Welcome This Hospitality Leader To Your Portfolio

Another Quality Business Trading at a Historical Discount

Over the past several weeks, we’ve identified high-quality businesses in some of the industries most adversely impacted by the COVID-19 pandemic. While evaluating restaurants, malls, homebuilders, airlines, and even advertising agencies, we have found several hidden gems including SYSCO Corporation (SYY), Darden Restaurants (DRI), Cracker Barrel Old Country Store (CBRL), Simon Property Group (SPG), D.R. Horton (DHI), Southwest Airlines (LUV), and Omnicom Group (OMC).

Hyatt Hotels (H), with its leading profitability, strong balance sheet, and undervalued stock presents another excellent buying opportunity for investors willing to look beyond the current economic crisis.

Hyatt’s History of Profit Growth

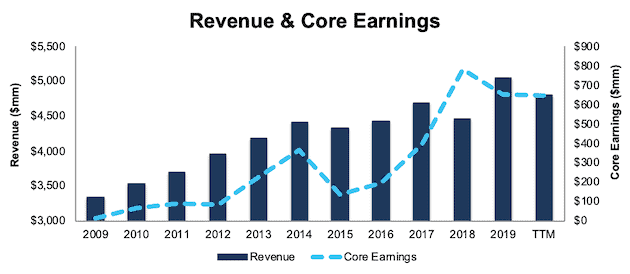

Hyatt has a strong history of generating consistent profits. Over the past five years, Hyatt has grown revenue by 3% compounded annually and core earnings[1] by 12% compounded annually, per Figure 1. Since 2009 (the year of H’s IPO), Hyatt has grown core earnings by 46% compounded annually. The firm increased its core earnings margin year-over-year (YoY) in seven of the past ten years and from less than 1% in 2009 to 13% TTM.

Figure 1: Hyatt’s Profitability Growth Since 2009

Sources: New Constructs, LLC and company filings.

Hyatt’s improving profitability helps the business generate significant free cash flow (FCF). The company generated positive FCF in eight of the past ten years (and each of the past six) and a cumulative $3.2 billion (71% of market cap) over the past five years. Hyatt’s $943 million in FCF over the TTM period equates to a 16% FCF yield, which is significantly higher than the Hotels & Entertainment Services Industry average of 2%.

We note that this stock currently gets our Neutral rating, largely due to the impact of the dramatic decline in revenue and profitability in 1Q20 on trailing-twelve-month (TTM) results. We expect financial performance will get worse before it gets better, and our Risk/Reward rating could get even worse.

However, we believe Hyatt has the balance sheet to survive and operational superiority to emerge from this crisis as an even strong company.

Hyatt’s Balance Sheet Provides Plenty of Time for a Recovery

There’s no doubt that Hyatt will face tough financial times in the future. Industry experts are projecting a ~51% decline in revenue per available room (RevPAR) – a key performance metric for the hotel industry – in 2020.

But, Hyatt’s large cash reserve and newly issued debt provide the liquidity it needs to survive the expected economic decline – and then some.

On April 21, 2020, the firm issued $900 million worth of senior notes. Subsequent to the issuance of the notes, Hyatt paid down $350 million outstanding on its revolving credit facility, which gives the firm access to the full $1.5 billion borrowing capacity. When combined with existing cash on hand, Hyatt has over $3.1 billion in available liquidity.

During its earnings call, the firm estimated that its monthly cash burn was $90 million not including the payment of its next debt maturity in 3Q21. At this monthly burn rate and after retiring its 3Q21 debt, Hyatt could operate for over 30 months before exhausting its credit facility and cash on hand.

To further enhance its liquidity, the firm reduced capital expenditures, suspended share repurchases and dividends, and recently announced layoffs and reduced pay across its operations. Lastly, Hyatt noted in its earnings call that its monthly selling, general and administrative (SGA) costs are $16 million and monthly capital expenditures are over $10 million. Should operating conditions worsen, Hyatt could eliminate investment spending, cut SG&A expenses by, say, an additional 10%, and reduce its spend by $12 million a month.

In a worst-case scenario where Hyatt generates no revenue for an extended period, the firm could operate at the afore-mentioned reduced spending level for at least 36 months.

Superior Profitability Matters Even More When the Economy Recovers

COVID-driven disruptions may drive some weaker hotel operators out of business for good. As a survivor, Hyatt’s superior profitability positions it to take the market share lost by weaker operators and return to its pre-crisis profit growth when the economy recovers.

