U.S. Long Rates Low For Longer – DJIA Price To Continue “Cooking With Gas”

Summary

U.S. inflation remains moribund as massive increases in monetary base have failed to flow through to real economy resulting in a collapse in the Velocity of Money and thus the potential for inflation.

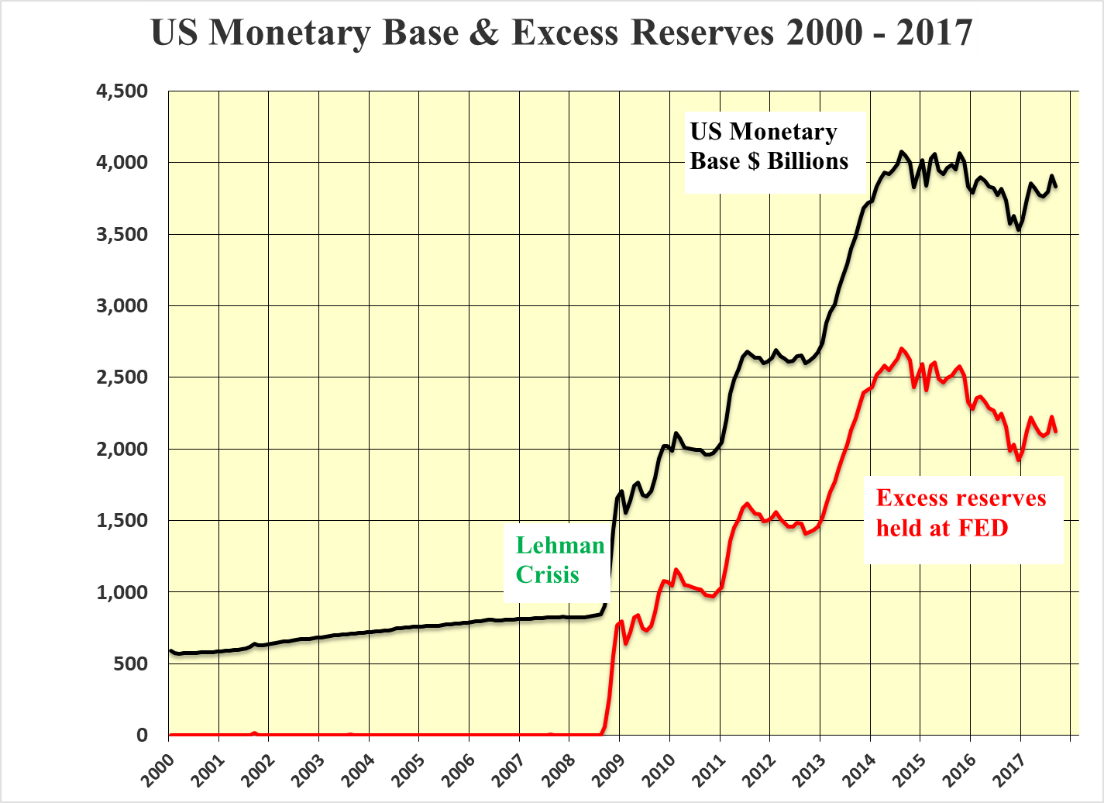

Combination of fear and contradictory action by congress have led to build up of excess reserves of $2.25 trillion.

Excess reserves effectively sterilized by the Fed paying interest.

DJIA continues “cooking with gas”

Unintended Consequences of Glass Steagall Repeal

The repeal of the Glass Steagall Act in 1999 enabled banks to trade for their own account for the first time since the Act was introduced in 1933. This was the critical change to the entire banking system and the real birth of Transactional Banking. The nature of banking changed more towards trading for the banks own profit rather than lending money into the economy on a relationship basis, which creates jobs.

Following Lehman, quantitative easing by the Fed pushed the monetary base up five-fold from $0.8 trillion to $4 trillion. However, there was no commensurate rise in the GDP. It is, thus, little wonder that Money Velocity has collapsed.

