Netflix’s Price Increase Signals Original Content Isn’t Enough

Netflix’s Price Increase Signals Original Content Isn’t Enough

Netflix (NFLX) announced a price increase that will affect new U.S. members immediately while existing members will see the changes “over the next several months.” We’ve recently seen the impact that price increases can have on Netflix’s membership growth, when the company blamed poor 2Q16 growth on cancelations due to a price increase. Will the latest price increase have the same effect? In the larger context, we believe the price increase signifies that Netflix’s competitive advantage has been wiped away. In order to justify its massive original content budget, it must raise prices if it is to ever meet the expectations implied by its stock price.

Competition Is Eroding Netflix’s Business Model

The streaming video market has grown dramatically and Netflix has lost much of its early-mover advantage as we detailed in July 2016. Today, the market is highly fragmented with competitors offering live TV bundles, original content, and exclusive access to content from certain movie studios to attract customers. Competitors are also eating away at Netflix’s business model by removing content from the service. Disney recently announced a standalone streaming platform with all Disney content, including Marvel and Star Wars. Fox has been pulling its content from Netflix over the past few months and making it available via Hulu. Meanwhile, Apple has plans to invest billions into original content that it is streaming via its Apple music service.

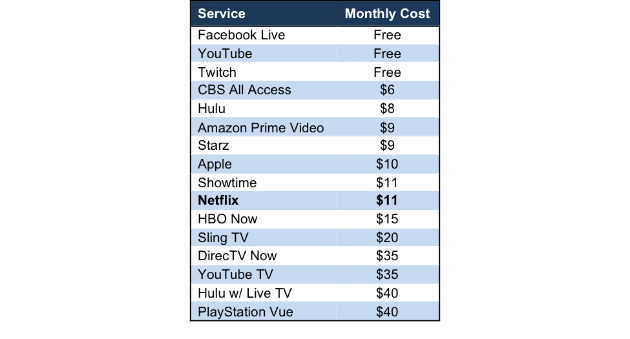

Worse yet, Netflix’s pending price increase limits its pricing power over the competition, per Figure 1. The competitors in Figure 1 also include live TV offerings, such as Sling TV and DirecTV Now.

Figure 1: Streaming Market Competition

Sources: New Constructs, LLC and company filings.

The increase in competition leaves limited pricing power, a lynchpin for the viability of Netflix. Without pricing power, Netflix can’t afford to continue to do all the things that have helped management hype the stock, such as invest in growing original content, attracting new members and maintaining its large content library. As we have written for some time, investors will not tolerate huge cash flow losses forever. Now, with ample competition, it’s clear Netflix’s only value is in its costly original content.

The recent revelations that competitors are willing to pull content from Netflix and start their own service indicate that Netflix’s business model is completing its shift to a traditional TV network, even if not by its own choosing.Accordingly, all investors, not just the bankers and insiders, should beware especially since the valuation of the stock is yet to recognize the cracks in the Netflix bull thesis.

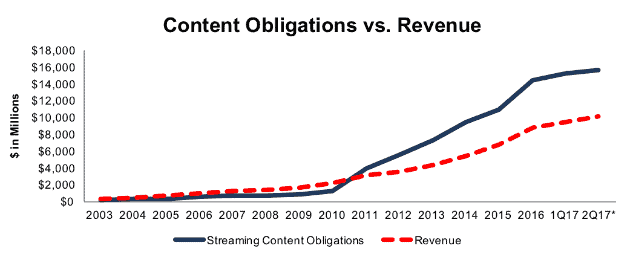

Content Costs Continue to Outpace Revenue Growth

With plans to spend $6 billion on content in 2017, Netflix’s streaming content obligations continue to grow faster than revenue. We first warned about Netflix’s alarming streaming content obligation growth in 2014. Since then, the issue has only worsened as free cash flow has fallen further.

Since 2010, content obligations have grown 43% compounded annually while revenue has grown 25% compounded annually, per Figure 2. At the end of 2Q17, content obligations totaled $15.7 billion and have grown faster than revenue YoY in six of the past seven years. The realities of Netflix’s costly business model are finally catching up to the firm.

Figure 2: Content Obligation Growth Outpaces Revenue

*Revenue from the trailing twelve months

Sources: New Constructs, LLC and company filings

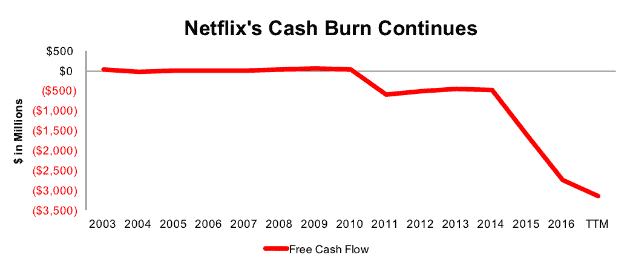

Cash Burn Compounds Obligation Growth Issues

As Netflix’s content obligations increase, its free cash flow (FCF) only grows more negative. Since 2010, the last year Netflix generated positive FCF (and first year it began increasing its content library), Netflix has burned through a cumulative $6.4 billion in cash, per Figure 3. Netflix’s FCF over the trailing twelve months sits at -$3.1 billion, the largest cash burn reported in Netflix’s history.

