One Way For High-Yield Energy Midstream Stocks To Boost Share Prices

The midstream energy sector has been a scary place for investors. Despite high dividend yields, it seems that no kind of news will stop the relentless slide in share prices. It has been tough for investors to stick with their energy midstream stock investments, with share values dropping 10%, 20%, or more, even as the rest of the stock market moves higher into record territory. I am convinced that midstream stock values will turn around, and I have a trigger event/”cure” to look for, which will signal higher share prices on the horizon.

Energy midstream companies gather, process, store, and transport energy commodities, crude oil, natural gas, and fuels from the producers to the end-users. In 2014, most of the companies were organized as master limited partnerships (MLPs). Midstream, along with the rest of the energy sector, went through a deep bear market from late 2014 until early 2016.

The sector crash pushed many midstream companies into big restructuring plans. Growth projects were restructured or canceled, balance sheets were tightened up, the MLP structure was changed or modified, and a lot of dividends were reduced. In fact, for the 2019 third quarter, it was the first quarter in well over a year when not a single MLP reduced its dividend rate, and half announced rate increases.

The investing public has not forgiven the midstream sector for the dividend cuts and is ignoring the much stronger financial fundamentals of all the companies in the group. Share prices continue to drop, which causes more investor pain, which leads to more selling, which leads to further value declines. The investing public is ignoring the substantial improvement in fundamentals out of the midstream sector. There appears to be nothing that will get more investors interested in the sector, which would stimulate buying and share price appreciation.

Eventually, a business sector with solid economics that pays excellent dividends will recover. I am ready for the selling to end, and here is what I think will trigger a turnaround in share prices.

These companies need to institute and follow through with meaningful share buyback programs. Buying in shares will give demand to the stocks and at the same time, increase free cash flow per share to grow future dividends. Here are three midstream companies that have or should soon institute buyback initiatives.

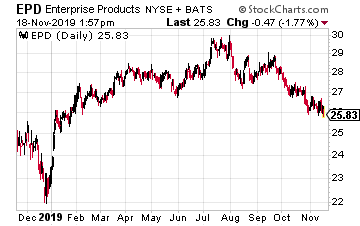

Enterprise Product Partners LP (EPD) is the largest publicly traded MLP, with a $58 billion market cap. It is among the largest energy midstream companies of any corporate structure.

Enterprise is in a serious growth mode, with $9 billion of major capital projects under construction.

This conservative, growth-focused company has not been immune to the sector selloff, dropping 15% since mid-Summer. For the third quarter, the company reported distributable cash flow (DCF) of $1.6 billion, which provided 1.7 times coverage of the distributions paid to investors.

The $600 million-plus in excess cash flow goes a long way to pay for growth projects. I would like to see a portion of that cash allocated to share buybacks. I think it would help the EPD unit value.

In August the company shifted to buying shares in the open market for its DRiP and Employee Unit Purchase Plan. 1.4 billion units were purchased for this purpose in the third quarter.

EPD currently yields 6.2%.

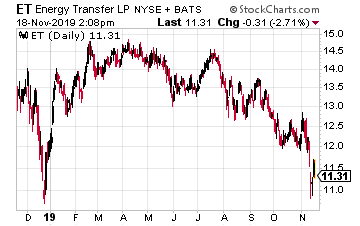

Energy Transfer LP (ET) is a $29 billion market cap midstream company. For the third quarter, ET generated $1.52 billion of distributable cash flow. The DCF provided 1.88 times coverage of the dividends paid, or put the other way; there was $712 million of excess cash flow.

Now think about this: Energy Transfer is a $30 billion company generating $6 billion of free cash flow per year. Even with the tremendous cash flow coverage of the distributions, ET yields almost 11%. This company should be close to double the current market value.

A share buyback program would be hugely accretive to the cash flow per share. I think this is the one stock in the sector where a buyback and some share price gains would trigger a rally for the entire sector.

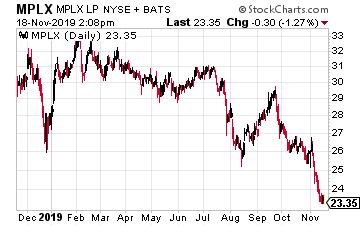

MPLX LP (MPLX) is a $25 billion MLP that primarily provides midstream services to refining company Marathon Petroleum Corp. (MPC). Marathon is also the largest owner of MLPX units.

MPLX third quarter DCF was $1.0 billion, providing 1.42 times coverage of the distributions.

This is an exciting combination because MPC is buying in $500 million of the refining company’s shares each and every quarter. It would be a benefit for MPC if MPLX also initiated a share buyback program.

The MLP units yield 11.25%.

Disclaimer: The information contained in this article is neither an offer nor a recommendation to buy or sell any security, options on equities, or cryptocurrency. Investors Alley Corp. and its ...

more