Muscle Maker Grill Positioning For Growth Through Acquisition And Expansion

Source: Muscle Maker Grill

- MMG raised $10 million via private placement.

- MMG plans to open more locations.

- MMG is likely to acquire complementary targets like superfit foods.

Muscle Maker, Inc. (GRIL) just announced its plan to raise $10 Million via a private placement with a lone U.S. institutional investor. While restaurant businesses are trying to find their footing, Muscle Maker has found the sweet spot that allows it to grow in any environment, pre and post COVID. Investors buying the recent dip in price could soon be rewarded with a paradigm-changing acquisition that puts the $10 million to good use and gets pricing on par with the smart money that just invested. The big question is: what will this cash be used for? In this article, we will show how the market misunderstood the above-the-market equity raise GRIL conducted, and how the company is poised for growth over the next year. It appears shares are significantly undervalued compared to other Quick Service Restaurant (QSR) brands.

Details of the Private Placement

The recent raise of $10 million included the issuance of 1.25 million shares of common stock, a pre-funded warrant to acquire 2.865 million shares of common stock, and a common stock purchase warrant to acquire 4.12 million shares of common stock exercisable at $2.43 per share.Due to the nominal $.01 exercise price of the pre-funded warrants it basically means that 4.12 million shares were traded for approximately $10 million which represents an above-market transaction at $2.43.Many restaurant businesses are on the brink as a result of the recent pandemic and the team at Muscle Maker believes this creates the perfect environment for acquisitions. Muscle Maker is evaluating opportunities and hopes to implement its business plan in the near future. If the remaining 4.12 million warrants at a strike of $2.43 with an expiration of 5.5 years were exercised in full by the investor, it would yield an additional $10 million in capital for the company. With shares trading way below the recent deal raise price, investors have the chance to participate in the fundraising with institutions. Many restaurant businesses are on the brink and that is a perfect time for money to strike. It's very obvious that GRIL is in acquisition mode based on how quickly this deal came together. The quick funding points directly toward a pending acquisition, and this speaks to the demand for their products and locations, as well as intense investor interest—it is quite uncommon for a raise like this for such a small company to be conducted just with one investor. When reading the tea leaves of GRIL’s corporate update, it's clear anacquisition is pending and might fit the parameters of an expandable business with a great brand of convenient food in the fitness and health market. The question is: what will their next acquisition be and what will it look like?

According to Muscle Maker’s Update:

“As mentioned in other filings, updates and press releases, Muscle Maker, Inc. will continue to be on the lookout for accretive strategic acquisitions. Our strategy continues to be to develop and grow the company using non-traditional approaches and locations to get healthy food in consumer’s stomachs. It is our intent to continue to organically grow by opening new strategic locations on military bases, universities, fresh-prepared meal prep delivery and ghost kitchens. However, we also believe an expedited way to drive revenue and performance is to acquire profitable strategic assets when possible. Our approach is to analyze companies we believe follow our philosophy of healthier eating while also being unique in how they operate. This can be via non-traditional locations or simply how they get food to consumers. We believe there will be multiple acquisition opportunities that will present themselves in the wake of Covid-19.”

Muscle Maker Grill’s Strategy: Non-traditional Assets

Muscle Maker took advantage of the pandemic and the drastic changes in customer habits by doubling down on non-traditional foodservice - their focus is on non-traditional location opportunities - delivery-only ghost kitchens, military bases, and universities. As of now, they have 32 locations as well as 4 campus locations that are ready to open when universities are expected to open back up in the fall. The company is acquiring concepts that are accretive to the top line as well as companies that succeeded during the pandemic—thriving companies, not struggling companies.

Source: Muscle Maker Grill's Facebook

New QSR Trend: Ghost Kitchens

Ghost kitchens are a concept where food is prepared and then shipped out using delivery services, as to avoid the dine-in of a traditional restaurant, which was the primary issue for restaurants during COVID-19. Consumers are expected to, even after the pandemic, continue to use these non-traditional methods to eat such as third-party delivery services like Uber Eats (UBER) and the partnership between Grubhub (GRUB) and Lyft (LYFT), ghost kitchens (a focus of GRIL), and meal prep like Blue Apron (APRN) or Hello Fresh (HLFFF). Interestingly Grubhub was just bought for Just Eat Takeaway (TKAYY) for $7.3 billion in an attempt to grow over predominant USA-based peers such as DoorDash (DASH). This is a really hot space for industry growth and new consumer habits as Walmart (WMT) and Amazon (AMZN) are now competing, as well as more traditional players like Papa Johns (PZZA).

