Stagnant Earnings Create A Risky Environment For Dividend Investors

As a dividend growth investor, my goal to purchase shares in a company at an attractive valuation, and then receive a rising stream of dividend payments for decades.

The companies that tend to shower shareholders with more dividends every year tend to be the ones who manage to grow earnings per share over time and have manageable payout ratios. These companies manage to distribute excess cash to shareholders in the form of dividends. As earnings are rising, this translates into higher annual dividends for these shareholders. Any remaining earnings are retained to maintain and grow the business, which results in more growth down the road.

At some point, corporations start facing challenges due to changes in the competitive environment. As a result, companies are unable to grow revenues and earnings per share. This in itself is not a problem, because shareholders could still, in theory, generate high returns, even if revenues and earnings are flat. For example, if a company stops growing and as a result sells at 10 times earnings, it can generate great returns to shareholders if it distributed most of its earnings in the form of dividends or share buybacks. If the company manages to cut costs a little bit, it can generate good long-term returns to shareholders. This is management’s job – to work for the shareholders.

Unfortunately, at some point, management teams become unhappy with the status quo. It is not exciting to be sitting still, generating a lot of excess cashflows, but not growing the business. All of this creates the urge for management teams to do something. Rather than focus on shareholder returns, they focus on growing the enterprise at all costs, in order to perpetuate the entity and get higher status in the corporate world ( and bigger paychecks too). This is an example of the tug of war between top management and shareholders. In theory, top management works for shareholders who have capital at risk. In reality, top management is only looking after themselves. Most CEO’s are not very good at what they do. It is usually the business model or the business environment that creates shareholder wealth – management usually just take the credit for being in the right place at the right time.

In some cases, they end up buying growth at inflated valuations, so that revenues grow and net income grows. That doesn’t fool investors however. In the process, these management teams discard the prudent strategy of dividend growth and share buybacks used to share profits with investors. By taking on more debt, or using stock at cheap prices to fund acquisitions at inflated values, these companies waste shareholder resources and endanger the financial viability of the enterprise.

A few companies I had in mind when writing this article include General Mills and IBM. I am tempted to include Altria as well, despite the fact that the company has managed to grow earnings and revenues.

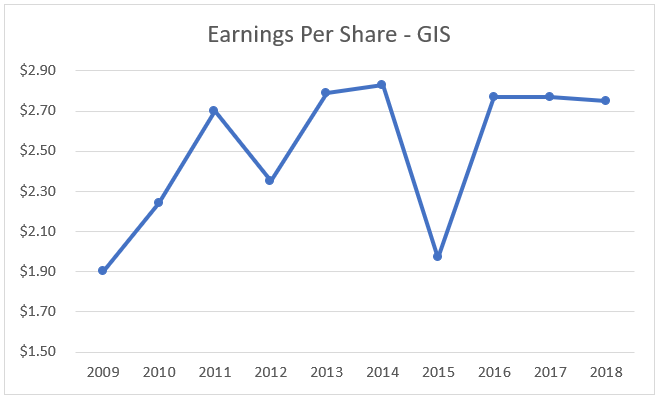

General Mills (GIS )

For several years in a row, General Mills had been unable to grow earnings per share. The company earned $2.70/share in 2011, and it was unable to grow beyond that amount. That is unfortunate given the fact that over 12% of shares outstanding were repurchased during that time period. The 2018 earnings per share have been adjusted for the one-time 89 cent/share impact of the new tax law signed at the end of 2017.

A few months ago, General Mills acquired Blue Buffalo, which produces pet food. Usually, acquisitions are a great source of future earnings growth, as you get synergies on top of existing lines of business. In the case of General Mills, however, the company ended up overpaying massively, using cheap stock it sold at $44/share or almost 14 times forward earnings. This is unfortunate because General Mills had acquired shares over the past five years at prices that were higher than $44/share.

Blue Buffalo was purchased for roughly $8 billion and had earnings of $193 million in 2017. The stock was acquired for $40/share, while it earned 99 cents/share in 2017. The company had sales of $1.27 billion in 2017.

While General Mills did not obtain a lot of earnings power and revenues from Blue Buffalo, it mostly paid up for the future expected growth.

Perhaps they saw that some of their competitors own pet foods ( Nestle, Colgate-Palmolive, J.M. Smucker), so they decided to own a piece of the pie.