Hyatt’s net operating profit after-tax (NOPAT) margin of 14% ranks highest among the three largest (by revenue) hotels, which include Marriott International, Inc. (MAR), Hilton Worldwide Holdings Inc. (HLT), and Hyatt.

High margins and rising invested capital turns drive Hyatt’s leading return on invested capital (ROIC). Per Figure 2, Hyatt’s current ROIC of 11% is well above both of its peers.

Figure 2: Superior Profitability vs. Competitors

Sources: New Constructs, LLC and company filings.

Unless you believe that there will be no hotels at all in the post-COVID world, it’s hard to argue against Hyatt’s ability to survive. And, if it survives, it’s hard to argue that the firm’s superior profitability before the crisis will not translate into market share and profit growth after the crisis.

Well-Positioned for Continued Growth

Hyatt has a proven track record of taking and keeping market share. The firm has grown total rooms from 116,000 in 2008 to 226,000 in 2019, or 6% compounded annually. In 2019 alone, Hyatt grew net rooms by 7.4%, which outpaces competitors Hilton (6.6%) and Marriott (4.9%).

Despite its success in implementing its expansion strategy, Hyatt has plenty of room to grow. In its 2019 10-K, Hyatt noted that “the recognition of our brands and our reputation for service is larger than the scale of our presence around the world, and therefore, we have a unique opportunity to grow.” Since 2009, the firm has taken advantage of this opportunity to expand into 281 new markets and 24 new countries. In 2019, the firm added 35 new markets to its portfolio. At the end of 2019, Hyatt had executed management or franchise contracts with ~500 hotels in its development pipeline, which means the firm expects to add 101,000 rooms (45% of total rooms in 2019) at some point in the future.

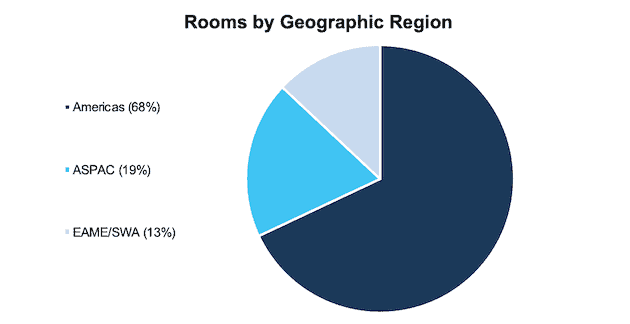

Per Figure 3, Hyatt provides rooms across the globe in three geographical regions, the Americas, Asia Pacific (ASPAC), and Europe, Africa, the Middle East, and Southwest Asia (EAME/SWA).

Figure 3: Hyatt’s Global Presence

Sources: New Constructs, LLC and Investor Presentation

Hyatt’s present geographic diversification allows the firm to participate in economic recoveries across the world as various markets reopen and is not entirely dependent upon the United States fully reopening.

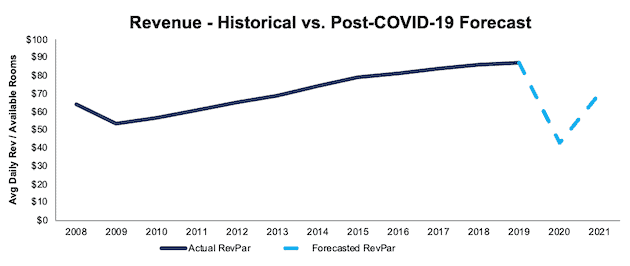

Hotel Industry Expected to Rebound

We believe the current drop off in economic activity is temporary, even if prolonged, and expect the hotel industry to recover over the long term. Recent forecasts project U.S. RevPAR to fall ~51% in 2020 before increasing by ~63% in 2021. Figure 4 shows RevPAR from 2008 to 2019 along with the expected drop to $43 in 2020 with a recovery to $70 in 2021.

Figure 4: Revenue Per Available Room (RevPAR) – U.S. Hotel Industry

Sources: New Constructs, LLC and STR.

Furthermore, the International Monetary Fund (IMF) and nearly every economist in the world believe the global economy will grow strongly in 2021. The IMF estimates the global economy will expand by 5.8%, and the U.S. economy by 4.7%, in 2021. The overall growth in the economy should lead to a rebound in the hotel industry as consumers escape the confines of their neighborhoods and enjoy leisure travel once more.

