Rogers Communications- The Telecom Riding The Market Like There Is No Tomorrow

For the second part of my “Canadian Telecoms on the radar”, I’m taking a look at Rogers Communications (RCI). The company rid the market this year with +27% as at July 22nd 2017. Is it too much? Is it too late to pick this gem? Let’s dig deeper to find out!

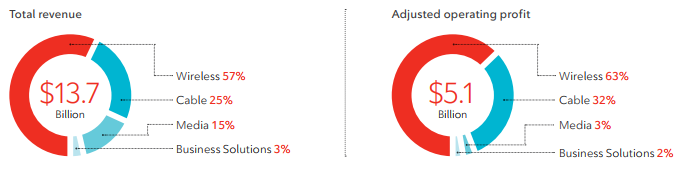

Rogers Communications has adapted since its creation to offer the services and technology its clients were looking for. It started with radio broadcasting, added television and internet services, and now has a predominant wireless business segment:

Source: RCI 2016 annual report

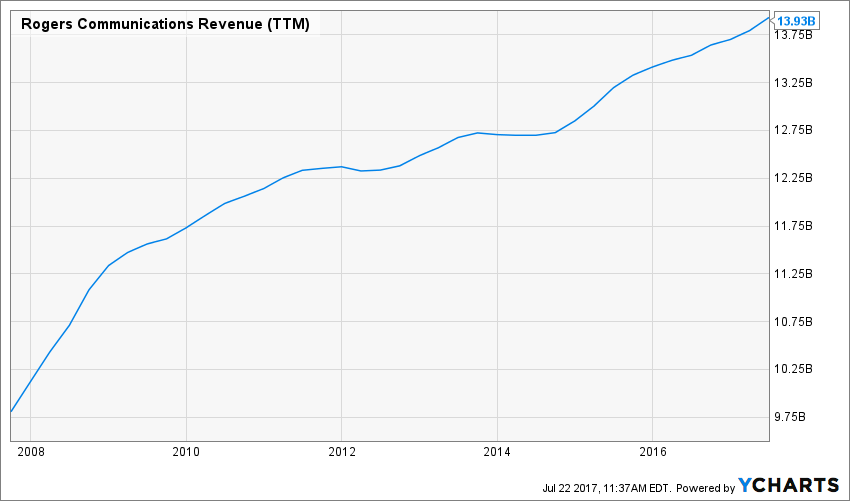

Revenue

Revenue Graph from Ycharts

Rogers has shown a very strong revenue progression since 2008. The company’s latest move was pricey, but I appreciate the effort to always bring something new to the table for shareholders. Back in 2013, RCI agreed to pay $5.2 billion to own the broadcasting right of all the NHL games. It now appears as very good timing as the Oilers & Maple Leafs are now back in the race for the cup with young and talented teams. Sports now represent more than 50% of RCI’s media segment revenue. Rogers also tends to pay high prices for new spectrum licences, a must in the wireless industry.

How RCI fares vs My 7 Principles of Investing

We all have our methods for analyzing a company. Over the years of trading, I’ve been through several stock research methodologies from various sources. This is how I came up with my 7 investing principles of dividend investing. Let’s take a closer look at them.

