After 12 years of a liquidity-fueled, Fed-induced bull market, are the markets set to start another “secular” bear market? In an interview with the Financial Times, Boaz Weinstein, founder of Saba Capital Management, suggested such.

“There isn’t a rainbow at the end of all this. There’s no reason that this difficult economic period will only last two to three quarters and no reason to think we’ll have a soft landing or a shallow recession.”

Before you dismiss his opinion as hyperbole, Saba Capital was one of the world’s top-performing hedge funds in 2020 and is up by almost a third in 2022.

Before we go further with our analysis, we must distinguish between a cyclical and secular market cycle.

“A secular market trend is a long-term trend which lasts 5 to 25 years and consists of a series of primary trends. A secular bear market consists of smaller bull markets and larger bear markets; a secular bull market consists of larger bull markets and smaller bear markets.”

The prevailing trend in a “secular bull” market is “bullish” or upward-moving. In a “secular bear,” the market tends to trend sideways with severe drawdowns and sharp rallies.

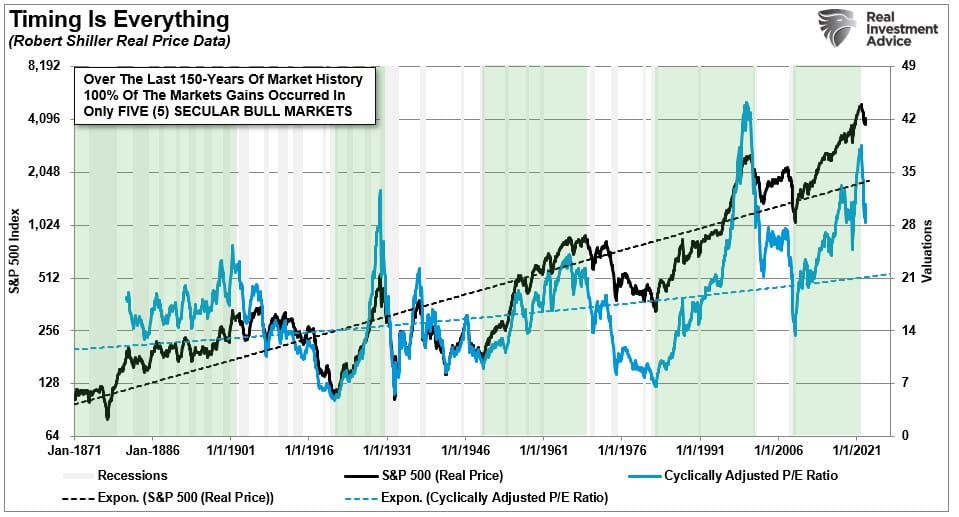

The chart below shows the market from 1871 to the present, with secular bull market cycles highlighted.

Notably, as an investor, only 5-periods are secular bull markets (where prices are increasing) over the last 150 years. Those five periods account for 100% of all the index gains. In other words, the outcome was disappointing if you invested on a buy-and-hold basis during any other period.

Valuations & Earnings

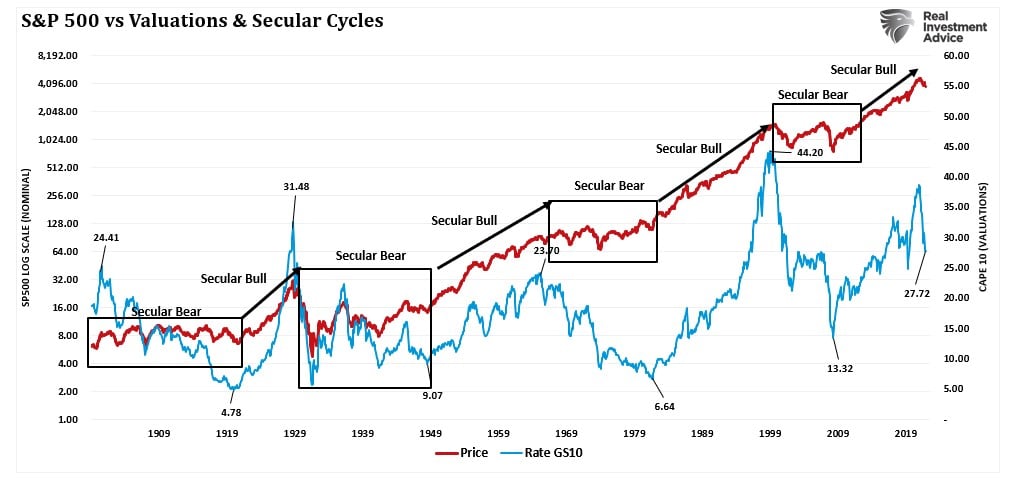

Three items drive secular bull markets: 1) valuation expansion, 2) earnings growth, and 3) falling interest rates. The most prominent driver of secular returns are periods of valuation expansion and contractions.