Encouraging Signs Rising from the East

Hyatt is already seeing signs of a recovery in its Greater China market. At its highest point in the first quarter, 26 of Hyatt’s hotels in China had suspended operations. At the time of its latest earnings call, that number had fallen to just one. Hyatt’s occupancy in the Greater China market is improving too, and reached nearly 25% at the end of April. For context, Hyatt mentioned in its 1Q20 earnings call that breakeven occupancy levels for some of their lower-labor cost international markets is around 30% to 35%.

China also recently celebrated its five-day May Day holiday from May 1 to May 5. While the total number of trips was down 41% from the prior year, there was plenty of demand at Hyatt’s hotels as several of its properties sold out. According to Hyatt CEO Mark Hoplamazian, the strong May Day showing, “validates what we expect to see elsewhere, which leisure and drive-to markets will lead.”

If leisure does in fact lead a recovery, Hyatt is well-positioned to benefit. In 2019, 73% of Hyatt’s system-wide room nights sold came from “transient” guests, or individuals traveling for business or leisure. While it may take longer for conferences and group activity (27% of room nights sold in 2019) to recover, a May-Day-type response in newly reopened markets worldwide could be welcome news for Hyatt.

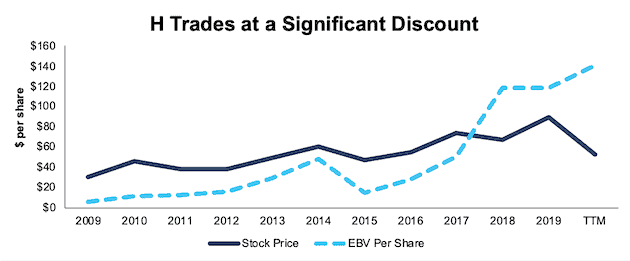

H Trades at Cheapest Level in History

After falling 50% YTD to $44/share, H now trades at its cheapest PEBV ratio (0.3) in the history of our model. This ratio means the market expects Hyatt’s NOPAT to permanently decline by 70%. This expectation seems overly pessimistic over the long term.

Hyatt’s current economic book value, or no-growth value, is $139/share – a 216% upside to the current price.

Figure 5: Stock Price vs. Economic Book Value (EBV)

Sources: New Constructs, LLC and company filings.

Current Price Implies Permanent Economic Downturn

Below, we use our reverse DCF model to quantify the cash flow expectations baked into H’s current stock price. Then, we analyze the implied value of the stock based on different assumptions about COVID-19’s impact on the hotel industry and Hyatt’s future growth in cash flows.

Scenario 1: Using recent projections for revenue declines, historical margins, and average historical GDP growth rates, we can model the worst-case scenario already implied by H’s current stock price. In this scenario, we assume:

- NOPAT margins fall to 2% (all-time company low in 2009, vs. 14% TTM) from 2020-2024 before rebounding to 7% (company average since 2009) in 2025 and each year thereafter

- Revenue falls 50.6% in 2020 and grows 63.1% in 2021 (in line with recent U.S. revenue decline projections)

- Revenue grows 3.5% in 2022 and each year thereafter, which equals the average global GDP growth rate since 1961

In this scenario, where Hyatt’s NOPAT declines 34% compounded annually from 2019 to 2024 and 9% compounded annually over the next eight years, the stock is worth $45/share today – slightly above the current stock price. This scenario accounts for the debt issuance and repayment of its credit facility since the end of 1Q20 noted earlier. We assume this capital will be used to cover operating expenses and do not treat it as excess cash. See the math behind this reverse DCF scenario.

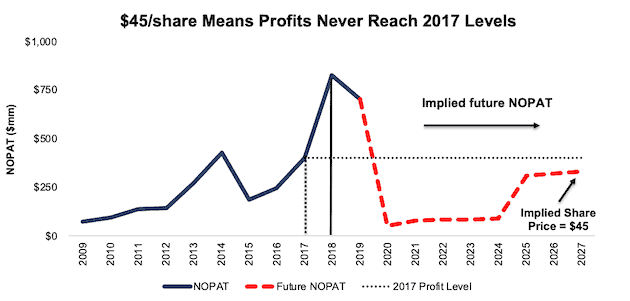

Figure 6 compares the stock’s implied future NOPAT to the firm’s historical NOPAT in this scenario. This worst-case scenario implies Hyatt’s NOPAT eight years from now will be 53% below its 2019 NOPAT. In other words, this scenario implies that eight years after the COVID-19 pandemic, Hyatt’s profits will have only recovered to ~2017 levels. In any scenario better than this one, H holds significant upside potential, as we’ll show in scenario 2.

