Microsoft Dividend: 11% Increase For This Dividend Growth Stock

There are generally two different groups of income investors. One group focuses on receiving high levels of current income. This is done by investing in stocks with high dividend yields. The downside of high-yield stocks is that they often have low dividend growth over the years or no dividend growth at all.

In the other camp are dividend growth investors who are willing to sacrifice some income today, for the prospect of even more income down the road. Dividend growth investors focus less on current dividend yields and focus more on stocks that can increase their dividends at a high rate each year.

Tech giant Microsoft Corporation (MSFT) falls into the second camp. Microsoft recently increased its dividend by 11%, raising the forward yield to 1.5%.

Microsoft’s 1.5% forward yield is still a fairly low yield and falls below the average yield of the S&P 500 Index. But if Microsoft can continue to increase its dividend at such a high rate, investors will see their yield on cost rise dramatically over time.

Microsoft stock does not have a high dividend yield right now, and it could be argued the stock is overvalued. But from a dividend growth perspective, Microsoft is tough to beat. This article will discuss Microsoft and its recent dividend increase.

Business Overview

Microsoft develops, manufactures and sells both software and hardware to businesses and consumers. Its offerings include operating systems, business software, software development tools, video games and gaming hardware, and cloud services. Products and services are delivered under various brand names including Office, Windows, Surface, Xbox, Azure, Dynamics, Bing, and more. Microsoft also owns LinkedIn, which was acquired for $26.2 billion in 2016.

Many businesses would not be able to function properly without the use of Microsoft products like Word, Excel, and Outlook. Further, many homes would lose much of their functionality (in terms of communication, eCommerce, etc.) without the personal computing capabilities provided by the Windows operating system.

Microsoft’s market capitalization is now over $1 trillion, and the company generated over $125 billion of revenue in the most recent fiscal year. On July 18th, Microsoft reported quarterly and full-year results for fiscal 2019. For the fourth fiscal quarter, the company generated revenue of $33.7 billion. This beat analyst estimates and increased 12% from the same quarter the previous fiscal year.

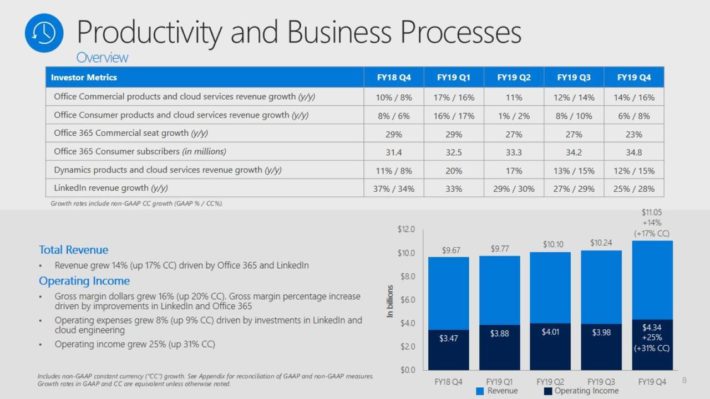

Growth was spread across Microsoft’s business segments. Productivity and Business Processes, Intelligent Cloud and Personal Computing making up 32.8%, 33.8% and 33.5% of revenue, and each grew 14%, 19%, and 4% respectively.

(Click on image to enlarge)

Source: Investor Presentation

Adjusted net income came in at $10.6 billion, a 24% year-over-year increase, while earnings-per-share also increased 24% for the quarter.

For the fiscal year, Microsoft reported revenue of $125.8 billion, up 14% from fiscal 2018. The company also reported operating income of $43 billion (up 23%), and adjusted earnings-per-share of $4.75 (up 22%).

Overall, it was a tremendous year for Microsoft. And, due to the company’s investments in a massive growth industry, its revenue and EPS growth should continue over the next several years.

Growth Prospects

It wasn’t too long ago that investors widely shunned Microsoft for its weak growth prospects. In the years immediately following the 2008-2009, Microsoft struggled to grow earnings as its revenue growth slowed. Microsoft struggled to produce high growth as its reliance on the personal computer weighed on the company. It was widely theorized that Microsoft could not compete in a technology industry increasingly moving away from PCs, which were losing relevance to smartphones and tablets.

