The Amtrust "Hit-Piece:" Amateur Hour Short-Selling From The Once Respectable Geoinvesting

Geoinvesting is a bunch of short-sellers who I grew to respect during the great era of picking off Chinese reverse merger scams. They got several right and the ones that they got wrong (notably on Zhongpin) they were I believe right on most of the analysis.

Yesterday they came out with a "hit-piece" on Seeking Alpha on Amtrust Financial Services (AFSI). This is a complicated, high growth, multi-jurisdictional insurance company. For most people a black box. For me it is home turf. Most my career I was a bank and insurance analyst (and the first 200 or so posts on this blog are about financial institutions). [Check my title here if you want career details...]

Amtrust is clearly a worthy candidate for examination by a short-seller. Several of the executives have colourful backgrounds and it is in a bunch of difficult, even problematic businesses. The first problem is identified by Geoinvesting. The second not so much.

One business that they are in – and one responsible for a large proportion of the growth – is California Workers Compensation, sometimes written (and any insurance junky will tell you this is problematic) through Managing General Agents.

Other businesses are also difficult, eg life settlements or buying of in-force life-insurance policies, in this case originally written by marginally problematic insurance companies.

They are also in the slimey business of offering warranty extensions on electronic goods sold through second tier retailers. [Anyone who buys the warranty extension is an idiot, and many of these are missold leaving all sorts of liabilities behind.]

But the real warts in this business (and there are many) are simply not identified by Geoinvesting – and instead they make howling error after howling error in their report.

Howler one: accusations of reinsurance accounting fraud by someone who does not understand what is meant by "ceded losses"

The allegation in the Geoinvesting report is that Amtrust has – and I quote:

From 2009 to 2012 we believe that AFSI has not disclosed a total of $276.9 million in losses ceded to Luxembourg subsidiaries.

What Geoinvesting mean by this is that they believe that Amtrust has simply failed to recognize in their consolidated P&L $276.9 million in losses.

This is a total misunderstanding of what is meant by "ceding losses". To explain I need to explain reinsurance a little (though in this case with some help from the very well written Wikipedia article):

When an insurance policy is written the insurance company "writer" will recognize as an asset the premium received. They will also recognize a "loss reserve" an amount being the amount they will expect to pay out on the policy over time.

This "loss reserve" is not a loss. Its simply a reserve for future payments. Whether the policy makes a profit or loss will be determined as the decades roll on. [If it is a workers compensation policy for instance an insurer may be paying an injured worker's medical bills thirty years hence...]

In a typical (and in this case proportional) reinsurance arrangement, a reinsurer takes a stated percentage share of each policy that an insurer produces "writes". This means that the reinsurer will receive that stated percentage of the premiums and will pay the same percentage of claims. In an accounting sense this is called "ceding the loss" and "ceding the premium" to the reinsurer. The reinsurer also recognizes no loss in the P&L. The gain or loss of the policy is recognized over decades.

In addition, the reinsurer will allow a "ceding commission" to the insurer to cover the costs incurred by the insurer (marketing, underwriting, claims etc.).

Geoinvesting has simply added up the "losses ceded" to the (internal) reinsurers and wondered why the "losses" did not wind up in the P&L.

This is profoundly amateurish.

It must be galling for the management of Amtrust to be accused of reinsurance fraud by someone who does not appear to be able to comprehend the basic Wikipedia article on reinsurance.

Life settlements

Life settlements are a business with a reputation for scumminess. It is the business of buying life insurance policies for more than their surrender value but less than their face value.

There are legitimate reasons for life settlements. Insurance companies are parsimonious slime-balls on the surrender value of a life insurance policy. They consider surrender a significant source of profit.

And some people might want to cash their life insurance policy – for example someone with terminal cancer and big medical bills may wish to cash their life policy so that they have money to pay their bills before they die. And the insurance company won't offer anything like fair value for a policy which is about to be claimed on.

But the reputation for scumminess is also deserved. In the early days of the HIV epidemic there was no test for HIV and men who visited "bathhouses" in San Francisco had low life expectancies. There were viatical companies who encouraged these men to buy policies which they immediately purchased from them at a premium. Of course they encouraged the men to lie about their sexuality. This was fraud against the insurance companies pure and simple.

It turns out that life settlements, particularly of the scummy variety, was not as good a business as it seemed. Insurance companies sometimes successfully persuaded the Feds to knock down your door and "examine" your business. But just as bad, policies that once traded at a premium (eg men with HIV) turned out to be worth less than was expected. HIV patients once had a two year life expectancy. The new drugs have extended that sometimes to more than twenty years. The life settlement company expected to collect a big fat policy. Instead they wound up paying twenty years of unexpected premiums.

Life settlement businesses (sometimes called viatical businesses) are justifiably controversial. Many have not turned out that well for investors.

