Longer-Term Multiples Remain Similar To Mid-February

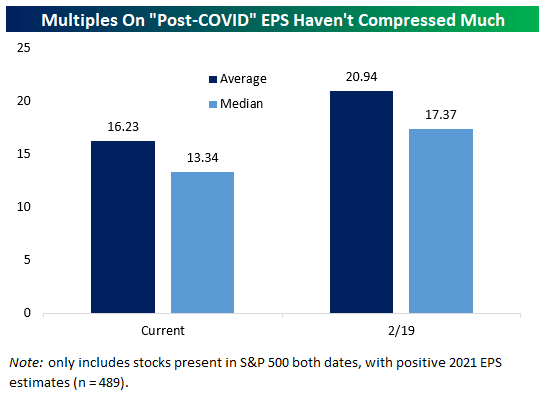

Markets understand pretty well just how badly earnings are going to be hit in 2020, and we’ll start to get a more specific view of that with earnings reports that start next week. There’s a good argument to be made that longer-term earnings should be the touchstone for equity valuation, looking past the near-term COVID shock to EPS. With that in mind, how cheap are stocks getting relative to estimated earnings in the longer-term? As shown in the chart below, not very much. Multiples on calendar 2021 EPS estimates were 20.9x on average in February, versus 16.2x today. That’s certainly a notable compression, but it’s not anything we would call dramatic. On a median basis, the compression has been from 17.4x to 13.3x, again nothing overly dramatic. There’s a compelling case to be made for US stocks given the recent peaking of European new case counts and flattening of US case counts in major outbreak states, of course. But valuation doesn’t seem to be as compelling as a justification for owning the market here.

(Click on image to enlarge)

Start a two-week free trial to one of Bespoke’s three premium memberships to see our best and most actionable ...

more