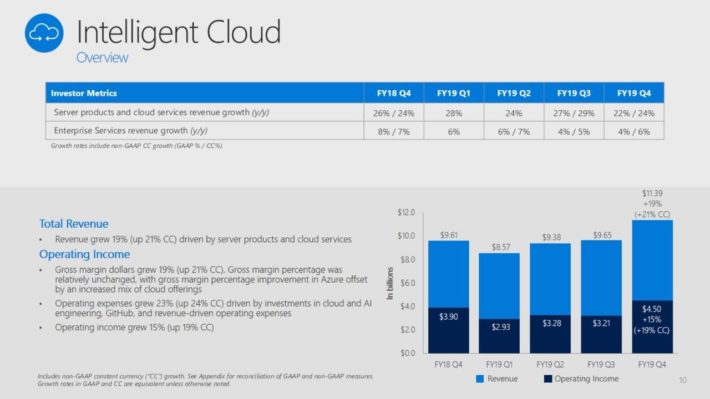

But what a difference a few years makes. Microsoft has successfully turned its business around, with a much greater reliance on software, particularly in the cloud. Azure, Microsoft’s high-growth cloud platform, grew by 64% last quarter, showcasing Microsoft’s strong position in this high-growth market. Azure resulted in Microsoft’s Intelligent Cloud business leading its growth last quarter.

(Click on image to enlarge)

Source: Investor Presentation

Microsoft’s resurgence, led by CEO Satya Nadella, has been nothing short of remarkable. Microsoft’s cloud business is growing at a ~20% pace thanks to Azure, which combines IaaS, PaaS & SaaS offerings and which had been growing at a 70%+ rate for 12 quarters in a row. Microsoft’s Office product range, which has been a low-growth cash cow for many years, is showing strong growth rates as well after Microsoft has changed its business model towards the Office 365 software-as-a-service (SaaS) system.

Due to low variable costs, the impact of operating leverage will allow Microsoft to maintain an earnings growth rate that is higher than the revenue growth rate for the foreseeable future. Buybacks are an additional factor for Microsoft’s earnings-per-share growth, although this form of capital allocation becomes less attractive with an elevated valuation.

The markets Microsoft addresses continue to grow, with cloud computing being the most compelling one of these markets. This means that even without any market share gains Microsoft will most likely be able to grow its top line. Thanks to rising margins and a declining share count Microsoft’s growth outlook over the coming years looks quite compelling, although not quite as robust as the company’s last couple of years.

In all, we expect 8% annualized EPS growth from Microsoft over the next five years. This could prove to be an overly conservative estimate, as the company is growing revenue at a high rate. Margins should remain stable, and the company’s huge share buyback should only boost EPS growth going forward.

To that end, Microsoft recently authorized a massive new $40 billion share repurchase along with its recent dividend increase. The current repurchase represents about 4% of the company’s current market capitalization, which means all else being equal, Microsoft’s new buyback could grow EPS by 4%. Between buybacks and dividends, Microsoft has a strong total shareholder yield. Of course, Microsoft’s dividend remains a key component of the company’s capital allocation strategy.

Microsoft Dividend Analysis

Microsoft has an excellent history of dividend growth. The company has increased its dividend for over 10 years in a row, qualifying the stock as a Dividend Achiever. And while some companies give shareholders small dividend increases just to remain on lists like the Dividend Achievers, Microsoft is a strong dividend growth stock. Including the most recent 11% raise, Microsoft has increased its dividend by a compound annual rate of 15% per year over the past 10 years.

Such a high dividend growth rate can really add up for shareholders over time. For example, if Microsoft continued to increase its annual dividend by 15% per year, in 10 years from now the quarterly dividend would reach $2.06 per share, or approximately $8.24 per share on an annual basis. For investors buying at the current share price of ~$139, this would mean a yield on cost of nearly 6% in a decade.

And investors should keep in mind, this calculation does not assume reinvestment of dividends over the given time period, which would elevate the yield on cost even further.

For dividend growth stocks like Microsoft, the yield on cost can actually surpass that of stocks with much higher current dividend yields. To emphasize this point, consider a stock that has a 5% dividend yield today, but only increases its dividend by 2% per year.

This is the typical dividend yield and growth profile that an investor might see from a utility or a telecom stock. But in this scenario, the high-yield stock would have a yield on cost of 6.1% in 10 years—just barely higher than Microsoft’s yield on cost. And after that 10-year period, Microsoft’s yield on cost will far surpass the high-yielding stock.

It is worth mentioning that investors who reinvest dividends will still have a higher yield on cost from the 5% yielding stock, although many income investors buy dividend stocks to use the income and do not reinvest payouts.

This demonstrates the power of compounding over time. While Microsoft’s current dividend is less than 2% and may not entice income investors, those with at least a moderate time horizon can reap huge benefits by investing in high-quality dividend growth stocks.