Figure 6: Current Valuation Implies Severe, Long-Term Decline in Profits: Scenario 1

Sources: New Constructs, LLC and company filings.

Scenario 2: Long-term View Could Be Very Profitable

If we assume, as does the IMF and nearly every economist in the world, that the global economy rebounds and returns to growth starting in 2021, H is highly undervalued.

In this scenario, we assume:

- NOPAT margins fall to 2% (all-time company low vs. 14% TTM) in 2020 and 2021 and increase to 9% (below five-year company average of 10%) in 2022 and each year thereafter

- Revenue falls 50.6% in 2020 and grows 63.1% in 2021 (in line with recent U.S. revenue decline projections)

- Revenue grows 3.5% in 2022 and each year thereafter, which equals the average global GDP growth rate since 1961

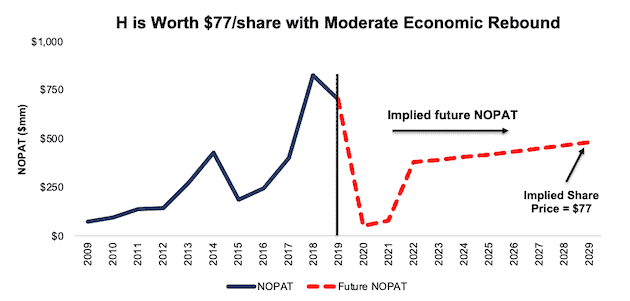

In this scenario, Hyatt’s NOPAT falls 93% in 2020 and 4% compounded annually over the next decade, and the stock is worth $77/share today – a 75% upside to the current price. This scenario also accounts for the debt issuance and repayment of its credit facility since the end of 1Q20 noted earlier. We assume this capital will be used to cover operating expenses and do not treat it as excess cash. See the math behind this reverse DCF scenario.

For comparison, Hyatt has grown NOPAT by 10% compounded annually over the past five years and 26% compounded annually over the past decade.

It’s not often investors get the opportunity to buy an industry leader at such a discounted price.

Figure 7 compares the stock’s implied future NOPAT to the firm’s historical NOPAT in scenario 2. This scenario implies that ten years from now, the firm’s NOPAT will be just 19% greater than its 2017 NOPAT and 32% below its 2019 level. If the firm’s profits return just to the 2019 level, H has even more upside potential.

Figure 7: Implied Profits Assuming Global Recovery Starts in 2021: Scenario 2

Sources: New Constructs, LLC and company filings.

Sustainable Competitive Advantages Will Drive Shareholder Value Creation

Here’s a summary of why we think the moat around Hyatt’s business will enable it to continue to generate higher NOPAT than the current market valuation implies. The following competitive advantages help Hyatt survive the downturn and return to growth as the economy grows again:

- Ample liquidity to survive the dip

- Net rooms growth outpacing main competitors

- Superior profitability to its main competitors

What Noise Traders Miss with Hyatt

These days, fewer investors focus on finding quality capital allocators with shareholder-friendly corporate governance. Instead, due to the proliferation of noise traders, the focus is on short-term technical trading trends while high-quality fundamental research is overlooked. Here’s a quick summary of what noise traders are missing:

- Consistent core earnings growth over the past decade

- Hyatt’s brand recognition exceeds its current geographic presence

- Valuation implies the hotel industry never recovers from COVID-19

Dividend and Buybacks Suspended in the Near-Term

Hyatt recently suspended its share repurchases and quarterly dividends through the first quarter of 2021 to maintain a stronger cash balance.

Hyatt began paying dividends in 2018 and since then has generated far more in free cash flow ($1.9 billion) than it paid out in dividends ($148 million), which is an average $861 million surplus each year. It’s latest quarterly dividend, when annualized, equaled $0.80/share or a 1.8% dividend yield.

Firms with cash flows greater than dividend payments have a higher likelihood to maintain and grow dividends. While Hyatt has suspended its dividend in the short term, investors buying at current prices could get a nice yield with upside potential if Hyatt reinstates the dividend over the long term.

