Prepared by Stephanie in consultation with Chris/Tara of BAD BEAT Investing

Less than two ago months in April, we encouraged you to take a stab in shares of Party City (PRTY). Our team universally agrees that sub-$8 is probably a good value to start buying and scaling into a position. With shares in the $6 range we pulled the trigger for a trade. The market is giving us another opportunity to get in there for a possible rapid-return trade, or for the more long-term oriented investor, another opportunity to initiate a position at value levels. Shares have rolled over once again and are once again in the $6 range. Sub-$7 we are recommending traders consider a buy in this stock, which has all the makings a deep value play, though some risks persist.

Source: BAD BEAT Investing chartist

In our opinion this is simply overdone. Maybe we are a glutton for punishment but greed is good during times of panic. Especially when there was no news release, and only ongoing risks are helium, moderate debt, and trade spats. Unless there is news of something more daunting waiting in the winds, this seems like opportunity.

The recommended plays

Recommended short-term trade

Target entry: $6.35-$6.55

Stop loss: $6.05

Target exit: $7.35-$7.55

Time frame: Up to a month

Investment--Scale in with percentage position sizing

Entry 1: $6.45 (20%)

Entry 2: $6.05 (30%)

Entry 3: $5.50 (50%)

Medium-term target: $10.00

Fundamental reasons to own the stock

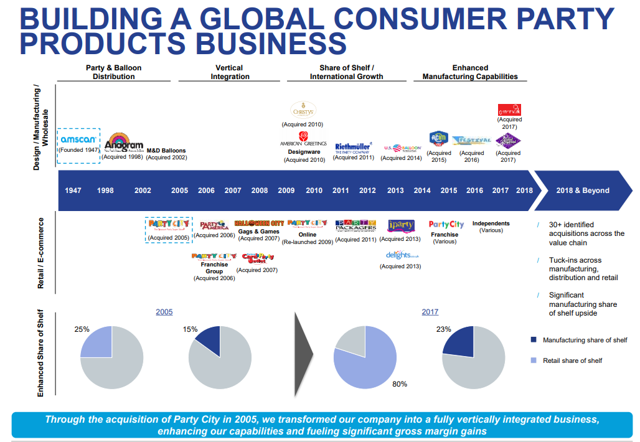

The recommendation is above, but let us talk about the justification beyond a swing trade. Despite our coverage many still have not heard of this name. While this is a small retailer it is perhaps the national leader for party goods and Halloween specialty supplies by sales. This name grew through a series of acquisitions between 2005 and today. It has a really broad and deep product offering for all manner of party occasions. Below is a brief timeline of expansion.

Source: Party City Investor Presentation

This is an impressive timeline of growth. Revenues are in growth mode as are earnings, even if it is low growth. The question of course remains is why is the market pricing this thing as if revenues are about to be cut in half and earnings are going to decline immensely? There is definitely some risk, but we are down 40% from the highs again.

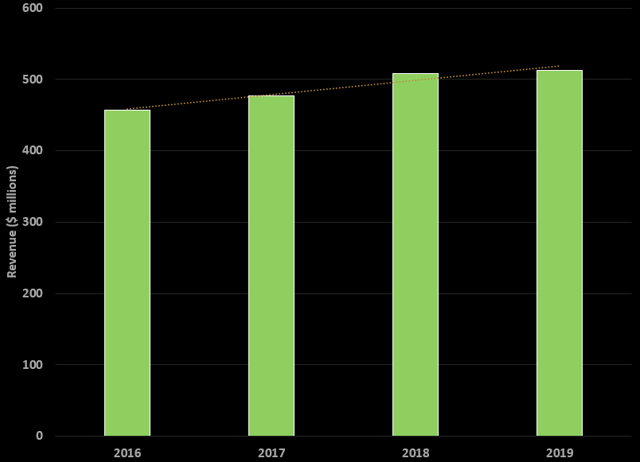

Performance numbers in Q1

In Q1, total revenues increased 1.1% on a reported basis and 2.0% on a constant currency basis. Retail sales increased 4.0% on a reported basis, driven primarily by square footage growth from ongoing store acquisitions. Revenues have grown slowly but steadily in the last few Q1:

Source: BAD BEAT Investing Chartist

The sales picture shows continued growth, but brand comparable sales have been problematic. They decreased 1.4% in the quarter. Sales fell in part due to approximately 200 basis points of headwinds from the helium shortage issue which has been plaguing the company. What is more, net third-party wholesale revenues decreased 6.1% on a reported basis and increased 1.0% after adjusting for the impacts of currency and store acquisitions. As such, total gross profit margin decreased 350 basis points, to 33.7%, due to increased freight and distribution costs and increased commodity pressures, including higher helium costs, as well as a transitional program to optimize stores. We view margins as rebounding moving forward generally speaking.

This takes us to overall operating expenses which totaled $184.4 million or 35.9% of revenues. On the surface this was an increase of 270 basis points from Q1 2018 due to $18 million of impairment and restructuring charges from the store optimization program. If we back out these charges operating expenses were flat with Q1 2018, helping offset helium cost headwinds.

Turning to earnings the expenses led to a GAAP net loss. On an adjusted basis EPS was just $0.01 per share. Adjusted EBITDA for the quarter was $51.5 million. As the store optimization program leads to strategic closings and reduced expenditures, we expect margins and earnings to improve.

Of course, at the end of the day, EPS is what matters. And if the market senses EPS declines, it will hammer a stock. Management and analysts on the most recent conference call, cited helium several times in the last conference call, 41 times to be exact, coming into Q1. Helium continued to weigh in Q1 and remains a prime risk.

The role of helium persists

In our review of the most recent conference call, helium, which is used to fill balloons so they float, was mentioned 41 times by management and analysts, and that matters. In Q1, it was cited that the helium shortage continues to weigh. The helium is currently used to inflate the majority of the company's metallic balloons and a portion of its latex balloons. Party City relies upon adequate supplies of helium and shortages can adversely impact financial performance.

In addition China has driven much of the growth of helium demand. Asia now the largest market for helium demand at 2.1 bcf, surpassing the US which has an annual demand of 2 bcf. China alone accounts for around 33% of global helium demand. What is more, the ongoing tariff strife and trade war between China and the US is also hitting the costs of merchandise. This needs to be watched. Do not forget that Party City operates in a number of foreign countries, many of which are located in Asia. The trade disputes have been an issue to watch, as they can increase costs dramatically.

Debt is another risk that needs to be highlighted which hurts the value case a bit. The company ended the quarter with $1.99 billion om debt (net of cash), resulting in net debt leverage of 5.0 times, and approximately $185 million in availability under its asset-based revolving credit facility. When you couple debt payments with significant lease obligations that it will continue to have, one can see why the market gets spooked if it looks like costs will rise and cash flow is hampered. This substantial level of indebtedness increases the possibility that the company in the future may be unable to generate cash sufficient to pay, when due, the principal of, interest on or other amounts due as far as debt goes, despite current cash flows being solid.

Value still there

Our valuation calculations suggest the stock is a buy here at $6.50, which despite the risks above, we find to be almost unbelievably cheap. We have to take into account guidance. Management guided to ~$1.61-$1.72 in EPS for the year 2019. However, after the stock has been crushed down nearly 50% from the highs again. unless on the next call EPS is guided downward, shares are cheap. At $6 53, there is a current PE of 4.0 and a forward PE of just 3.8 if EPS hits the high side. These are numbers you’d expect from a company in a death spiral, not one that is growing. Free cash flow remains solid.

Take home

This is a value story and we expect a sizable bounce once again following this selloff on no real news. Even with a big helium shortage the possible impacts are not nearly enough to justify the massive selloff we have seen since the last earnings report. We made a great trade on this stock a few months ago and we believe it is time do so once again. Come party with us.

Comments

Log in or sign up to join the conversation.