The chart above shows the history of secular market periods going back to 1871 using data from Dr. Robert Shiller. You will notice that secular bull markets begin with CAPE valuations around 10x earnings or even less. Secular bear markets tend to start with valuations of 23-25x earnings or greater. (Over the long-term, valuations do matter.) Most notably, secular BEAR market periods are defined by near-zero returns during the valuation contraction process.

It is imperative to remember valuations are very predictive of long-term returns from the investment process. However, they are horrible timing indicators. Because valuations, and fundamentals in general, take a long-time to play out in the markets, it is not surprising investors dismiss them during a secular bull market.

As noted, what drives long-term secular “bear” markets is “valuation contraction.” Such is driven by investor re-evaluation of earning power by companies due to changes in interest rates, inflation, and, most importantly, prospects for economic growth. Unfortunately, forward prospects for more robust economic growth remain challenging due to high debt levels, which is a deflationary headwind.

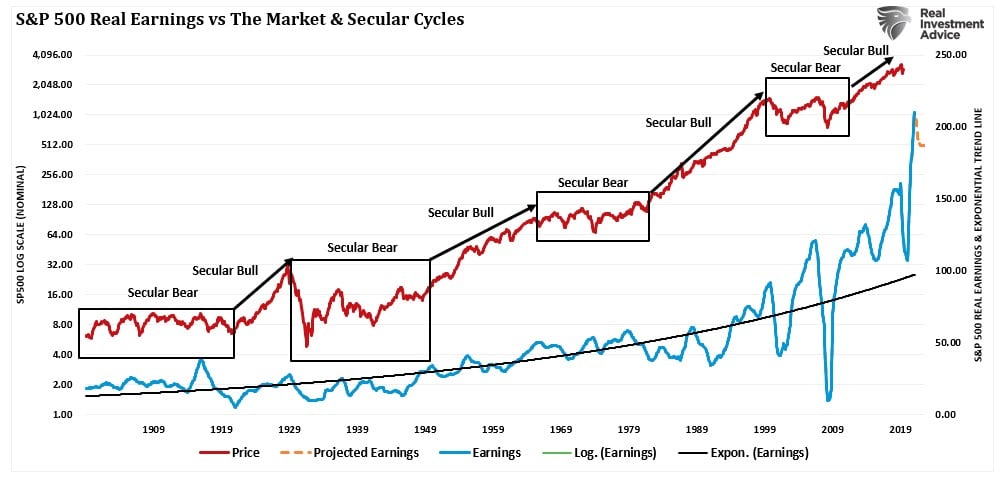

The problem of overvaluation in a slow-growth economic environment is problematic. The massive surge in earnings during the pandemic-driven shutdown is unsustainable as the economy normalizes. Massive stimulus programs, combined with enormous unemployment, led to surging profits that are not replicable in the future. As shown, earnings are one of the most mean-reverting data series in existence, and ultimately if earnings don’t revert, capitalism is no longer functioning correctly.

The most obvious indication that a secular bear market may be upon us is the deviation of earnings from their underlying growth trend. Earnings can not, over the long term, outgrow the economy. Such is because it is economic activity that creates corporate revenues. The eventual reversion in economic growth and corporate earnings suggests that asset prices are vulnerable to a much more significant repricing to reflect future economic realities.

Don’t Be Afraid. Just Be Aware Of The Bear

As stated above, the stock market reflects the underlying economic activity over the long term. Personal consumption makes up roughly 70% of that activity. The consumer is more heavily leveraged than ever, making it doubtful they can become a significantly larger chunk of the economy. With savings low, income growth lagging inflation, and debt back at record levels, the fundamental capacity to re-leverage to similar extremes is no longer available.

Let’s also not forget the singular most important fact.

Following the two previous bear markets, the breakout of the markets in 2013 was NOT one based on organic economic fundamentals. Instead, it was from massive monetary interventions by Central Banks globally. All previous secular bull markets were a function of extreme under-valuations, washed-out financial markets, and falling interest rates.

Such is not the case currently.

Hopefully, I am wrong, and the secular bull market that began in 2013 has years of life left in it. However, given high debt levels, a rise in socialistic policies, and the shift from capitalism to corporatism, there is a risk of a reversion.

Such doesn’t mean you can’t make money in a secular bear market. You can, as there will be fantastic rallies. However, those rallies will likely get repeatedly met with disappointing declines. Such means that market returns will probably be exceptionally low on a “buy and hold” basis. However, investors with a bit of skill, a little luck, and a lot of work can likely continue to build wealth as the market reprices to a slow economic growth environment.

One thing is sure. Until Central Banks revert to all-out monetary accommodation, investors will face a challenging investment environment as valuation contraction continues to drive future returns.

More By This Author:

More Bearish Market Action Before The Bull Can Run

Hard Landing Coming? Investors Don’t Think So

Midterm Elections Are Bullish Even In A Bear Market

Comments

Log in or sign up to join the conversation.