The Safety Net: Why Wall Street Is Wrong About This 11% Yield

In April, I recommended Sunoco L.P. (NYSE: SUN) to my Oxford Income Letter subscribers. The master limited partnership operates gas stations and convenience stores around the country.

Sunoco has raised its distribution (MLPs pay distributions, not dividends) in 13 of the past 15 quarters, including the past 12 quarters in a row.

You don’t often find a double-digit yield this safe.

But Sunoco’s is.

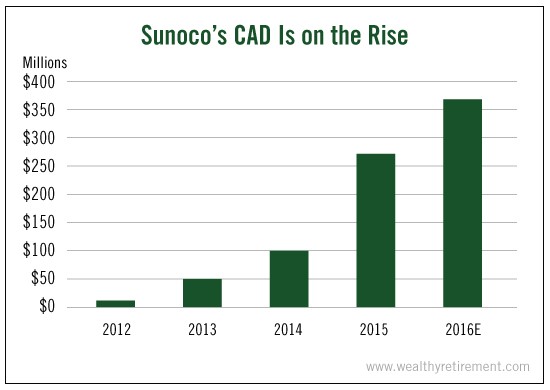

Cash Flow Boost Coming Soon

In fact, its cash available for distribution (CAD) has been steadily rising since the company’s beginning. CAD is the metric used to measure an MLP’s cash flow.

Sunoco’s CAD is expected to grow 37% this year thanks to several acquisitions that will significantly boost cash flow.

Historically, the company has paid out all of its CAD to unit holders in the form of a distribution. But with CAD rising over recent months, it’s currently paying just 88% of CAD. That’s why I expect the company to continue raising the distribution in upcoming quarters.

Keeping an Eye on Debt

Recently, however, Wall Street has become spooked by Sunoco’s debt levels.

Last month, an analyst at Jefferies said that rising debt could force Sunoco to cut its distribution.

Its loan agreements mandate a leverage ratio (measure of debt) below 6.25 in the first quarter of 2017 and 5.5 after that. Sunoco’s ratio isn’t above either level, but it’s getting close to 5.5.

If it exceeds those levels, the lenders are allowed to demand repayment. And in order to make those payments, Sunoco would likely have to cut its distribution.

Seems like a logical argument for being cautious on the distribution, doesn’t it?

Except that the Jefferies analyst forgot to mention one very important fact.

If Sunoco makes an acquisition, it’s permitted to raise its leverage ratio to 6.0 for another year. And Sunoco often makes acquisitions.

We spoke with management for more clarification. It said that if debt became a concern, it could easily make a small cash flow-positive acquisition that would buy the company some more time.

As cash flow increases, the leverage ratio decreases. So there are several things management can do – such as cutting expenses or capital expenditures – to ensure the leverage ratio doesn’t creep too high.

I’m not worried at all.

And neither is SafetyNet Pro, which gives Sunoco a high dividend safety rating.

Sunoco’s debt level is well below SafetyNet Pro’s threshold. If its debt were higher, its safety rating would be lower.

Dividend Safety Rating: B

If you have a stock whose dividend safety you’d like me to analyze, leave the ticker symbol in the comments section below.

Good investing,

Marc

Disclaimer: Nothing published by Wealthy Retirement should be considered ...

more