In addition to dividends, Hyatt historically returned capital to shareholders through share repurchases. Hyatt has repurchased $3.2 billion worth of shares since 2014 (71% of current market cap). Prior to the suspension, Hyatt had an additional $928 million remaining under its current authorization. Should the firm resume share repurchases, the yield for investors will only increase.

A Consensus Beat or Signs of Recovery Could Send Shares Higher

According to Zacks, consensus estimates at the end of January pegged Hyatt’s 2020 EPS at $1.76/share. Jump forward to May 13, and consensus estimates for Hyatt’s 2020 EPS have fallen to -$2.95/share.

Though the COVID shutdowns are crushing near-term profits, these lowered expectations provide a great opportunity for a strong business, such as Hyatt, to beat consensus, if not this quarter, then maybe the next. Though our current Earnings Distortion Score for Hyatt is “In-Line”, the firm beat EPS estimates in 11 of the past 12 quarters, and doing so again, in the midst of such market turmoil, could send shares higher.

Additionally, any signs of a recovery in RevPAR, or consumer interest in hotels, such as the recent demand in China, would send shares higher.

Executive Compensation Plan Could Be Improved

No matter the macro environment, investors should look for companies with executive compensation plans that directly align executives’ interests with shareholders’ interests. Quality corporate governance holds executives accountable to shareholders by incentivizing them to allocate capital prudently.

In fiscal 2019, 55% to 90% of Hyatt’s executive target pay mix was linked to its long-term incentive performance (LTIP) program. 40% to 50% of the named executive officers’ (NEO’s) LTIP was in the form of performance share units (PSUs) tied to a return on gross assets (ROGA) goal and a managed and franchised adjusted EBITDA goal.

Hyatt defines ROGA as Adjusted EBITDA divided by Average Gross Assets for each year of a three-year performance period. While we applaud Hyatt for linking executive performance to a measure of profitability, we would still prefer the firm use an accurate ROIC calculation as there is a strong correlation between improving ROIC and increasing shareholder value. Having accurate values for NOPAT and invested capital closes accounting loopholes and ensures management is accountable for every dollar invested into the company over the entirety of its life.

Despite using flawed metrics for measuring performance, Hyatt’s plan has not compensated executives while destroying shareholder value. Hyatt grew economic earnings by 34% compounded annually over the past five years.

Insider Trading and Short Interest Trends

Over the past twelve months, insiders have bought a total of ~3.0 million shares and sold ~2.6 million shares for a net effect of 364 thousand shares purchased. These purchases represent less than 1% of shares outstanding.

There are currently 4.4 million shares sold short, which equates to 13% of shares outstanding and over 2 days to cover. Short interest is up 28% from the prior month. The high short interest increases the chances of a short squeeze should Hyatt report good guidance and/or an earnings beat.

Critical Details Found in Financial Filings by Our Robo-Analyst Technology

As investors focus more on fundamental research, research automation technology is needed to analyze all the critical financial details in financial filings as shown in the Harvard Business School and MIT Sloan paper, "Core Earnings: New Data and Evidence”.

Below are specifics on the adjustments we make based on Robo-Analyst findings in Hyatt Hotels Corp’s 2019 10-K:

Income Statement: we made $404 million of adjustments with a net effect of removing $62 million in non-operating income (8% of revenue). See all adjustments made to Hyatt’s income statement here.

Balance Sheet: we made $2.1 billion of adjustments to calculate invested capital with a net decrease of $1.0 billion. One of the most notable adjustments was $450 million (6% of reported net assets) in deferred compensation assets. See all adjustments to Hyatt’s balance sheet here.

Valuation: we made $3.7 billion of adjustments with a net effect of decreasing shareholder value by $1.4 billion. Apart from total debt, the most notable adjustment to shareholder value was $32 million in outstanding ESOs after tax. This adjustment represents 1% of Hyatt’s market cap. See all adjustments to Hyatt’s valuation here.

Attractive Funds That Hold H

The following fund receives our Attractive rating and allocates significantly to Hyatt Hotels Corp.

- Invesco Gl Responsibility Equity Fund (VSQFX) –1.6% allocation

[1] Our core earnings are a superior measure of profits, as demonstrated in In Core Earnings: New Data & Evidence a paper by professors at Harvard Business School (HBS) & MIT Sloan. The paper empirically shows that our data is superior to “Income Before Special Items” from Compustat, owned by S&P Global (SPGI).

Disclosure: David Trainer, Kyle Guske II, and Matt Shuler receive no compensation to write about any specific stock, style, or theme.