Equation of Money Velocity:

MV = GDP/QM

MV = Money Velocity

GDP = Nominal Gross Domestic Product

QM = Monetary Base, M1, or M2

The rise of the numerator, GDP, in the equation has been swamped by the staggering jump in the denominator, whether that be the monetary base, M1 or M2. The net result is the drop in the velocity of money.

The rise in the monetary base, which would have historically moved into the economy under the old relationship banking method, has been diverted by the big money centre banks for the purpose of trading. Initially the recession reduced the demand for money at a time when the Fed was acting in desperation to re-liquefy the entire banking system.

As this was happening, fear and banking regulatory changes reduced the willingness and ability of banks to increase their lending. The fractional banking issue applies to lending but not to trading. Hence, money failed to flow into the real economy just at the time it was most needed.

Simultaneously, Congress introduced legislation to protect consumers, which effectively rolled back the repeal of the Glass Steagall Act and reduced the ability of banks to trade. Caught in the middle of the Fed pushing on the proverbial string and regulatory changes banks have built up $2.25 trillion of excess reserves which are parked at the Fed. This is money not being lent on into the economy, which further reduces the fractional banking ratio and thus the velocity.

The money that banks are simply parking are garnering a return of 1.25% pa, which in today’s low interest environment is a much higher reward at a much lower risk than could be had by lending into the economy. Given this Money Velocity could remain low for a long time and inflation may remain elusive.

With the Volker Rule and the rest of the Dodd Frank Act moving backwards toward the effective re-imposition of Glass Steagall and President Trump wanting its repeal, is it any wonder that the banks are reluctant to let go of their nice little excess reserve annuities until the dust settles?

Possible Solution

A solution to this conundrum may be the elimination of the deposit rates. At which point the banks should return to relationship banking and push money out into the real economy. It will take a considerable time to redirect this super-tanker of excess reserves. Hence, Money Velocity should only pick up gradually and inflation should remain persistently low, much to the continued puzzlement of Chair Yellen and the rest of the Fed.

There is also the problem of the huge amount of debt sloshing around the world that central banks may well have to maintain their easy-money policies to enable the continued ability to service such debt. This, itself, is an argument for continued low long term rates.

