of Master Limited Partnerships (MLP’s) and chasing dividend yields. To wit:

“One of the big issues starting in 2016 will be the reversions of MLP’s. Many investors jumped into MLP’s believing them to be a ‘no-brainer’ investment for income with little or no price risk. As I have suggested many times over the last few years, this was ALWAYS a false premise. In 2016, many companies that spun-off pipelines in the form of MLP’s, will ‘revert’ them back into the parent company as they can buy the asset back very cheaply, boosting cash flows of the parent company, during a period of weak commodity prices. This will leave MLP investors who just ‘bought it for the dividend,’ receiving back much less than they invested to begin with.”

That prediction continues to come to fruition with the latest announcement by Tallgrass Energy Partners. Via Bloomberg:

“Tallgrass Energy GP, LP announced late on Monday it would buy out the public unit-holders owning about two-thirds of its master limited partnership, Tallgrass Energy Partners, LP. It’s the latest MLP to be shuffled off and a good example of why the ranks are thinning in this once-beloved corner of the market.

Tallgrass Energy Partners listed in 2013, when the combination of yield and growth — predicated on the resurgence in U.S. oil and gas production — offered by MLPs had them in high demand. The general partner, Tallgrass Energy GP, listed two years later, when oil’s bear market had started but MLPs hadn’t yet fallen out of favor. That followed soon after.”

The “yield” is the problem.

“Tallgrass actually avoided cutting its quarterly distributions in the downturn, making it a relatively rare beast and explaining much its outperformance. But those high distributions evidently didn’t inspire enough confidence — and just became a high cost of capital instead.”

But it isn’t just Tallgrass, but most MLP’s. The “yields” reflected by MLP’s are actually understatements of the true cost of equity. Once prices fall, both on the MLP and with the underlying commodity, the entire premise of “raising capital cheaply” gets called into question. It then becomes much more opportunistic to “revert” the MLP back into the parent company.

This is the point where a common“investment thesis” falls apart.

The Dangers Of “I Bought It For The Dividend”

“I don’t care about the price, I bought it for the yield.”

First of all, let’s clear up something.

Tallgrass Energy Partners pays out an annual dividend of $3.86 and is currently priced at $39.24 (as of this writing) which translates into a yield of 9..84%. (3.86/39.24)

Let’s assume an individual bought 100 shares at $50 in 2017 which would generate a “yield” of 7.72%.

Investment Return (39.24 – 50 = -10.76) + Dividend of $3.86= Net Loss of $6.90

“The terms — laid out in a perfunctory seven-slide deck — are as austere as you might expect in a deal where the limited partners don’t get to vote. The parent offered a nominal premium of about 1 percent to Tallgrass Energy Partners’ minority unitholders. The exchange ratio of two shares for each unit was essentially in line with the average since the general partner listed.”

That’s not a great deal, but better than a “sharp stick in the eye.”

Here is the important point. You do NOT receive a “yield.”

“Yield” is just a mathematical calculation.

The “yield” can, and often does, go away.

I previously posted an article discussing the “Fatal Flaws In Your Financial Plan” which, as you can imagine, generated much debate. One of the more interesting rebuttals was the following:

“‘The single biggest mistake made in financial planning is NOT to include variable rates of return in your planning process.’

This statement puzzles me. If a retired person has a portfolio of high-quality dividend growth stocks, the dividends will most likely increase every single year. Even during the stock market crashes of 2002 and 2008, my dividends continued to increase. It is true that the total value of the portfolio will fluctuate every year, but that is irrelevant since the retired person is living off his dividends and never selling any shares of stock.

Dividends are a wonderful thing, Lance. Dividends usually go up even when the stock market goes down.”

This comment drives to the heart of the “buy and hold” mentality and, along with it, many of the most common investing misconceptions.

Let’s start with the notion that “dividends always increase.”

When a recession/market reversion occurs the “cash dividends” don’t increase but the “yield” does as prices collapse. Well, that is until the cash dividend is cut or is eliminated entirely.

During the 2008 financial crisis, more than 140 companies decreased or eliminated their dividends to shareholders. Yes, many of those companies were major banks, however, leading up to the financial crisis there were many individuals holding large allocations to banks for the income stream their dividends generated. In hindsight, that was not such a good idea.

