Yalla Group Limited’s (YALA) financial performances in the third quarter injected new energy into the company.

Image provided by Mentor Finance

Yalla is one of the leading companies in the Middle East and North Africa (MENA) area that has a voice-centric social network and entertainment platform. It operates two core products locally, Yalla and Yalla Ludo. Although the 21Q3 season did not show an exponential growth experienced in 21Q1, the company claims that the overall revenue increase and user expansion were maintained at a better level. "We achieved yet another quarter of strong growth, with good operating and financial performances." said Yang Tao, founder, chairman, and CEO of Yalla.

Headquartered in Dubai, UAE, Yalla Technology was founded in February 2018. In September 2020, after only two and half years, it was listed on the New York Stock Exchange. Compared to other voice-based social startups, Yalla claims that it has gained more market attention — owing to its geographical location.

Rapid Growth in the MENA Area

As a "follower" in terms of the adoption of mobile internet, the number of mobile users in the Middle East and North Africa demonstrated rapid growth in recent years. According to a 42-page report by GSMA in 2020, the number of independent mobile users in the Middle East and North Africa reached a milestone of 400 million in 2020, representing a penetration rate of 65% of the local population, with statistics that were even higher in some countries.

By 2025, 700 million people will have access to mobile internet services. As digital technology becomes more centered around daily life, more people in the Middle East and North Africa will enjoy the benefits of the Internet and smart devices.

Due to religious beliefs, cultural customs, and other factors in the Middle East and North Africa, in-person leisure activities are restricted, driving up the increasing demand for online entertainment. According to data from Hootsuite in July 2020, citizens in the UAE and Saudi Arabia, respectively, spend 3 hours and 17 minutes and 3 hours and 11 minutes on social media each day, which are both higher than the global average of 2.4 hours per day. By the time of the publication, the penetration rate for online social and entertainment in the MENA area is only 14%, still indicating areas for continued advancement.

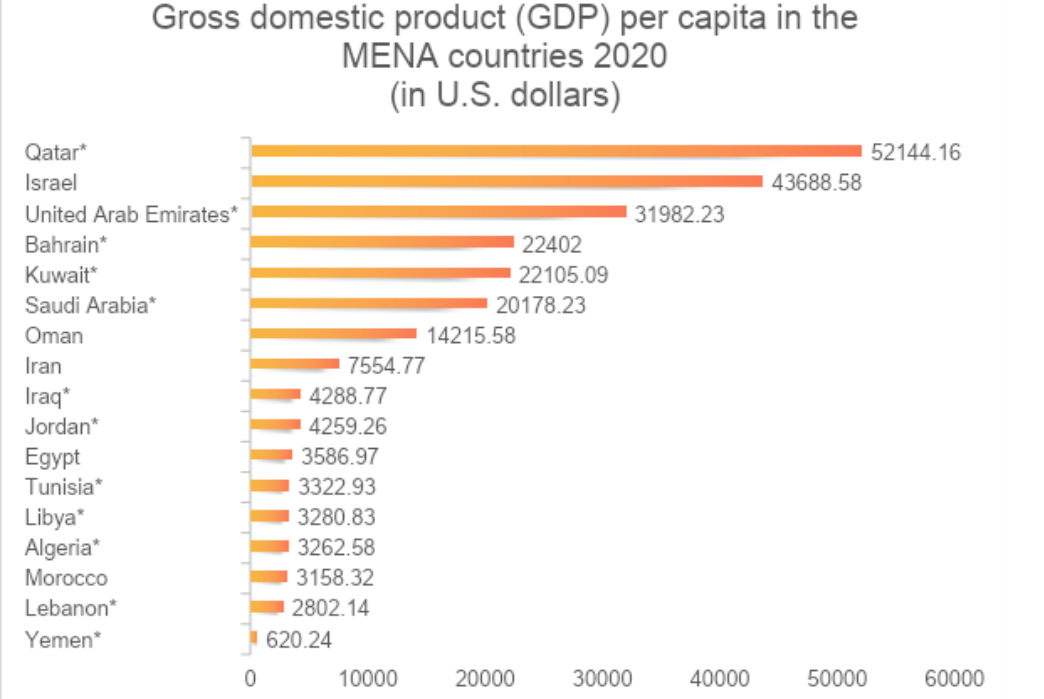

In terms of purchasing power, the major countries and regions in the MENA area are comparable to the Western and the Asia-Pacific nations. A report from The World Bank in July this year suggested that the urbanization rate of the Middle East and North Africa countries such as Kuwait, Qatar, Israel, etc., is close to 100%. These cities are highly developed and their resident income far outstrips all the other parts of the region. Thus, users in these areas have a strong purchasing power, providing a solid foundation for the development of local online entertainment products, with Yalla being one of the beneficiaries.