Additionally, ghost kitchens are likely to become more popular in the future, and GRIL is set up well for this transition. As minimum wages are expected to increase over the next four years to a potential federal minimum of $15, ghost kitchens are expected to be a more profitable way to run a restaurant-type business with labor costs being almost half of a traditional dine-in restaurant, on average. Thus, GRIL is positioned for the future.

Fortunately, GRIL is not competing directly with these gargantuan companies, as they are focusing on low-carbohydrate diets, meal plans, convenience, and healthy food, in locations that these giants are not playing in as much such as universities and military bases. Additionally, GRIL’s business model is to franchise, which is the growth strategy of extremely successful QSR businesses such as Chick-fil-A and McDonald’s (MCD), though its food is probably more popular among those consumers who prefer a non-franchised QSR brand Chipotle (CMG), which generally offers more well-balanced meals.

The difference is that GRIL is primarily operating in the interesting niche of military bases and universities—where its menus are likely to be popular—while also pursuing growth in traditional locations. They now have a $10 million pot of money and are looking to put it to work right away. Physical locations are back in play and they are going at fire-sale prices. What a great time to buy, and this is part of their overall plan to scale the business, and investors have a chance to get in just about where smart money recently bought in with this offering.

Source: delimarketnews.com

The exciting thing is that the lockdowns seem to be over and governments are now allowing more socialization. People want to go out to eat again. So, as many foodservice and restaurants have been struggling GRIL is likely going to acquire a business that is very discounted from its true value, which is why GRIL so quickly got money—so, the next acquisition is probably going to be a good one. It is important to remember that even with lockdowns coming to an end, the pandemic will still be a bit of a problem with viral variants, and so people will likely continue to buy from brands that have strong presences in delivery such as GRIL.

We expect to see consolidation in the only segment of the market that’s working, and we expect GRIL to grow organically and inorganically. According to GRIL’s corporate update, the acquisition of Superfit Foods comes down to buying ~$2.1 million in revenue, growing at a rate of at least 10% per year (double-digit growth since inception), and is a highly expandable model with 20x more growth potential alone in Jacksonville as there is only 5% current market penetration of the gyms and wellness centers in the city.

With GRIL’s $10 million, investors might expect another acquisition to take place in the convenient fitness and healthy food space. Again, according to the corporate update, the Superfit Foods acquisition fits into GRIL’s business model perfectly:

“Fitness and wellness takes many forms but combining healthy eating with an active lifestyle produces the best results. Getting healthy doesn't work if you are only working out or only eating healthy. Yes, there are benefits from doing only one part of the overall process but combining an active lifestyle with healthy eating is a strong combination to produce results. Gyms struggle to keep consumers active with memberships, they experience a lot of turnover. Trainers experience the same thing. Our belief is that this is a direct result of people not seeing immediate results. Combining healthy eating with an active lifestyle typically produces sustainable and measurable results. By partnering with gyms, trainers, wellness and lifestyle centers, it's a win-win-win scenario. Consumers see results, gyms/trainers retain clients and Superfit Foods continues to grow at a rapid pace via new subscribers. Combine that with convenience and we believe we have a unique approach to this market.”

With a deal obviously cooking, investors are going to keep their eyes peeled for GRIL’s next press release.

