Nike: Don’t Buy This Dow Stock, Despite Its Growth

Athletic apparel juggernaut Nike (NKE) has seen its shares rally nicely in 2019. The stock began the year in the mid-$70s after a tough end to 2018 and has rallied alongside the broader market since then, settling in the mid-$80s today. Nike stock is only a few dollars away from its all-time high achieved in April of 2019.

Nike is one of nearly 700 consumer cyclical dividend stocks, a group of companies that compete in a variety of cyclical industries leveraged to consumer spending. More importantly, Nike is also a member of the Dow Jones Industrial Average, a group of 30 large stocks in the U.S. representing a variety of sectors and industries.

The company’s dividend has experienced strong rates of growth in the past decade and that is something we certainly see continuing. However, the share price, near its all-time high, has created a less favorable situation for investors as the stock is now quite expensive.

In this article, we’ll take a look at the value proposition the stock offers, as determined by our Sure Analysis Research Database, where we rank stocks based upon total expected returns.

Nike’s low expected total returns are principally the result of the strong rally in the stock and the resulting overvaluation. Because of this, as well as the low dividend yield, we currently have a sell rating on Nike despite the company’s future growth potential.

Company Overview and Current Events

Nike was incorporated in 1967 in Beaverton, Oregon, where it is still headquartered today. The company is the product of a partnership between a high-profile track and field trainer name Bill Bowerman, and the company’s long-time leader, Phil Knight.

Nike began as an athletic retail store and in 1972, the Nike brand was born with the introduction of the Nike Cortez, a track and field shoe designed by Bowerman. Based upon the success of the company’s Nike-branded shoes, the company was renamed Nike, Inc. in 1978, and went public shortly thereafter.

Since then, Nike has expanded its scale and reach exponentially and today is present all over the globe. The company’s brands now include Nike, Converse, Hurley, and Jordan.

Nike-branded product offerings are made in six key categories: running, basketball, Jordan, soccer, Training, and Sportswear. In addition, the company markets products designed for kids, as well as products for a variety of sports and other outdoor activities. The Nike brand today is a full-service athletic outlet that provides just about anything an athlete of any age would need to compete in a variety of sports, and is not limited to apparel and shoes.

The Jordan brand designs distributes and licenses athletic apparel, footwear, and accessories using the Jumpman trademark made famous by basketball legend Michael Jordan. Converse designs distributes, and licenses casual shoes, apparel, and accessories under a variety of related brands, and this brand is reported as a standalone segment. Hurley offers a line of action sports and youth lifestyle apparel and accessories and is reported within the Nike brand’s North America geographic segment.

Today, Nike offers its products through thousands of retail and distributor points throughout the world, as well as about 400 of its own stores under the Nike, Converse, and Hurley brands.

The stock has a market capitalization of $135 billion and Nike should produce about $39 billion in total revenue this fiscal year.

Nike reported fiscal Q3 earnings on March 21, 2019, and results were characteristically strong. The top line rose 7% year-over-year to $9.6 billion on a reported basis. Excluding Nike’s significant exposure to currency translation given its highly global sales base, total revenue would have risen an even more impressive 11%.

Revenue for the Nike brand was up 12% on a currency-neutral basis to $9.1 billion, driven by growth across wholesale and the company’s Nike Direct business. Strength was seen from the sportswear and Jordan categories, respectively, while footwear and apparel continue to post double-digit growth rates.

The Converse brand saw its revenue down 2% on a currency-neutral basis, coming in at $463 million in FQ3. The decline was driven by shrinking revenue in the U.S. and Europe, which were partially offset by double-digit growth in Asia and the brand’s digital channel. Converse has struggled for some time and certainly represents the weakest of the company’s brands.

FQ3’s revenue gain of 7% is impressive, but sales for the first three quarters of the year are up a combined 9%, exhibiting the top line strength investors are accustomed to seeing from Nike.

Gross margins increased 130 basis points in FQ3 to 45.1%, driven by higher selling prices, growth in Nike Direct, as well as favorable changes in foreign exchanged rates. Higher product costs partially offset some of these gains, but FQ3 was a strong showing on the gross margin front. Nike is building upon strength from the first half of the fiscal year, as the company’s gross margins were up 90 basis points to 44.4% for the first three quarters of the year.

Selling and administrative expense, or SG&A, increased 12% in FQ3 to $3.1 billion. Demand creation was $865 million during the quarter, which was flat from last year. This is Nike’s version of research and development as its team of designers create the next wave of products to sell under the company’s brands.

Operating expenses increased 17% in FQ3, primarily driven by higher wages, reflecting strategic investments in the company’s Consumer Direct Offense. This is the company’s renewed focus on providing athletic apparel to athletes of all ages around the world at significant scale, focusing on the opportunities with the greatest potential for returns.

Earnings-per-share came in at $0.68 in FQ3 thanks to strong revenue growth, gross margin expansion, a lower tax rate, and a lower share count, some of which was slightly offset by higher SG&A costs.

Nike doesn’t buy back a lot of stock, and for what it does buy, it largely reissues it as compensation to employees. Still, the share count was ~1% lower year-over-year, helping to boost earnings-per-share growth.

Growth Prospects

For fiscal 2019, we see earnings-per-share of $2.65, which would represent year-over-year growth of just over 10%.

Looking forward, we see Nike producing 10% annual earnings-per-share growth in the coming five-year period. Indeed, as this image from the company’s website shows its commitment to growing, as it has for the entirety of its existence.

