Market Briefing For Monday, May 6

A serious dilemma facing money managers as they contend with rather evident S&P resilience entering the old adage of 'sell in May and go away' seasonal vulnerability (mostly due to a paucity of fresh funds coming into a market; after that's already 'typically' occurred), is a valid question: why is 2019 different? (It's emerging from a prior year of 'pretend prosperity' and is the tail-end of recessionary conditions; and ahead of an Election year.)

After all; statistics validate a point I've brought up periodically this year; that large funds (and even seemingly large investors) have been selling all year thru an historic rally, which is still in the all-time high vicinity for the S&P. So many missed the move; thus you have conventional interpretations of 'why' (being a recession coming) of course, and then 'what to do' about it.

Some have capitulated and chased stocks around recent highs; while other players have simply retained their staunch (superficial) skepticism; praying for stocks to retreat. I call them the 'Bull-Bears', and a large contributor to a sort of underlying 'bid' to the market; as skepticism actually prevails more it seems than 'euphoria'. They 'say' it's euphoria (and sort of is in IPO's or at least the FOMO approach for monetizing start-up's ... fear of missing out in case the market rolls-over); versus FOMO for the big stock managers; who are resigned to a poor performance year if they 'don't get a big shakeout'.

So the irony is the small company underwriters are trying to get money out of earlier investments because they fear a decline; and the big managers, to the contrary; are praying for decline so they can enter at better valuation levels. This is a different bifurcation than commonly seen; and 'Bull-Bears'are a type of manager/analyst coming out of hibernation that's amusing for those of us who caught the drop last year and 'V-bottom' turnaround.

All this matters, as I've tried to outline, not because we were right about the market soaring 'if Trump won'; but more importantly how the then-projected 'rolling bear market' (rinse & repeat corrections of 2018) set-up what we're in in 2019. This matters not to pat ourselves on the back (though I do seem to on rare occasion haha); but because a primary reason is to contemplate whether this is 'stretching' the old cycle as most contend, or 'really the start of a new cycle', from December-forward, as I have contended.

Now of course that won't prevent normal pauses-to-refresh or corrections, along the way; provided serious failures (like China talks breaking-down), don't derail prospects and tank the stock market big time (it's a risk but not a probability given how long both sides have been sparring to cut a deal).

What it does suggest (and I have constantly reiterated) is that all the pundit forecasts of the 'worst bear market ever' and 'recession coming' are totally off the mark; because the nuances of recession began over a year ago and (although most analysts and economists deny that to be the case even as a slew of charts and even Fed tracking data supported our view) as you're well aware, I have suggested would end about the time it's proclaimed, if at all. They are surprised we're not in recession now; they ignore we had one and it's basically being emerged from.

That's the heart of my argument as to why last year was so important both for selling early into rallies, and then buying the near-year-end liquidation; a climactic selling wave as I called it. If correct (again barring fundamentals going off a cliff or an Oil collapse) this remains a technology transition year, and all that we can envision is a 'correction' or partial retracement of rallies from December to the area of present highs; or higher if we spike on China deals (perhaps as soon as the next week or so).

In sum: the primary trend is up; with the cycle commencing last December not some time in the future. China trade agreements are key to vibrancy orat least very near-term resilience. Conversely disruptions with China could accelerate a shakeout that is due anyway in some form.

The point is: the corrections should be within-context of the upward cycle I identified from December's projected washout and turn-up; and while easy to view the secular trend as old; the cyclical trend is not an extension; but a new bullish cycle identified to start in December.

Many small stocks thrust a bit at 2019's start, then corrected; and actually are more stable at this time than they were over the last two months. Many FANG-types are shakier; with the recent plunge (not recovered much) by Alphabet / Google pretty much denoting significant air-pockets than can quickly unwind the bloated 'grand dames' of this era; and is foreboding for the near-term in terms of hindering enthusiasm for the overpriced sectors.

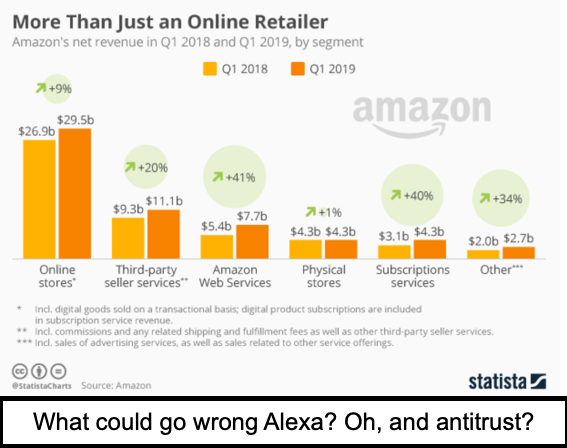

Bottom-line: valuations are stretched for big-caps generally; not for others but generally a seasonal prospect for corrections, aside spikes related to a China Deal, lead us into a rangebound at-best, or correcting phase for the majority (especially those that haven't dipped much this year). Some offset is provided by the already-corrected but they can't really offset any big dip in the FANG types, if that does arrive. Buffett going into Amazon buys time; it doesn't change the bloated nature of that stock or the sector.

Firms are using debt and buybacks both for acquisitions and preserving at least a modicum of stability. This has been going on for some time. In fact, I believe one reason the market has absorbed the general selling by those who were too bearish and ill-informed (not just the permabears trying hard to entice investors into lousy investments based on fear-mongering they've not modified for years in many cases) has to do with those buybacks.

And one more thing: demographics have (us?) baby-boomers compelled to gradually withdraw from markets (at least our mandatory retirement funds that are tax-deferred, not tax-exempt). That probably accounts a lot for the statistical anomaly of a strong S&P with underlying liquidation all year long (maybe more so than Norway or other sovereign-wealth-fund buying).

If 'new money', foreign money, or buybacks combine to absorb well-known demographic trends certain pundits have suggested would cream markets for years; well fine. Then bearish from January of 2018 because we'd spiked in a sort of blow-off ('then, not now'); and then eventually bullish as we capitulated into an anticipated liquidation selling-climax in December.

So; discretion remains the better part of valor; while a correction (based on what is known now; not outcomes of known unknowns) appears likely to be within the 'context of an overall uptrend dating from December's low.