The Unknowns Can Derail Past Conclusions

An important factor associated with writing blog content is it serves as a written record of one's thinking at certain points in time. It is often beneficial to go back and review one's thoughts and conclusions at these various points in time. If the conclusions that are drawn from one's writings turn out to be different than what was expected, understanding why is important going forward.

I was curious about some of the conclusions in the blog in September last year as the market was reaching new highs. Knowing that stocks do not know what day or month it is during calendar years, seasonality plays a role in market return due to investors' influence in the market. With this noted, August and September tend to be volatile down market periods and I sometimes write about this seasonality at this time of the year. As fate would have it, I did not write about the seasonality in 2018.

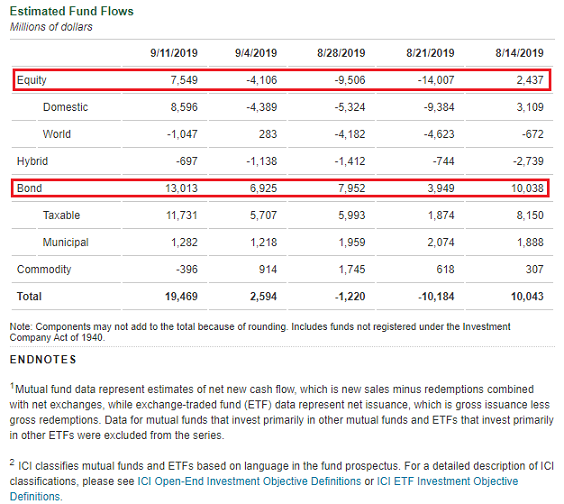

What was noted in my last post in September 2018 was the fact investment flows into bond and equity funds and ETF's had increased. Specifically, equity flows turned positive in the next to last week of September after being negative in the four prior weeks. Today, for the week ending September 18, Lipper reports, "All asset groups were on the plus side for the week, paced by equity funds (+$6.0 billion) and followed closely by money market funds (+$5.4 billion) and taxable bond funds (+$4.1 billion). Municipal bond funds extended their streak of consecutive net inflows to 37 weeks as the group had net positive flows of $209 million." ICI reports flows as well, but with a one week lag. Their reporting is showing similar flow data for the week ending September 11.

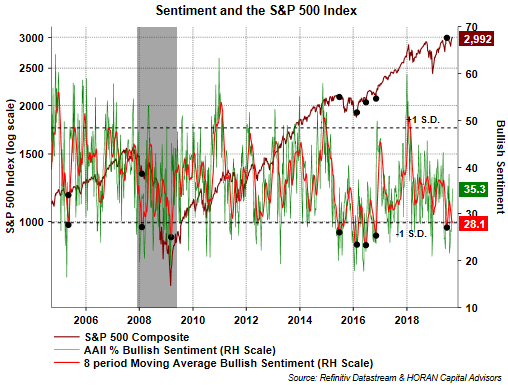

Also in the post from last year I commented on the fact individual investor sentiment seemed more balanced/neutral with bullish sentiment at that time equaling 36.2%. Today bullish sentiment is nearly the same at 35.3%. However, the eight-period moving average of the bullish sentiment is much less bullish today at 28.1% versus the 37.3% last year at this time. As a contrarian indicator, the low level of bullishness today would be a bullish signal for stocks.

The conclusion of my post at the end of September 2018 was, "In my view, with a balanced sentiment level, relatively strong returns in the current quarter and strong recent equity inflows, this might be an environment suggestive of more positive equity inflows in the weeks ahead as well. This would serve as a tailwind for stocks all else being equal." A similar conclusion based solely on these two variables might be made today.

As one remembers, and can see below, the market began a significant selloff a week later that ran through most of the fourth quarter.

The cause of the sell-off seemed to be precipitated by a comment made by Federal Reserve Chairman Jerome Powell in a PBS interview on October 3. In that interview, the Fed Chair responding to a question stated, “Interest rates are still accommodative, but we’re gradually moving to a place where they will be neutral,” he added. "We may go past neutral, but we’re a long way from neutral [emphasis added] at this point, probably." This comment occurred at a time some economic data was indicating a slowing environment was unfolding. Additionally, the Fed had increased rates eight times over a two and a half year period at a near uninterrupted pace. In my view, the economy did not have a chance to adjust to the higher rate regime.

In summary, fund flows and sentiment are at similar levels today. With this stated, there is value in going back and reviewing one's thinking and conclusions. In this case, when looking at year ago writings and conclusions, a valuable lesson centers around the unknown. In fact, it is often those unknown events that can trigger a market selloff or increase, like Jerome Powell's interest rate comment. Because of the negative impact unknown events can have on the market, one should be comfortable with their asset allocation in case an unknown event occurs that causes the market to decline. Ideally, investors do not want to be in a position where they are forced to sell stocks when the stocks or investments are down.