Microsoft’s chances of replicating its high dividend growth rate moving forward are quite good. First, it has a dominant position in its industry and tremendous competitive advantages through its research and development, brand, and financial resources. During fiscal years 2018, 2017, and 2016, research and development expense was $14.7 billion, $13.0 billion, and $12.0 billion, respectively. These amounts represented 13% of revenue those fiscal years.

This has resulted in a very wide economic moat, a term popularized by legendary investor Warren Buffett to describe a company’s impenetrable business model. Microsoft has a great moat in the operating system & Office business units and a strong market position in cloud computing, an emerging business segment with a long runway of growth up ahead.

Next, Microsoft is a highly profitable company with strong EPS growth. As a result, the company has a low payout ratio which leaves room for high dividend raises each year. The dividend payout ratio has never risen substantially above 50%, and the fact that Microsoft owns one of the strongest balance sheets in the world means that the dividend is very safe.

Microsoft has an expected dividend payout ratio of 39% for the upcoming fiscal year. This is a healthy payout ratio which leaves plenty of room for continued dividend increases. Plus, since the company is expected to continue growing EPS, annual dividend increases of at least 10% are certainly not out of the question for Microsoft.

In fact, Microsoft is one of only two U.S. companies to hold the coveted AAA credit rating from Standard & Poor’s—the other company being healthcare giant Johnson & Johnson (JNJ). Microsoft’s AAA-rated balance sheet makes it a low-risk business by providing the company with a much lower cost of capital.

As of the most recent quarterly report, Microsoft held $133.8 billion in cash and securities, $175.6 billion in current assets and $286.6 billion in total assets against $69.4 billion in current liabilities and $184.2 billion in total liabilities.

Potential Risk Factors

The only possible negatives to be said about Microsoft stock would be its valuation and its vulnerability to recessions. Microsoft stock has rallied tremendously in recent years. It has trounced the broader market over the past 10 years, with a total annual return of 21.5% compared with 13.1% for the SPDR S&P 500 ETF (SPY).

The downside of such a huge rise in share price is that the stock is much less attractive today. Based on expected EPS of $5.00 for the upcoming fiscal year, Microsoft stock trades for a price-to-earnings ratio of nearly 28. This is in stark contrast to Microsoft’s historical valuation multiples. For example, in the past 10 years, the stock traded for a P/E ratio of 16.

Microsoft’s valuation bottomed out in 2011 with a P/E ratio slightly under 10. By these standards, today’s valuation seems very high, even with Microsoft’s impressive EPS growth. Our fair value estimate is a P/E ratio of 22, which would imply significant downside from the present level.

Therefore, from the perspective of total returns, Microsoft gets a hold recommendation from Sure Dividend. The following video further details our hold rating on Microsoft stock:

Video Length: 00:12:01

Valuation is unrelated to a company’s dividend growth potential. For this reason, even though Microsoft stock is too aggressively valued to earn a buy recommendation from Sure Dividend today, it is still a compelling stock from the perspective of long-term dividend growth.

That said, one factor that could derail Microsoft’s future dividend growth is a recession. The other potential negative of Microsoft stock is that the company is not highly resistant to recessions. Technology is a cyclical industry, and one that typically suffers during economic downturns. Software and services companies like Microsoft are likely to see reduced demand when the economy goes into recession.

Despite these risks, Microsoft remains a compelling stock for long-term dividend growth investors. Those with a very short investing time horizon are likely to stock to high income stocks, but investors looking out 10 years or more should also consider high-growth dividend stocks. Dividend growth stocks like Microsoft have the potential to offer greater income over the long-term than stocks with the highest dividend yields right now.

Final Thoughts

Microsoft is a cash cow. The company is highly profitable and generates billions of free cash flow each year. The cash has piled up on the balance sheet, which gives the company a rare AAA credit rating. And, thanks to Microsoft’s turnaround and exposure to emerging segments such as the cloud, the company is generating high revenue and earnings growth.

Add it all up, and investors can expect Microsoft’s high dividend growth rates to continue for the foreseeable future. Double-digit dividend increases each year are realistic and attainable, provided the global economy stays out of a deep and lengthy recession. Microsoft’s high valuation prevents it from receiving a buy recommendation from Sure Dividend at this time, but for investors primarily concerned with long-term income generation are likely to be impressed with Microsoft’s dividend.

Disclaimer: Sure Dividend is published as an information service. It includes opinions as to buying, selling and holding various stocks and other securities. However, the publishers of Sure ...

more