Figure 3: Netflix’s TTM Free Cash Flow is -$3.1 Billion

Sources: New Constructs, LLC and company filings.

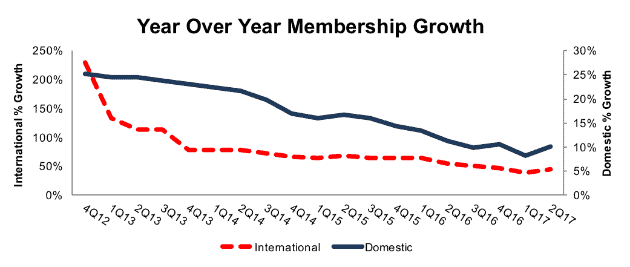

Price Increases Have Hurt Membership Growth

In 2Q16, Netflix missed membership growth expectations and blamed the slow growth on customers cancelling the service ahead of a planned price increase. Per Figure 4, Netflix stopped a long-term trend in slowing membership growth in 2Q17. The newly announced price increase could see as similar impact as 2Q16 and halt the membership growth trend reversal in its tracks.

Per Figure 4, international members grew 44% YoY in 2Q17, down from 55% in 2Q16 and 78% in 2Q14. Similarly, domestic members grew 10% YoY in 2Q17, down from 11% in 2Q16 and 22% in 2Q14.

Figure 4: Netflix’s Membership Growth Rates

Sources: New Constructs, LLC and company filings.

NFLX Valuation Remains Unrealistically Optimistic

Figure 5 shows the striking valuation gap between Netflix and TV networks such as CBS, Viacom, and HBO parent Time Warner. Despite having a similar return on invested capital (ROIC), Netflix is valued with an Enterprise Value/Revenue ratio between 2-4 times higher.

Figure 5: Netflix Is Much More Expensive Than TV Networks

Sources: New Constructs, LLC and company filings.

Assuming a 2.7x multiple (average of TWX, CBS, and VIAB) to TTM revenue of $10.8 billion, NFLX is worth $51 share – a 72% downside.

One could argue that NFLX deserves a premium over these other stocks due to its international growth opportunities and popularity among younger viewers. Still, it’s hard to justify the massive premium at 8.4. Furthermore, TWX, CBS, and VIAB actually generate significant free cash flow and have sustainable competitive advantages. They also have a customer base that includes nearly every household with a TV – or 118.4 million homes to which networks can advertise. How does Netflix stand a chance or, much less, deserve a premium valuation?

Disclosure: David Trainer and Kyle Guske II receive no compensation to write about any specific stock, sector, style, or theme.

Damn, I gotta sell my Netflix shares! Bye bye $NFLX

They lost $2.8 billion in 2016.

Over the trailing twelve months - free cash flow is -$3.1 billion.

Wall Street loves the stock and the firm's strategy b/c it will generate lots of underwriting fees for all the debt and stock NFLX can sell to the suckers willing to fund a business model that has not made money 2010 when free cash flow was $29 million.

Since 2002, free cash flows is -$9.4 billion, cumulatively.

Seeing the cold, hard numbers has really opened my eyes and completely changed my opinion on $NFLX.

Thank you @[David Trainer](user:4666), those are some pretty sobering facts!

Thanks @[Harry Goldstein](user:15520).

Understanding how far off they are from profitability today helps investors see the real risk in the stock.

Excellent article. I couldn't agree more.

Good comment thread. Yes, #Netflix has much to offer and a rabidly loyal customer base. But the financials can't be ignored either. And unlike TV networks, they can't make up additional revenue in advertising without alienating the very customers whose loyalty the company relies on to survive.

I believe the solution is to take a page from #Disney's book and focus more on licensing. Sure Disney made billions of people paying to see it's lovable princesses, and other cartoon characters, not to mention the Star Wars franchise. But they've many more billions off the licensing of these characters.

Netflix has come up with some really top tier original content for both adults and kids. Not to mention brought over some cancelled shows which already had cult followings. They should leverage these character with licensing opportunities and bring a much needed additional revenue stream. $NFLX $DIS

I like this idea. I doubt Netflix characters are as iconic as Disney's, But yes, there's certainly money to be made in licensing.