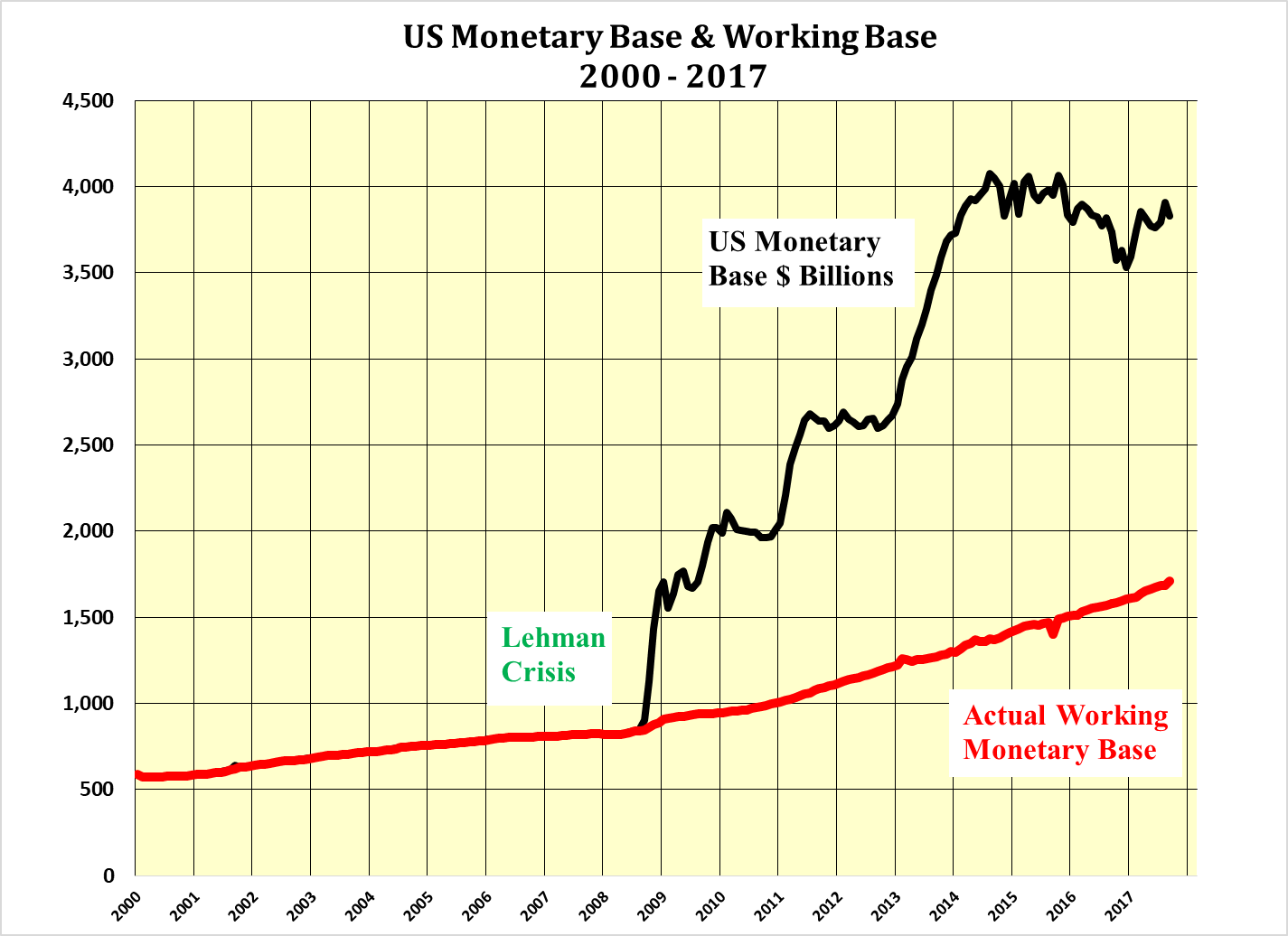

GDP Growth more in line with rise in Actual Working Monetary Base

Subtracting the excess reserves from the monetary base shows the actual working monetary base (AWMB). This seems more in keeping with the much slower than expected rise in GDP experienced since the great recession.

Elimination of the deposit rate that was implemented in 2008 can only be carried out gradually to avoid a wall of money flooding into the real economy and reigniting inflation on a massive scale. In previous reports it was proffered that a slow reduction of the deposit rate to discourage the parking of excess reserves combined with the hiking of the Fed Funds rate could make other short term investments in the relationship banking arena more attractive to the banks.

This gives the Fed the ability to raise the Funds rate back to whatever level is considered normal without reducing the AWMB, in fact this should continue to rise as excess reserves move into the real economy through increased relationship banking.

Should the economy weaken unexpectedly the Fed could always lower the Funds rate without adding to the monetary base. The Fed is thus empowered with two levers to control the economy and inflation, the Funds rate and the deposit rate. Until the AWMB rises to the point where excess reserves are eliminated then the Fed should be able to reduce its balance sheet without any deleterious economic impact.

DJIA continues “cooking with gas”

With earnings recovering and dividends with a payout ratio of 46% standing at a record level of $510.11 the price of the DJIA at 22,558 remains at a 45% discount to its dividend discount value of41,058. With low inflation and oodles of money seeking yield it would appear doubtful that the U.S. 30 year T Bond yield will rise significantly anytime soon. The DJIA thus offers a far higher after-tax yield than long bonds today and with the prospect of a rising dividend in the year to come there would seem no alternative for investors in publicly traded securities, with ability to do so, but to buy the DJIA.