The Street Debates Monster Beverage's Quarter

Monster Beverage Corp (MNST) reported a top-and-bottom line beat in its first quarter results but some Street analysts remain convinced a bullish stance on the stock can be justified.

The Analysts

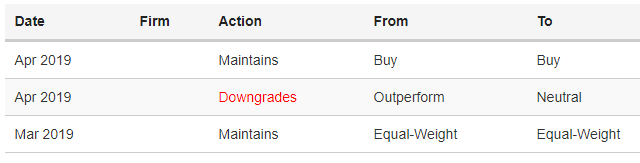

Stifel's Mark Astrachan maintains a Buy rating on Monster Beverage's stock with a price target lifted from $67 to $69.

Wells Fargo's Bonnie Herzog maintains at Market Perform, price target lifted from $53 to $56.

UBS' Sean King maintains at Sell, price target lifted from $50 to $53.

Credit Suisse's Kaumil Gajrawala maintains at Outperform, price target lifted from $75 to $77.

BMO Capital Markets' Amit Sharma maintains at Market Perform, unchanged $62 price target.

Monster's stock traded higher by 8.6 percent at $62.97 per share Friday afternoon.

Stifel: Q1 'Refutes' Bears

Monster reported strong earnings with multiple metrics that "refutes much of the current bear thesis," Astrachan said in a research report. Domestic sales rose 9 percent and organic sales were up around 4-5 percent. The company did see a benefit from the launch of Reign while the legacy business "remains healthy."

The company's legacy brand saw an estimated 28 percent increase in sales internationally and this level of growth is consistent with 2016 to 2018 levels. The analyst said the international market remains a notable long-term opportunity as the company holds an estimated 9-percent market share of the global drink market.

Gross margin improved sequentially to 60.6 percent and there is room for continued upside from benefits of pricing, improving input cost pressure and a more favorable mix from higher-margin products.

Wells Fargo: Reasons To Stay Cautious

Five factors continue supporting a neutral stance on the stock, Herzog said. These include:

- Ongoing concerns that pricing is "not fully sticking";

- Competition from a combination of legacy and new brands;

- It's unclear what The Coca-Cola Co (KO)'s "end game" is after the launch of an energy drink in Europe while arbitration is ongoing in the U.S.;

- Margin upside looks limited moving forward as faster growth in lower margin markets are dilutive; and

- The stock is "not cheap" at 25.5 times fiscal 2020 P/E.

UBS: Got Some Things Wrong

King said UBS underestimated the advanced Reign and Ultra shipments and the potential of the new products in the international market. Meanwhile, part of the strength in the first quarter could be attributed to advanced shipments ahead of Brexit and "strategic sales" ahead of Coke Energy.

The company did report a 15.6-percent growth in April, but the analyst said this could be attributed to an extra selling day and launch shipments. Excluding certain factors, it's likely overall growth was at or below industry levels.

Credit Suisse: Innovating In A Challenging Environment

Monster's report shows the company combined innovation, distribution and its balance sheet to exceed expectations despite a challenging environment, Gajrawala said. Reign looks like it saw a successful launch as it gained 2.5-percent market share in just five weeks.

The energy drink market should see a mid-single-digit U.S. category growth expansion and Monster should perform better than average, the analyst wrote. Outside of the U.S., the market is twice the size and growing twice as fast, which adds another layer to a favorable long-term growth story.

BMO: Tempered Enthusiasm

Monster's top- and the bottom-line beat is "optically appealing" but digging beyond the headline numbers shows three reasons to "temper investors' enthusiasm," Sharma said.

- Close to half of all U.S. sales growth can be attributed to "unproven" brands like Reign.

- U.S. sales trends are in line with IRI sales trends which point to a significant volume share loss in Monster's core brands. The company acknowledged it may take a look at pricing or promotional strategies if current volume trends remain.

- The company made use of a "seldom, if ever" used promotion by offering Reign consumers a buy-one-get-one-free offer. The analyst said this could impact margin performance moving forward, especially at a time when management needs to keep a "watchful eye" on rival Red Bull's pricing activity.

Latest Ratings for MNST

(Click on image to enlarge)