Nevertheless, I find it foolish that they spent billions of dollars buying back stock when it was high, only to sell billions in stock at the low price of $44/share. As a result, they are no longer buying back stock when the price is even lower today. And best of all, General Mills froze the dividend. When they sold those extra shares, now they have to pay even more in total dividend income, leaving less for growing the dividend income for the existing shareholders like you and me. Given the high yield today, some investors seem to believe that there is a higher chance of a dividend cut than an year ago.

I believe that management is trying hard to make themselves look better, after several years of stagnant revenues and earnings. This really created the pressure to do something. In reality, shareholders would have been better if the funds used to acquire Blue Buffalo were distributed as special dividends or even through share buybacks.

I believe that the underlying business that General Mills is strong enough to withstand some mismanagement. So while I will hold on to my shares for as long as the dividend is maintained, I doubt I will add to my position.

The stock looks cheap at 13.70 times forward earnings and yields 4.70% today. The stagnant earnings and stagnant dividend is what is keeping me away from adding to my position there. I will likely allocate dividends elsewhere as well.

International Business Machines (IBM)

A few months ago IBM announced that it would acquire cloud company Red Hat for over $34 billion. Red Hat earned $259 million in 2018 on annual revenues of $2.92 billion. I believe that IBM is overpaying for this acquisition. I believe that IBM is desperate to get out of the trend of declining revenues at any price, after experiencing several years’ worth of decreasing sales.

IBM’s 2017 revenues of $79 billion were smaller than their 2008 revenues of $103 billion. Earnings per share grew from $8.89 in 2008 to $11.98 in 2017 ( adjusted for the one-time impact of the new tax law enacted at the end of 2017).

I believe that IBM should have simply stuck to its role of growing the dividend and making share buybacks. At least the purchase is made with cash and debt. As a result of the acquisition, the share buybacks have been halted, which is ironic given the fact that the share price is at its lowest this decade and is selling at a very low valuation today. IBM shares are selling at roughly 13.90 times earnings and yield 5.20%.

If I were in charge of IBM, this would be the time to step on the gas to do buybacks when valuations are low. Or just distribute special dividends to shareholders.

It is likely that IBM can turn its operations around, and the stock today is a great bargain. However, it is also possible that it continues to go through a painful transition. IBM has been through a transition before, in the early 1990s. The company did manage to pull through but had to cut its generous dividend ( ironically the stock was yielding around 5% at that time as well). In my case, I will continue holding on to any shares I own, but allocate dividends elsewhere. Due to the stagnant earnings per share, I do not see the stock as a long-term buy at the moment.

Altria Group (MO)

Last month, Altria purchased a large stake in an upcoming competitor JUUL. I dislike the fact that Altria is overpaying so much, and it is also providing a lot of concessions which are going to disrupt its existing cigarette business. I wrote a more detailed article on the topic here. The difference, of course, is the fact that Altria has been able to grow earnings and even revenues over the past decade.

Conclusion

I believe that stagnant earnings and revenues create pressure for company executives to do something. This pressure leads to expensive acquisitions to grow the company's revenues and earnings at any cost. When companies are desperate to grow the bottom line at any cost through acquisitions, they risk overpaying for the shiny company with growth expectations behind it. When you overpay dearly for a growth company, you can undo the effects of a subsequent decade of favorable business developments. Ultimately, the price is being paid by shareholders, as the focus shifts from sending excess cashflows in the form of dividends, to purchasing growth at high valuations.

In the case of General Mills (GIS), IBM (IBM) and Altria (MO), these stocks are cheap today. If they can turn the operations around and grow those earnings, it is possible that an investment today will be a smart one. However, if there is integration risk, and rosy growth expectations do not turn out as expected, managements would have ended up wasting shareholder resources. Any extra debt can shift the focus from being a dividend growth company to becoming a growth company. This change in mindset can increase the risk of a dividend cut down the road, particularly if reality does not work out as the projections.

In my case, I will keep holding on to my positions in all three companies. However, I will allocate dividends elsewhere. If the dividends are cut, I will likely sell my positions there.

Disclaimer: I am not a licensed investment adviser, and I am not providing you with individual investment advice on this site. Please consult with an investment professional before you invest ...

more