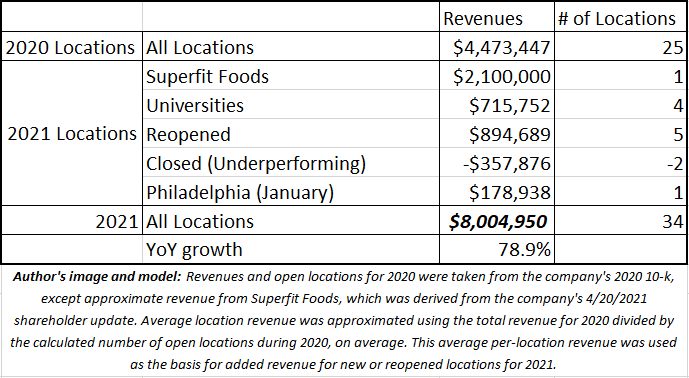

Modeling Revenues in 2021

What most investors don’t realize is that GRIL’s revenues are set to skyrocket this year. The company, compared with 2020, reopened 5 locations that were closed due to COVID-19 in 2020, closed two underperforming locations, has 4 university locations ready for when students come back, and opened a site in Philadelphia in early 2021. Investors should also expect more military base locations to open up throughout 2021.

What this calculation of about ~80% revenue growth doesn’t take into account are changes (likely growth) in existing locations, pending acquisitions, and any additional locations (traditional restaurants and ghost kitchens) opening up. The projection is quite conservative. Also, there is likely to be overall per-location revenue growth due to the brand expansions that have taken place over the last few months. This is just a base-case scenario based on existing run rates for other locations. Lastly, there are franchise fees/royalties to be paid to GRIL that were partially put on hold during the pandemic to help franchisees weather the storm.

Valuation and Financials

As of April 15th, there were 13,826,734 shares outstanding, and 23,664,508 shares fully diluted. However, the average exercise price for those warrants and options are significantly above the current market price. Prior to the PIPE, there were warrants to purchase an aggregate of 2,582,857 and 2,450,287 shares of common stock with weighted average exercise prices of $4.08 and $5.51 per share, respectively. Then, the PIPE introduced warrants at $2.43.

Thus, if the share price goes up, the company will already have funding potential at favorable prices, especially since another $10 million will be available at $2.43. According to the latest 10-K, the company had $4.2 million in cash. Assuming about $4 million was used between the end of the year and now for operations and the acquisition of Superfit Foods, there is currently about $10 million in cash just from the PIPE, and another potential $10 million. For such a fast-growing company with cash in its coffers, the current enterprise value of the company is just ~$14 million. This means that this fast-growing company is only trading at ~1.75 EV/sales.

One could use the fully diluted share count, but they would need to include the additional $10 million in proceeds from the recent PIPE and $24 million in proceeds from warrant exercises (see the 10-k)—essentially $34 million more in cash.

GRIL is trading barely over its current cash value, and with the economy opening back up, its rapid business expansion, and the stock trading well below the recent PIPE price, it is extremely inexpensive. While the company does continue to be cash flow negative, this is the nature of quickly scaling the business. Investors should also note the company’s ability to raise money at market prices.

NYU Stern cites an EV/TTM sales multiple of 5.27x for the restaurant/dining business, and QSR competitors MacDonald’s and Chipotle trade at about 11x and 6x right now, respectively. Starbucks (SBUX) and QSR brands (QSR), which includes KFC and Pizza Hut, also trade at about 6-7x EV/TTM sales. Using a conservative EV/TTM sales multiple even though GRIL is likely to continue growing faster than these companies (given its smaller size), we can put a 5x EV sales multiple on GRIL for and we arrive at a stock price of ~$3, using 13.8 million shares. Thus, over the next year, we would expect GRIL to appreciate to ~$3, which is almost 100% above the current price.

Investor Summary

A perfect storm for growth is brewing in the restaurant sector and GRIL is one of the best-positioned microcap names to profit from it. The market cap is hovering around $22.5 million not including the shares from the last acquisition which means that roughly half of the company or $10 million of that is in cash. The microcap markets appear to be bottoming. The investors that incorrectly sold the stock off after the offering have completely derisked this name. The next acquisition should be explosive for the stock price. This management team is very savvy and Michael Roper who grew the tex-mex chain Taco Bueno is leading the charge with a paradigm-changing strategy. This is a great growth story in the making due to the market's recent reaction to the fundraising. Growth should be exceptional this year even as they continue to focus on profitability.

Disclosure: I do not have a position in this company but may take a position in the coming months.