Source: Company website

Since the company’s founding, Nike has focused on growth at what seems to be any cost. Nike breaks out demand creation expense in its income statement to illustrate how much it is dedicated to creating the next generation of excellence in athletic apparel and footwear.

The upside to this commitment is obvious; Nike has been able to grow its earnings by leaps and bounds at times in its history.

Since 2007, Nike has managed to compound its earnings-per-share by nearly 12% annually, a very impressive track record considering that period contains the Great Recession. There aren’t many companies in any industry that can claim such a strong history of growth.

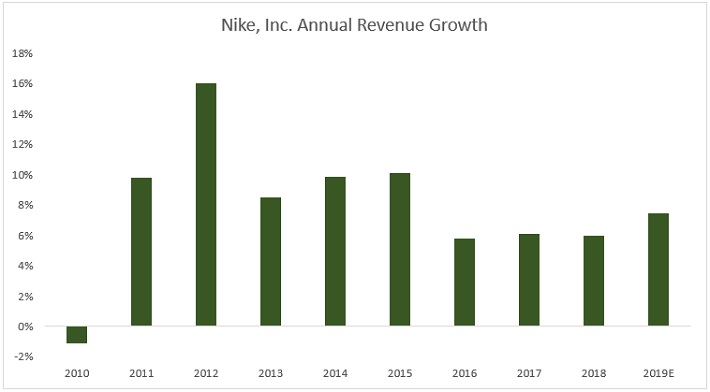

(Click on image to enlarge)

Source: Company financials

Indeed, Nike’s revenue growth over the past decade has been nothing short of outstanding, posting nine years of gains and one lower year-over-year revenue total, a 1% decline in 2010. Apart from that small hiccup, Nike has averaged ~9% revenue growth since 2010, and we see high-single-digit top-line gains as the key driver for earnings growth in the future.

Revenue growth should continue nicely for Nike in the coming years thanks to continued penetration in China, as well as growth in North America, Converse excluded. Nike states that 2 billion people in areas like China, India, and Latin America will join the world’s middle class by 2030.

These consumers will have disposable income unlike what they have today, providing potential revenue streams for providers of discretionary items, as is the case with Nike. Revenue in China grew a staggering 21% in 2018, and we expect the world’s most populous country to be a significant growth driver for Nike for years to come.

The company’s Consumer Direct Offense plan combines Nike’s desire to do three things well to drive the next stage of growth for the company. It is focused on Speed, Direct, and Innovation, providing the company with an emphasis on creating the right products, such as its relatively new wearables category, and getting those products to consumers quickly, and via the right channels.

Nike’s focus on prudent spending and initiatives like speed-to-market have left a bit to be desired by investors in the past. Nike spends freely on demand creation and other SG&A categories, including issuing stock to its employees.

The company’s philosophy has always been to grow at just about any cost. We don’t see that changing, which is why margin expansion will likely not be a meaningful factor in future growth.

Expected Returns

In the coming years, we think Nike will produce just under 4% in terms of total annual returns. Nike stock returned -37% in 2018, and have returned ~16% thus far in 2019. In our view, the strong returns from the past 18 months or so have priced in a lot of the company’s future growth, meaning that returns from here will likely be limited by the high valuation.

Today, Nike shares trade for 32.3x this year’s earnings estimate of $2.65 per share, which is the highest valuation the stock has traded within the past decade. Our fair value estimate is 22x earnings based upon the company’s projected growth rates, as well as its own historical valuations.

That means the valuation alone, should it revert back to a more normalized state, would represent a 7%+ headwind to total returns for shareholders each year for five years. Even with 10% projected earnings-per-share growth, that is a sizable headwind to overcome. Nike shares are very expensive today, trading for 146% of our fair value estimate, making it one of the most expensive stocks by this measure in our coverage universe.

The final piece of the total return puzzle, in addition to earnings-per-share growth and change in the valuation, is the dividend yield. Nike has raised its dividend at rates roughly congruent with earnings growth in recent years. However, Nike typically has a low dividend yield, and the soaring stock price in recent years has blunted the impact of the dividend increases.

Today, shares yield just 1%, so Nike is hardly considered an income stock. We do see meaningful payout growth continuing as the company’s payout ratio is still only in the mid-30% area, but those looking for a high yield must look elsewhere.

Given the relatively weak projected total returns in the low-single digits, we currently have a sell rating on Nike. We acknowledge that Nike is one of the best large-cap growth stocks in the Dow, and likely will remain as such for years to come, but also acknowledge that the valuation of the stock has reached alarming heights.

Final Thoughts

We very much like Nike’s fundamentals and its growth potential in North America and emerging markets such as China. However, the company’s gross margins have flattened in recent years, it spends heavily on SG&A costs, and much of the company’s buyback spending is absorbed as compensation expense as shares are reissued to employees.

Most significantly, however, Nike’s valuation is at very high levels. We see the current valuation as nearly 50% above our target. Even though Nike is likely to continue growing earnings going forward, this growth appears to be more than priced in.

As a result, we rate Nike stock a sell. Investors looking to own Nike should wait for a significant pullback closer to our fair value target of $58. On a pullback to that price level, Nike would likely represent a strong buying opportunity.

Disclaimer: Sure Dividend is published as an information service. It includes opinions as to buying, selling and holding various stocks and other securities. However, the publishers of Sure ...

more