Anyway Amtrust is in the life settlement business.

Here is what Geoinvesting say about it.

AFSI appears to be boosting earnings and tangible book value by marking up its portfolio of life settlement contracts ("LSCs"). LSC, net of non-controlling interest now represent approximately 19% of AFSI's tangible book value. In valuing an LSC portfolio, the discount rate and life expectancy ("LE") are the two most critical inputs. AFSI uses a 7.5% discount rate to value its LSCs while peers use a rate approximately 20%. Applying industry standard discount rates would result in a mark down of $90-135 million, or roughly 13-19% of AFSI's tangible equity. Further, it appears that AFSI relies on internal estimates, only considering third party estimates for the LE input (See 10-Q for the period ended September 30, 2013, page 17). In contrast, best practice is to use third party estimates to determine LE estimates and weight them towards the more conservative estimate. The use of internal LE estimates has been a staple of past frauds in the LSC industry (notably,Life Partners and Mutual Benefits).

AFSI has been revising down its LE assumptions, generating gains on its LSC portfolio. Publicly traded peers are revising their LE assumptions higher (especially for the premium-financed LSC paper that AFSI holds). Simply put, peers are assuming people are living longer while AFSI assumes people are going to die sooner. We are unaware of any reason why AFSI is taking a non-consensus view on lifespans of Americans. It is possible that AFSI's policyholders en masse have decided to take up smoking, skydiving, or ride motorcycles without their helmets, but given a diverse base of people, this seems unlikely despite what AFSI management is asking the market to believe if you accept its LSC valuations.

More than half of AFSI's LSC portfolio consists of contracts where Phoenix Life Insurance is the issuing carrier/counterparty . Faced with possible bankruptcy, PNX has been attempting to induce holders of its LSC paper to lapse on their policies by hiking premiums & denying death benefits. Given the possibility that PNX death benefits will not be paid, when PNX paper does trade, it trades for pennies on the dollar.

Now lets examine AFSI's rhetoric. They say dismiss changing life expectancy expectations as follows: it is possible that AFSI's policyholders en masse have decided to take up smoking, skydiving, or ride motorcycles without their helmets, but given a diverse base of people, this seems unlikely despite what AFSI management is asking the market to believe if you accept its LSC valuations."

Okay – well here are the policies and their assumptions as per the linked 10-Q:

The fair value of life settlement contracts as well as life settlement profit commission liability is based on information available to the Company at the end of the reporting period. The Company considers the following factors in its fair value estimates: cost at date of purchase, recent purchases and sales of similar investments (if available and applicable), financial standing of the issuer, changes in economic conditions affecting the issuer, maintenance cost, premiums, benefits, standard actuarially developed mortality tables and life expectancy reports prepared by nationally recognized and independent third party medical underwriters.

This seems pretty generous. Usually with a life insurance policy you would estimate values off some actuarial table and hope laws of large numbers mean you get it approximately right.

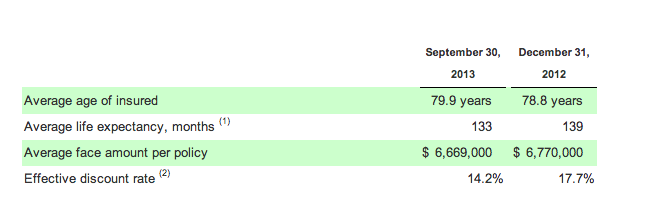

This company is different. Here are the details on the policies:

Yes – the average age of the insured is 79.9 years. They are old fogies. And their life expectancy is estimated as an average of 133 months or another 11.1 years. The company is assuming their life policy holders will live to an average of 91 years old.

Now this does not strike me an inherently implausibly low life expectancy – a life expectancy that geoinvesting could plausibly send up by wondering if these people (old fogies) have suddenly decided to take up skydiving. On these numbers it does not look like Amtrust is manipulating down the life expectancy to make their life-settlements business appear overly profitable.

In fact it looks like the opposite. At 31 December 2012 the average age of insured was 78.8 years and they were expected to live another 139 months which would place them an average age at death of 90.4 years. Now they are expected to have an average age at death of 91.0 years. The company has lengthened the average life expectancy which lowers the expected value of these policies. Geoinvesting argue they have manipulated life expectancy data to increase stated profit. The reverse is true – the changes in their life expectancy assumptions have lowered their expected profit.

There is a word for what Geoinvesting asserted: wrong.

Policies with a $6.669 million average face value against 79.9 year olds are clearly worth a lot of money. Perhaps it is unreasonable to chose your own life expectancy on each individual policy based on your assessment of their medical condition. But in this situation case-by-case assessment does not seem unreasonable. The 10-Q reveals precisely 272 policies in the book. That is all the business is… and it is likely that Amtrust has good data on all of its insured.