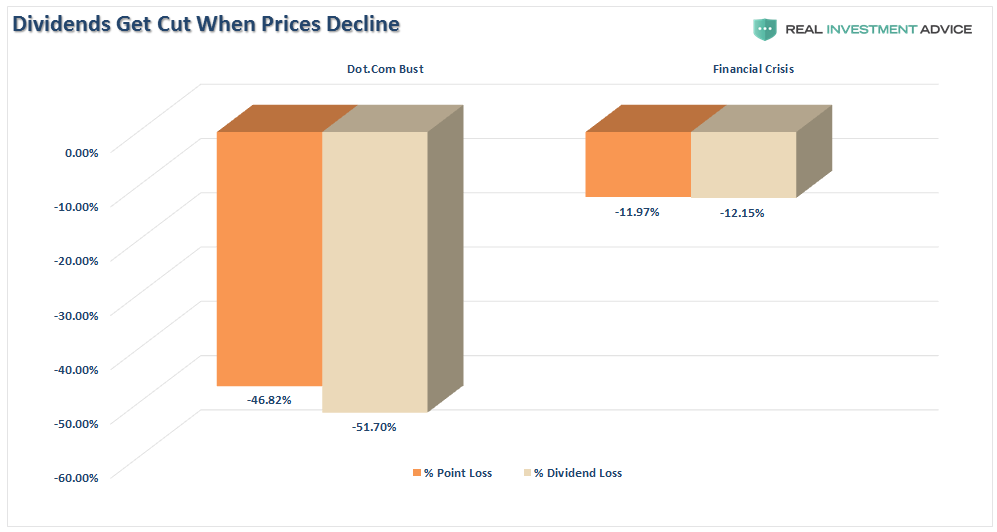

But it wasn’t just 2008. It also occurred dot.com bust in 2000. In both periods, while investors lost roughly 50% of their capital, dividends were also cut on average of 12%.

Of course, not EVERY company cut dividends by 12%. Some didn’t. But many did, and some even eliminated their dividends entirely, to protect cash flows and creditors.

Due to the Federal Reserve’s suppression of interest rates since 2009, investors have piled into dividend yielding equities, regardless of fundamentals, due to the belief “there is no alternative.” The resulting “dividend chase” has pushed valuations dividend yielding companies to excessive levels disregarding underlying fundamental weakness.

As with the “Nifty Fifty” heading into the 1970’s, the resulting outcome for investors was less than favorable. These periods are not isolated events. There is a high correlation between declines in asset prices and the actual dividends being paid out throughout history.

While I completely agree that investors should own companies that pay dividends (as it is a significant portion of long-term total returns), it is also crucial to understand that companies can, and will, cut dividends during periods of financial stress.

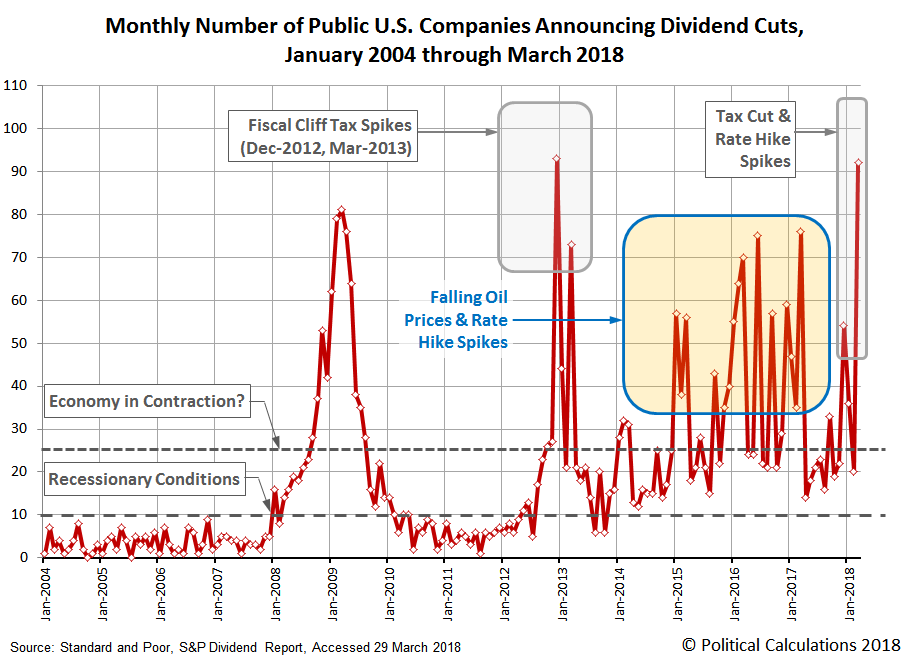

In fact, it is a good indicator of the strength of the underlying economy. As noted by Political Calculations recently, the economy may not be as “strong as an ox” currently:

“March 2018 saw the second-largest ever number of dividend cuts be declared by U.S. firms and funds in a single month. The month’s 92 dividend cuts reported was just one shy of the record 93 cuts that were recorded during the ‘Great Dividend Raid of 2012.””

Here are the dividend numbers as we know them for March 2018 today:

- There were 4,392 U.S. firms that issued some kind of declaration regarding their dividends in March 2018, which is up significantly from February 2018’s 3,493 and the year-ago March 2017’s 4,041. This figure is also the third highest number on record, coming behind December 2017’s 4,506 and December 2015’s 4,422.

- In March 2018, there were 36 U.S. firms that announced that they would pay an extra, or special, dividend. That figure is slightly down from the 38 firms that made similar declarations in both February 2018 and back in March 2017.

- 167 U.S. companies declared that they would increase their dividends in March 2018, which is down from 322 in February 2018, but up significantly from the 141 that boosted their dividends in March 2017. For the first quarter of 2018, a total of 807 dividend rises were recorded, which ranks third for any quarter’s total of dividend increases, behind March 2014’s 819 and March 2015’s 812.

- The 92 dividend cuts reported for March 2018 is up substantially from the 20 that were recorded in February 2018 and also from the 76 recorded back in March 2017, when the distress in the U.S. oil and gas industry was bottoming.

- 9 U.S. firms omitted paying dividends in March 2018, the same as in February 2018, but which is up from the 2 firms that did a year earlier in March 2017.”

During the next major market reversion, as prices collapse, so will the dividend payouts.

This is when the “I bought it for the dividend plan” doesn’t work out.

Why?

Because EVERY investor has a point, when prices fall far enough, that regardless of the dividend being paid they WILL capitulate and sell the position. This point generally comes when dividends have been cut and capital destruction has been maximized.

Psychology

Of course, while individuals suggest they will remain steadfast to their discipline over the long-term, repeated studies show that few individuals actually do.

Behavioral biases, specifically the “herding effect” and “loss aversion,” repeatedly leads to poor investment decision-making.

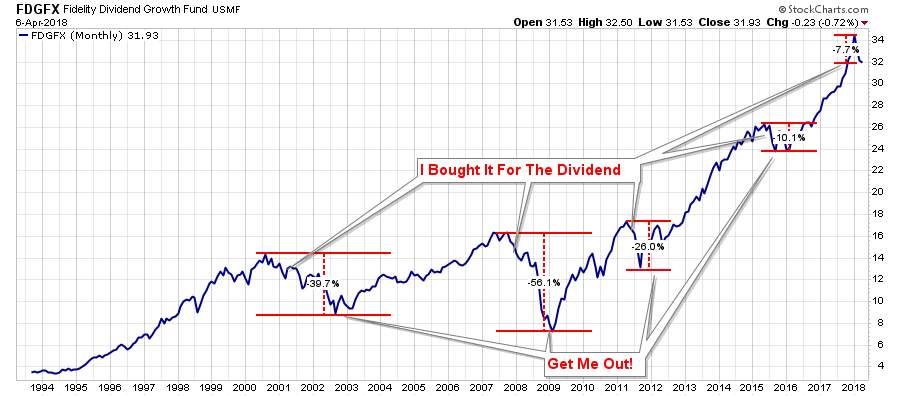

Ultimately, when markets decline, there is a slow realization “this decline” is something more than a “buy the dip” opportunity. As losses mount, so does the related anxiety until individuals seek to “avert further loss” by selling. It is generally believed that dividend yielding stocks offer protection during bear market declines. The chart below is the Fidelity Dividend Growth Fund (most ETF’s didn’t exist prior to 2000), as an example, suggests this is not the case.