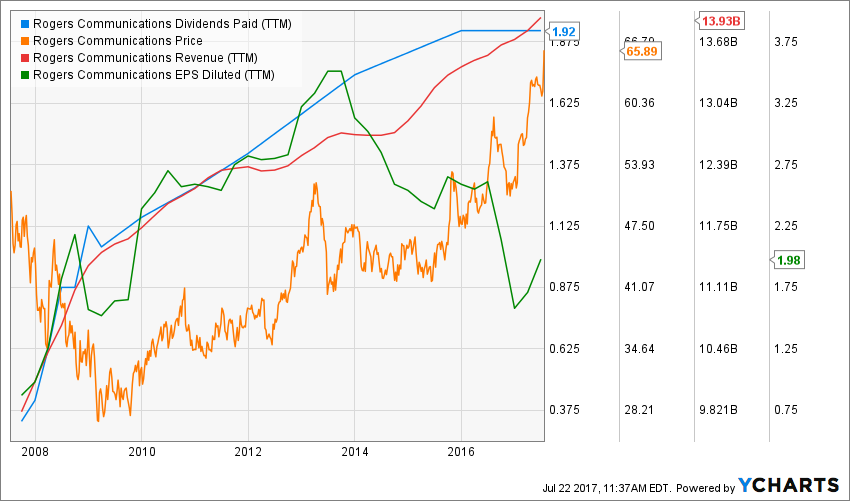

Source: Ycharts

Principle #1: High Dividend Yield Doesn’t Equal High Returns

My first investment principle goes against many income seeking investors’ rules: I try to avoid most companies with a dividend yield over 5%. Very few investments like this will be made in my case (you can read my case against high dividend yield here). The reason is simple; when a company pays a high dividend, it’s because the market thinks it’s a risky investment… or that the company has nothing else but a constant cash flow to offer its investors. However, high yield hardly comes with dividend growth and this is what I am seeking most.

Source: data from Ycharts.

RCI has always offered an interesting yield to income-seeking investors. However, the recent stock price surge pushed the yield under the 3% level for the first time in almost a decade. Still, RCI yield remains decent considering the overall market.

RCI meets my 1st investing principles.

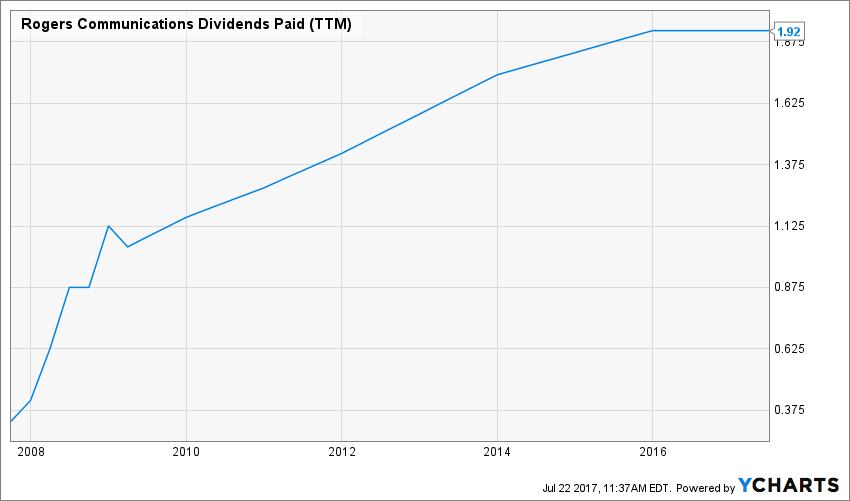

Principle#2: Focus on Dividend Growth

Speaking of which, my second investing principle relates to dividend growth as being the most important metric of all. It proves management’s trust in the company’s future and is also a good sign of a sound business model. Over time, a dividend payment cannot be increased if the company is unable to increase its earnings. Steady earnings can’t be derived from anything else but increasing revenue. Who doesn’t want to own a company that shows rising revenues and earnings?

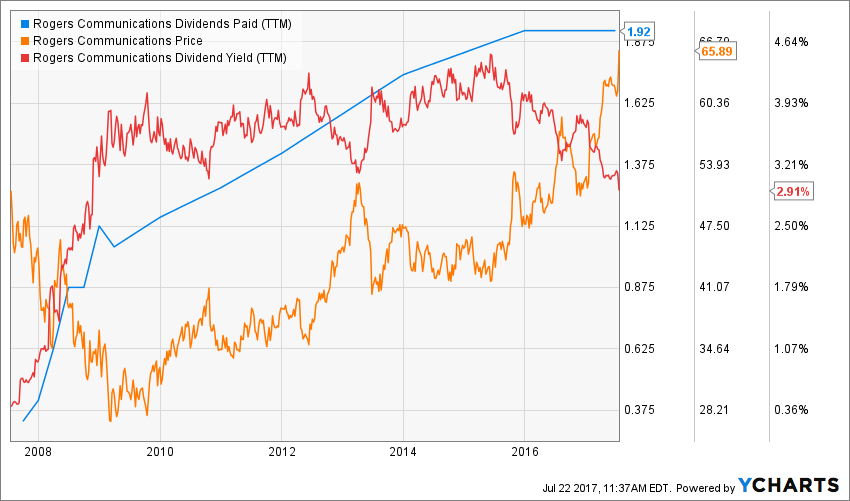

Source: Ycharts

Rogers Communications is part of the Canadian dividend aristocrats list. I expect another dividend raise this year as management took a pause in dividend increase last year. It will have to come with a new raise this year to keep their aristocrat title.