That's a really great idea. But if #Netflix really wants to generate more revenue, all they have to do is stop letting people share accounts with others who don't even live with them. Almost everyone I know has #Netflix. Virtually none of them pay for it themselves. Either they share an account with friends, or just use a relative's login. I don't get why #Netflix allows this to continue.

As a Netflix investor, this is a great suggestion. As a Netflix user, I really don't want to have to start paying for my own account! ;-)

Lol, couldn't agree more.

Netflix has to do this so that family members can share an account. I know that my children want to watch cartoons, while I may be watching House of Cards. To force them to buy their own account would be a deal breaker for me. By the way, Amazon has always let people share a Prime membership also..

Actually @[Dick Kaplan](user:7622), that's not quite correct. Amazon let's people at different addresses share 2-day free shipping, but not the Instant Video and other benefits. Only members of the paying household get that benefit.

Netflix, can and should do the same thing. They could have people at the same physical address share an account, but not those at other locations.

I stand corrected. But the argument is still valid - what happens when my child has a sleepover, or goes to visit grandma or eventually goes off to college. Should they have to buy a separate account?

That's a good point. But technically, couldn't you give anyone your Amazon login and then they could watch instant videos too?

Good back and forth. Clearly this solution isn't as easy as Justin (nor I) originally thought. The truth is, Netflix is spending billions creating original content. Which, while we all enjoy consuming that content, won't bring in enough new subscribers to cover the cost.

Yes, I suppose that's true Howie, but then they would have access to much more sensitive info. Such as your credit card info, product order history, etc. I know I wouldn't want people necessarily seeing my order history!

Another good point, I hadn't thought about that. But I wouldn't have those same qualms about handing over my Netflix login. How could Netflix ever know if I am logging in, or someone else I simply entrusted my login credentials to?

Good points - and the back and forth here illustrated the challenges Netflix has to making money. Not sure how they will ever make the kind of money they need to make to support original content creation.

Understanding how far off they are from profitability today helps investors see the real risk in the stock.

I think #Netflix is the clear leader in the streaming space and even the major competitors like the #Amazon powerhouse with it's edge in compatible hardware or extra benefits (like Prime shipping) or companies like #Sony with it's vast libraries of videos can't compete.

Netflix has the largest offering, the most critically acclaimed original content, the best tech and the most loyal fanbase. While the companies financials could be better, the fact that they've been able to take it's first mover advantage and persevere despite the intense competition shouldn't be so quickly dismissed.

Unlike most products they can continue to raise prices and I and many others would continue to pay. $NFLX $AMZN $SNE

While I don't doubt that you and many others would continue to pay despite additional membership fee increases, the fact is, many more wouldn't. if you read Mr. Trainer's article, the charts clearly show that the price increases directly cause a decrease in subscribers.

Not just persevere, but excel and obliterate the competition. Don't forget that many said #Netflix's days were finished when #Walmart, #Blockbuster and others tried to compete with them. Which of those other companies are still standing? Only one! $NFLX

What do you mean? #Walmart is still around. $WMT

Yes, Walmart is still around as a company, but not as a competitor to Netflix. The company abandoned this space and sold this division, including all of it's video customers to Blockbuster. But even with the additional customers, Blockbuster went the way of the dinosaurs and only Netflix remained. There are now new competitors but I believe Netflix will likely triumph once again.

"As we have written for some time, investors will not tolerate huge cash flow losses forever." Sadly #Netflix and others have so far proven this thesis incorrect. I do however agree that they should not. The simple fact is, although the stock price rises, their model is becoming more unsustainable, not less. $NFLX

I don't think that's so clear cut. #Netflix hasn't raised it's prices much and is still a bargain for what it offers. Netflix is still much cheaper than #Hulu which charges $11.99 per month (for no commercials, like Netflix). On the contrary, I think that this increase is meant to fuel a greater investment in it's original content since this is one area where others can't compete (at least not without investing billions themselves). And even then, loyal fans will stay with Netflix for it's original shows which they have come to love. $NFLX.

The issue isn't their service. Fortunately their sales in the US is growing. For a while they were relying on foreign expansion to grow. The issue is their finances which remain sub par. However, many companies in this low growth economy and low interest rate environment are adding on debt, so the model works until it doesn't.

By the way, they are raising prices this year. I am refuting the statement the author put forth saying the market won't tolerate their losses. As I stated, Netflix and others have proven those focusing only on their bad finances wrong for years now. however, people still should be aware of it.

I think #Netflix users are a bit like #Apple fan boys. They love the product so much, they are blind to any detractions, even when valid and critical to the company's long term health. I think we can all agree, Netflix has a wonderful product with many satisfied users. But the financials don't lie and can't be ignored.

@[Michele Grant](user:4854) - excellent point!

All good points, thanks for clarifying.