(Click on image to enlarge)

Glittering Performance

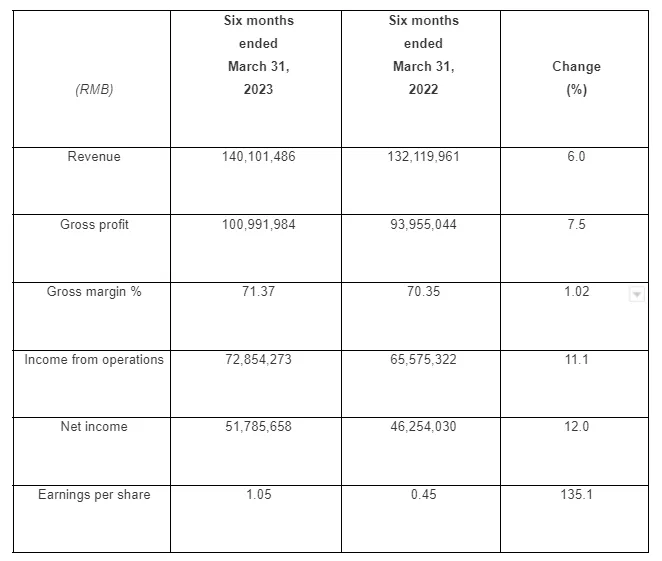

In the third-quarter earnings report, Yalla achieved a revenue of $71.3 million, a 110.8% increase compared to the third quarter of 2020. Chat service remains as the main revenue source for Yalla, totaling $53.9 million, while revenue from game service was $17.4 million, which mainly benefited from the increase in paying users brought by new products.

The net profit in the third quarter was $25.3 million, with a net profit margin of 35.5%. In comparison, there was a loss of $31 million in the same period last year due to equity incentives and other factors. Overall, the non-GAAP profit margin in the third quarter of 2021 was 46.6%.

In terms of users, Yalla group says it has maintained good growth. The average monthly active users (MAU) of 25.9 million was an 81.9% increase year-to-year compared to the 14.3 million users last year. The number of paying users increased from 5.1 million in the third quarter of 2020 to 7.7 million in the third quarter of 2021, achieving sustained growth for many quarters. Based on descriptions from conference calls, the management believes that the results from a series of marketing activities tailored to the local culture were reflected in the realization of user growth.

In the 21Q3 report, Yalla disclosed the operating data for its new product, Yalla Parchis. Yalla Prachis is a voice-based game platform targeting the South American market. It was officially launched in October and brought in 786,000 MAUs and 299,000 paying users for Yalla Group in the third quarter.

In terms of expenses, Yalla's total costs and expenses in the third quarter totaled $45.6 million, a decrease from the $64.7 million in the third quarter of 2020. With a continuous expansion of business scale, Yalla believes that its ability to control costs has been gradually improving. Among the expenses, technology and product development expenses were $3.9 million, accounting for 5.4% of the total revenue.

Based on the company’s strategic planning, the management is projecting revenue between $67 million and $72 million for the fourth quarter of 2021. This will be an increase of 38.6% to 48.9%, respectively, from the $48.3 million in the fourth quarter of 2020. It is worth noting that, according to Mr. Tao Yang, Yalla is developing a cutting-edge social application, Yalla Chat, which may be launched as early as the first quarter of next year in hope of becoming the first metaverse social application specifically customized for the MENA region.

Yalla's current price-to-earnings ratio (PE) is 60.73, which is at a lower range of the industry average, while its price-to-sales ratio (PS) is 4.40, which is down more than half from the historical average of 8.95. The significant drop has given Yalla a certain low valuation attribute. The China International Capital Corporation Limited (601995. SH) covered Yalla for the first time last week and gave it an outperforming rating. It is estimated that the company's EPS for 2021-23 will be 0.71, 0.77, and 1.01 US dollars, respectively, while the non-GAAP will be 19%.

Comments

Log in or sign up to join the conversation.