RCI meets my 2nd investing principle for now.

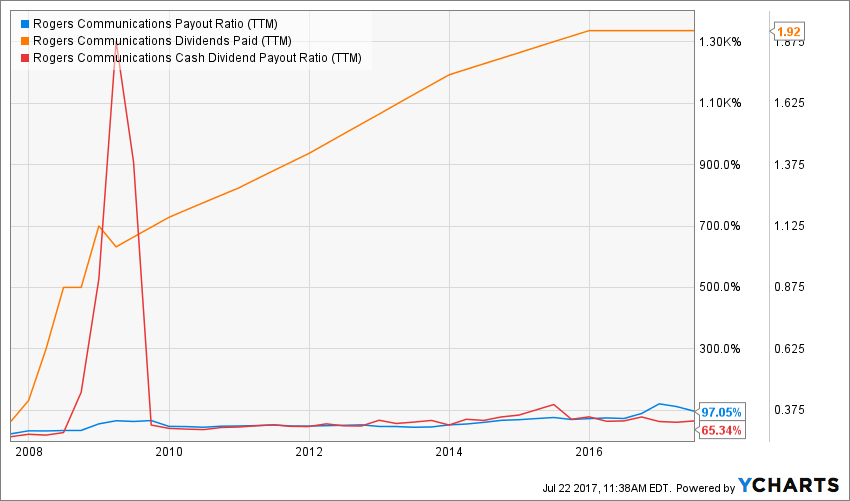

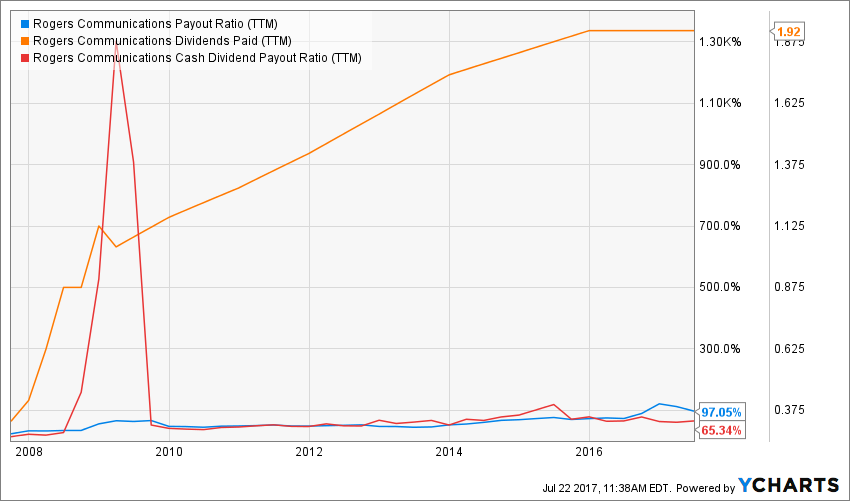

Principle #3: Find Sustainable Dividend Growth Stocks

Past dividend growth history is always interesting and tells you a lot about what happened with a company. As investors, we are more concerned about the future than the past. This is why it is important to find companies that will be able to sustain their dividend growth.

Source: data from Ycharts.

I always find it interesting to compare the payout ratio with the cash payout ratio. As accounting measures often drive us into the wrong direction. With a cash payout ratio of 65%, RCI has plenty of room to increase its dividend.

RCI meets my 3rd investing principle.

Principle #4: The Business Model Ensure Future Growth

I think Rogers decision to focus on sports broadcasting is giving them an edge in the television industry. Streaming companies like Netflix are very far from being able to broadcast live sport events. Therefore, Rogers will be able to capitalize on this advantage for several years to come.

