New Research Tries To Solve For Beta Risk’s “Failure” For Stocks

At the core of modern finance is the proposition that beta (market) risk is the dominant factor that drives performance. But numerous empirical tests of the capital asset pricing model (CAPM) over the decades suggest otherwise. There have be various attempts to adjust CAPM to find a closer mapping of risk and return, but the results have been mixed. Perhaps two new research papers move us closer to the elusive goal of revising a CAPM-based view of asset pricing so that its theoretical ideal for risk and return moves closer to empirical results in money management practice.

Before we briefly look at the research, let’s note that beta risk works much better in an asset allocation framework compared with using CAPM within asset classes. Plotting historical returns vs. beta for asset classes reveals a relatively robust relationship. The main challenge is within asset classes. In particular, many studies over the years demonstrate that the relationship between stocks and equity market risk overall is weak. In some research, beta risk appears to predict the opposite of what CAPM anticipates. That is, certain empirical studies show that low betas lead to high returns and vice versa–the basis for why so-called low-volatility strategies can outperform standard market-weighted portfolios.

Various efforts to refine the idea that higher risk does in fact relate to higher return for a basket of stocks has led to various modeling enhancements. The most famous is the Fama-French three-factor model that identifies beta risk in three flavors (market, valuation and capitalization) rather than the single factor market beta of CAPM.

As the years have passed, many innovations have been presented, delivering an ever-expanding suite of x-factor models. Two new and intriguing additions to the alternative methodologies introduce a so-called investor beta to the mix and a business-cycle variation of the Capital Asset Pricing Model.

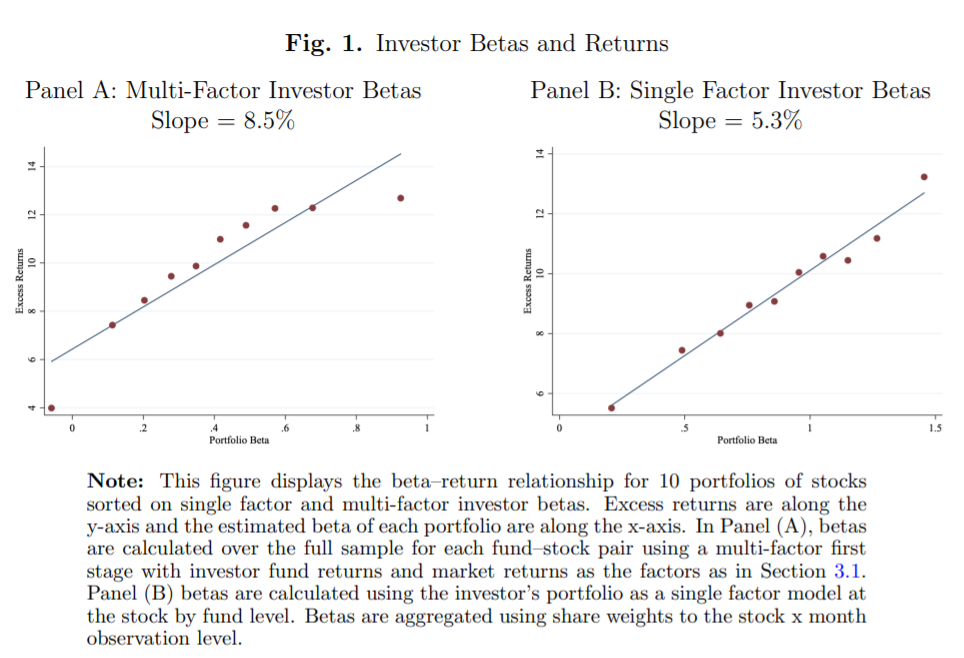

Let’s start with the investor beta model. The idea of “Investor Betas” (Ryan Lewis and Shrihari Santosh at University of Colorado, Boulder) is a model that “implies that an asset’s expected return is linear in its average idiosyncratic beta with respect to each active investor’s portfolio return.”

The key takeaway: “investors appear to be compensated for holding stocks that have a high covariance with the idiosyncratic component of their portfolio.” In other words, the authors identify “a strong risk-return trade off when we account for the fact that investors deviate from the market portfolio in their holding choices and therefore face ‘idiosyncratic’ risk.”

The crucial step is estimating the “idiosyncratic” beta for each stock in the portfolio and then averaging those betas. Lewis and Santosh report: “Aggregated across funds, betas are positively related to stock returns in the cross-section of stocks. Investors receive 5%-10% additional return per unit of risk related to their portfolio.”

The primary concept of the paper is captured in Figure 1 (see below), which illustrates the positive relationship between risk and return that’s identified via the idiosyncratic risk modeling.

(Click on image to enlarge)

Another recent attempt to provide a more tractable explanation for a CAPM-inspired view of markets: “A Business Cycle Capital Asset Pricing Model” by Wai Man Tse at Chu Hai College of Higher Education. The paper outlines an asset pricing model “that captures the market, liquidity, credit, and business cycle risks. The explicit incorporation of economic-phase-switching business cycle risks with rational expectations makes the predicted return volatility equal to the observed return volatility.”

Notably, the business-cycle model makes outlines a degree of progress in resolving long-standing issues related to excess volatility and the so-called equity premium puzzle that have challenged standard finance theories. But as this paper reports, “concerns over excessive volatility and equity premium puzzle become insignificant” via business-cycle modeling.

A crucial observation of the paper: “not all risks lead to a positive risk premium because the underlying economic dynamics, the business cycle, is mean-reverting.” For example, “the model demonstrates that credit risk relates to both momentum and reversal because it is represented by the difference between current and past moving average returns.”

Although this model is more complicated than the standard CAPM, the author reassures readers that the necessary data inputs are “as readily obtainable as those needed by CAPM.” As such, the model appears to be practical as well as empirically significant.

Both papers extend and enhance a long-running line of research efforts to adjust the original CAPM for application in the real world. The results are hardly silver bullets, in part because out-of-sample testing still awaits.

Meantime, the relation between risk and return is still more complicated and nuanced than standard finance theory allows. By incorporating more of this nuance and complication into the modeling process, however, the results appear to be more valuable for designing and managing portfolios.

CAPM, in short, is still challenged, but it’s far from dead.

Disclosure: None.