Closed end funds (CEFs) are an obscure sector of the market with a small but fiercely passionate following. Because they have a fixed share count, they can trade at a premium or discount to the value of their holdings, which are usually public equities or debt. This creates appealing opportunities to buy at a discount to intrinsic value. Closed End Fund Advisors provides a lot of useful information on the sector.

Liquidity is always a problem, so the investors tend to be retail with a small handful of institutions. It can sometimes take several days to get into or out of positions. We occasionally run across financial advisors who invest in CEFs for their clients.

In theory, CEFs should generally trade at a discount to Net Asset Value (NAV), because of their relative illiquidity compared to the basket of underlying shares. MLP CEFS have an especially interesting history. We often note the terrible tax structure of the Alerian MLP ETF, AMLP (see MLP Funds Made for Uncle Sam). But MLP CEFS pre-date AMLP and provided some justification for its launch.

(Click on image to enlarge)

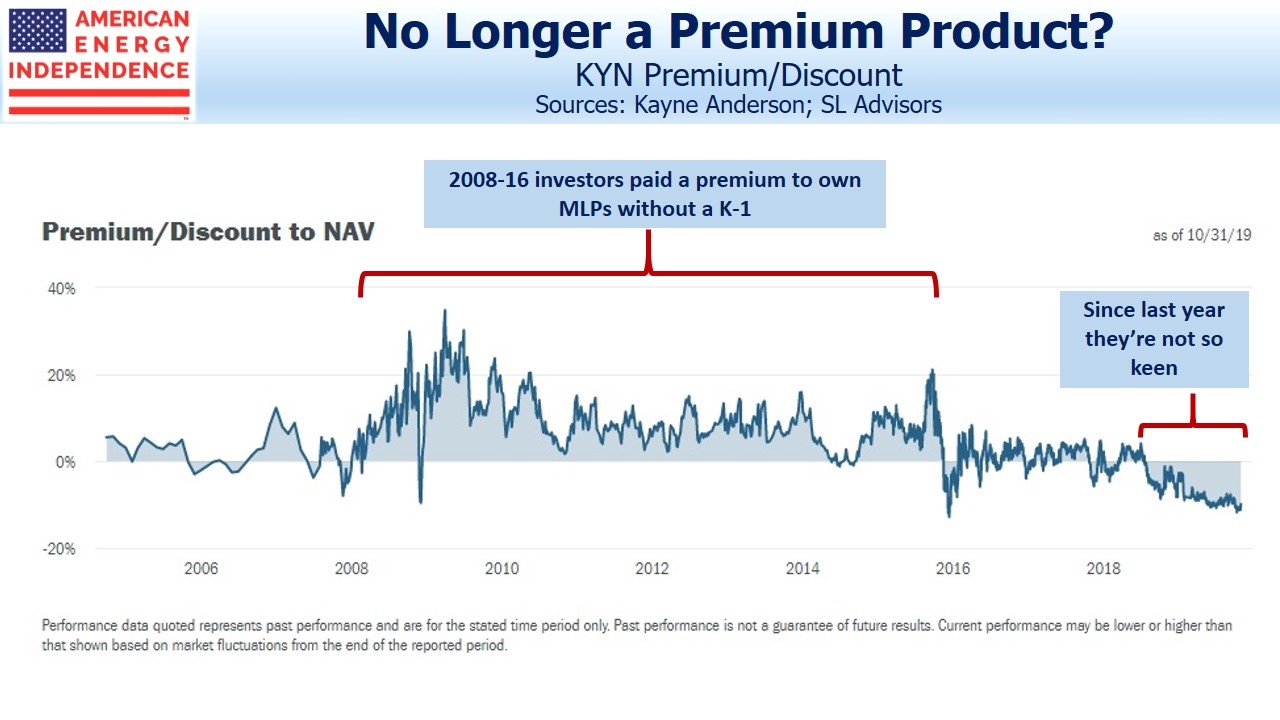

This is because for many years MLP CEFs consistently traded at a premium to NAV. The Kayne Anderson MLP/Midstream Investment Company (KYN) illustrates this point. For most of its history, KYN shares have traded at least 5% higher than NAV and at times over 30%. MLP CEFs possess the same tax inefficiencies as AMLP, in that they are liable for corporate taxes because they are more than 25% invested in MLPs.

The benefit of the tax drag is that KYN investors get exposure to MLPs without the tax hassle of K-1s for tax reporting. A decade ago, investors clearly placed a high value on this simplified tax reporting, as evidenced by the substantial premium to NAV at which KYN traded. AMLP’s 2010 launch took place against this backdrop of strong demand for the tax-burdened, 1099 structure.

Where KYN and other MLP CEFs differ from AMLP is in their use of leverage. This is common in CEFs and supports higher yields in exchange for increased NAV volatility. In addition, the interest expense lowers taxable income, which can lower the inherent inefficiency of an MLP CEF with its corporate tax obligation.

For the past year, KYN has traded at a discount to NAV averaging almost 10%. It’s another symptom of declining retail interest in the sector. The sharp 2014-16 drop with heightened volatility caused some damage.

It’s worth revisiting the use of leverage by MLP CEFs. To continue with KYN, in reviewing their past financials, they seek to stay close to “400% debt coverage”, meaning that their desired portfolio consists of $400 in investments funded with $100MM in debt and $300MM in equity. So $1 invested in KYN controls $1.33 in MLPs. The 400% debt coverage rises and falls with the market. Rebalancing back to their target requires selling after a market drop, and buying following a rally (i.e. buy high, sell low). KYN tends to move a little more than the market as a result.

The question is, whether such leverage continues to make sense. MLP balance sheets have come under a great deal of scrutiny in recent years. The industry has moved towards self-funding growth projects with less reliance on external financing; higher distribution coverage; less leverage. Investment grade companies now target around 4X Debt:EBITDA.

A portfolio of MLPs is pretty concentrated. An investor in KYN or other MLP CEF, by accepting leverage at the CEF level, is implicitly rejecting the industry’s 4X Debt:EBITDA target as needlessly conservative. Is this a smart decision? It might make sense to add leverage to a diversified portfolio, because the low correlations across pairs of individual names will keep the portfolio’s volatility below that of its average holding. But if you’re invested in a single sector, the average volatility of the holdings will come close to your portfolio’s volatility. Adding leverage to that portfolio increasingly looks like adding more debt to each individual holding. The practical result is that the investor is adding more risk than the company and credit rating agencies deem appropriate.

We don’t use leverage in our business. The sector has been volatile enough in recent years, and the periodic rebalancings that are required tend to force you to buy high/sell low.

In KYN’s most recent quarterly financials (August 31), they noted 401% debt coverage versus their target of 400%. Since August, the Alerian MLP index (AMZX) has dropped 10%, implying KYN’s coverage ratio has sunk to 360%. Restoring their 400% target coverage will have required selling over $110MM in securities, adding to the market’s recent selling pressure. Last year’s 4Q saw a 17% drop in AMZX which was almost certainly exacerbated by MLP CEFs delivering. The rebound earlier in the year would have seen MLP CEFs similarly increasing leverage back up.

MLP CEFs are constantly chasing the market to restore their desired leverage. Higher volatility increases the cost of such frequent portfolio rebalancings. We think it’s time their investors reassessed whether accessing the sector with leverage makes sense.

Comments

Log in or sign up to join the conversation.