Their wireless business is well protected thanks to the current oligopoly. The company does pay a high price for additional spectrum, but this is also a price to pay to make sure it continues to offer a great wireless service.

RCI still shows a strong business model and meets my 4th investing principle.

Principle #5: Buy When You Have Money in Hand – At The Right Valuation

I think the perfect timing to buy stocks is when you have money. Sleeping money is always a bad investment. However, it doesn’t mean that you should buy everything you see because you have some savings aside. There is valuation work to be done. In order to achieve this task, I will start by looking at how the stock market valued the stock over the past 10 years by looking at its PE ratio:

Source: Data from Ycharts

While the first part of my analysis leads me to like Rogers, this is where I want to get off at the next train station. I’m not sure what justify such high valuation at the moment. It is true Rogers showed strong wireless numbers, but a PE over 30 seems clearly overvalued to me.

Digging deeper into this stock valuation, I will use a double stage dividend discount model. As a dividend growth investor, I’d rather see companies like big money making machine and assess their value as such.

| Input Descriptions for 15-Cell Matrix | INPUTS | ||

| Enter Recent Annual Dividend Payment: | $1.92 | ||

| Enter Expected Dividend Growth Rate Years 1-10: | 5.00% | ||

| Enter Expected Terminal Dividend Growth Rate: | 6.00% | ||

| Enter Discount Rate: | 10.00% | ||

| Calculated Intrinsic Value OUTPUT 15-Cell Matrix | |||

| Discount Rate (Horizontal) | |||

| Margin of Safety | 9.00% | 10.00% | 11.00% |

| 20% Premium | $74.88 | $56.34 | $45.21 |

| 10% Premium | $68.64 | $51.65 | $41.44 |

| Intrinsic Value | $62.40 | $46.95 | $37.68 |

| 10% Discount | $56.16 | $42.26 | $33.91 |

| 20% Discount | $49.92 | $37.56 | $30.14 |

I think Rogers is well established in the cable and internet industry, but the stock is currently overvalued by 40%. Okay… 40% seems rough, but there is definitely not any upside at the moment, even if you use a 9% discount rate.

Source: how to use the Dividend Discount Model

RCI doesn’t meet my 5th investing principle

Principle #6: The Rationale Used to Buy is Also Used to Sell

I’ve found that one of the biggest investor struggles is to know when to buy and sell his holdings. I use a very simple, but very effective rule to overcome my emotions when it is the time to pull the trigger. My investment decisions are motivated by whether or not the company confirms my investment thesis. Once the reasons (my investment thesis) why I purchase shares of a company are not valid anymore, I sell and never look back.

Investment thesis

Rogers is a strong telecom company with a competitive edge in the sport events segment along with a growing wireless division. In a relatively mature market, RCI was able to post a 6% revenue growth for its wireless segment. Management is now focused on cost cutting operations to improve margins.

Rogers is a well-established company in the telecom industry. Its media and wireless segments will continue to show growth in the upcoming years

RCI shows a solid investment thesis and meet my 6th investing principle.

Principle #7: Think Core, Think Growth

My investing strategy is divided into two segments: the core portfolio built with strong & stable stocks meeting all our requirements. The second part is called the “dividend growth stock addition” where I may ignore one of the metrics mentioned in principles #1 to #5 for a greater upside potential (e.g. riskier pick as well).

While RCI’s stock price surged this year, it is more considered a stable blue chip than a rocket powered company. Don’t expect RCI to go up another 25% in the upcoming 12 months, but you can expect to get another dividend payment raise this year.

RCI is a core holding.

Final Thoughts on RCI – Buy, Hold or Sell?

Since RCI is a Canadian dividend aristocrats and it is evolving in a predictable environment, I will continue to hold my shares in my Canadian portfolios. However, I will follow its valuation closely. While I don’t expect much capital appreciation in the future, the dividend payment should be increasing anytime soon.

Disclaimer: I do hold RCI in my DividendStocksRock portfolios.

Each month, we do a review of a specific industry at our membership website; Dividend Stocks Rock. In addition to have full ...

more