Geoinvesting is scathing about the 7 percent rate used to discount these policies (to determine their value) and compare it to high rates at other companies. I disagree. Other companies do things like buy policies from young people who have cancer. These people have a high risk of dying – but they also have (from the perspective of someone who is betting on their death) a high risk of surviving. A high discount rate is appropriate for these people. By contrast Amtrust is betting on 80 year olds dying pretty soon. I figure that is a safe bet and a low discount rate seems appropriate. 7 percent doesn't seem unreasonable.

Geoinvesting has a point though about a substantial proportion of the policies being against a single insurer, Phoenix. Phoenix after demutualization grew like crazy by selling underpriced insurance policies (not a good idea). These underpriced policies prompted viatical companies to encourage people to take insurance that they would in turn purchase. Phoenix continued to grow. It wound up with a large book of business and a buoyant stock price. Unsurprisingly it invested the loot badly and in collapsed in the financial crisis. The stock price is a shadow of its former self and it has not filed SEC accounts for over a year. [The old accounts have been withdrawn and will be restated.]*

Phoenix however looks like it will survive. The regulator is even allowing the insurance company to pay almsot 30 million in dividends to the parent company (the listed stock). The regulator would not do this if they had discomfort about valid policyholders being paid.

Moreover Amtrust owns policies on people with an average age of almost 80. Surely some of them have died. So far they have not had any trouble collecting – the idea that these policies should be held by Amtrust at pennies on the dollar is ludicrous. But that is what Geoinvesting is suggesting.

Dangerous business

I don't want to pretend that Amtrust is a good business or that it is a bottom-drawer investment that you can safely put away for thirty years. It is not.

For instance they have been growing very fast in the dangerous game of California Workers' Compensation Insurance.

California Workers Comp has left a graveyard of dead insurance companies including some from Australia. Its an ugly place to do difficult business.

The first reason is a technical one: California Workers Comp policies are – by law – unlimited. When you buy auto or liability insurance there is almost always a maximum claim. The insurance company can bound its risk – and if – perchance you crash your car into a Rolls Royce showroom (causing $20 million in damage) your insurance company will cover you for damages up until the cap. But in California you might wind up with $40 million damages on a single policy. [Imagine the medical and care bills for a quadriplegic who lives another 45 years...]

The second reason why California is difficult is persistent "social inflation". The things an (unlimited) insurer is meant to cover have increased over the decades with Californian social mores. Think about "diseases" like fibromyalgia or carpels tunnel syndrome. Combined with increasing life expectancy for some injured (eg paraplegics, carpels tunnel "victims") this has been expensive.

The third reason that California is difficult is that the (state) insurance regulator is very competent at grabbing and securing your assets for the benefit of policyholders and not for the benefit of shareholders.

These things however take decades to play out. A typical California workers comp insurer seems to be extremely profitable on the current book of business but finds that old business produces old liabilities (eg carpels tunnel from white-collar workers who were originally thought to be and priced as low risk). The bad bits of the business grow over time.

The way Amtrust has been growing is by buying the renewal rights for insurance companies that have gone bankrupt. For instance they purchased the renewal rights from Majestic.

These will produce a business that looks really great now. And it will compound very nicely. In year one you have only the earnings from year one. In year two you have those earnings plus the earnings on the assets backing claims from year one. So on for year three. Profits grow at a super-fast compounding rate.

In the end it is difficult though because in the end every old insurance company winds up with old liabilities and in the case of California workers comp there is a reasonable chance the old liabilities kill you.

And in this case it might be particularly difficult. After all the customer list was purchased from a bankrupt company. It is unlikely to be a low risk or easy to price book of customers.

Why this is the perfect candidate for a short-squeeze

I have seldom seen a better candidate for a short squeeze. There is a large short position in the stock.

Some short-sellers however do not understand what they are short. They probably found the colourful people and built a story around it. The published short-thesis is incompetent.

Moreover the company is growing really fast in several businesses like California Workers Compensation. These may be (and probably are) very bad businesses that will eventually cause the company huge problems – but we may not know about these problems for a decade. It may actually wind up quite well. California may even have "social deflation". It seems unlikely but a decade is a long time and surprising things might happen.

There were several subprime mortgage companies run by colourful people in 2001. They wrote bad business and it eventually killed them. But if you were short the stock from 2001 you were pulverised. I would be receptive to a story that said you should short this company but you would have to argue that it was (say) Conseco 2001 not Conseco 1990. That is not an argument that Geoinvesting even attempt.

Meanwhile I went and took a small long. Its not a business I am comfortable owning long term but when I see people who are loudly incompetent in markets I want to get on the other side.

John

*When Phoenix collapsed it spun out a good business: Virtus Asset Management. This was one of the more successful investments in the history of Bronte. Check out the chart. We got moderately familiar with Phoenix and its parts.