As you can see, there is little relative “safety” during a major market reversion. The pain of a 38% loss, or a 56% loss, is devastating particularly when the prevailing market sentiment is one of a “can’t lose” environment. Furthermore, when it comes to dividend yielding stocks, the psychology is no different – a 3-5% yield and a 30-50% loss of capital are two VERY different issues.

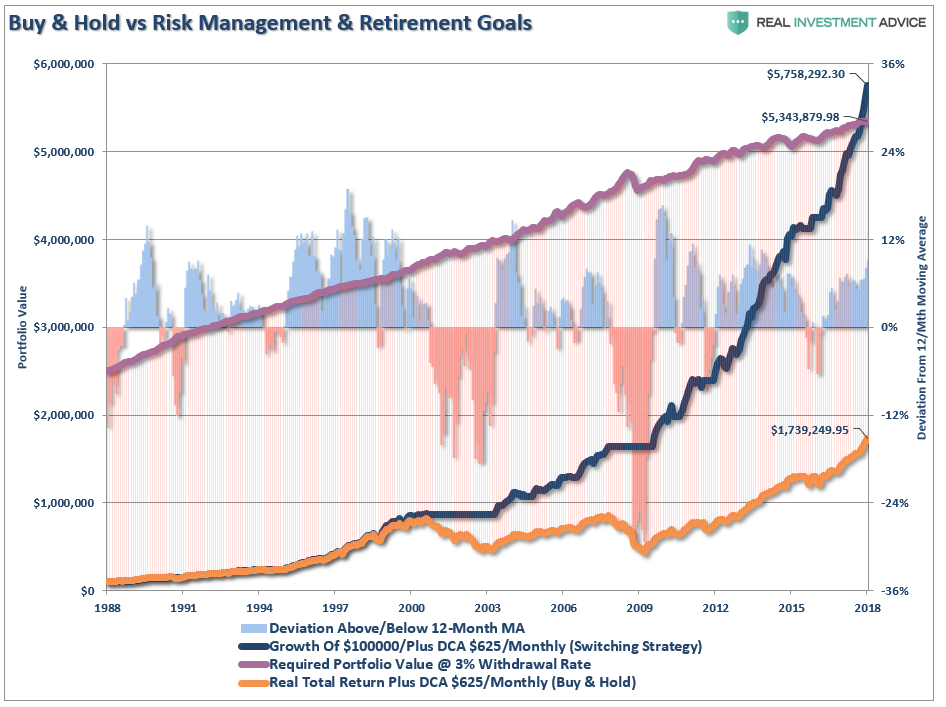

Buy & Hold Won’t Get You There Anyway

Most importantly, as it relates to this discussion, is the “fact” that “buy and hold” investing, even with dividends and dollar-cost-averaging, will not get you to your financial goals. (Click here for discussion of chart)

In the end, we are just human. Despite the best of our intentions, it is nearly impossible for an individual to be devoid of the emotional biases that inevitably lead to poor investment decision-making over time. This is why all great investors have strict investment disciplines that they follow to reduce the impact of human emotions.

While many studies show that “buy and hold", and “dividend” strategies do indeed work over very long periods of time; the reality is that few will ever survive the downturns in order to see the benefits. Furthermore, with valuations and market correlations at extremely elevated levels, the next major market correction will be equally unkind to all investors.

In the end, those who utter the words “I bought it for the dividend” are simply trying to rationalize an investment mistake. However, it is in the rationalization the“mistake” is compounded over time. One of the most important rules of successful investors is to “cut losers short and let winners run.”

Unfortunately, the rules are REALLY hard to follow. If they were easy, then everyone would be wealthy from investing. They aren’t because investing without a discipline and strategy has horrid consequences.

Tallgrass won’t be the last MLP, or corporation, to cut dividends. When the next major mean-reverting begins, you can “lie” to yourself for a while that you are fine with just the dividend. Eventually, when you have lost enough capital, and the dividend is cut or eliminated, you will eventually sell.

It happens every time.

But, you have been warned…again.

Disclosure: The information contained in this article should not be construed as financial or investment advice on any subject matter. Real Investment Advice is expressly disclaims all liability in ...

more