Is This 14.7% Yield In A Death Spiral?

I constantly receive requests to analyze the dividend safety of StoneMor Partners (NYSE: STON).

It’s not hard to see why it’s an investor favorite. It has a 14.7% yield and is in a recession–proof business.

StoneMor operates 316 cemeteries and 100 funeral homes in 27 states and Puerto Rico.

It pays a $0.33 quarterly dividend, or $1.32 per year. Based on the stock price, that comes out to a huge 14.7% yield.

A yield that large is attractive – but only if it’s safe.

StoneMor’s isn’t. And when SafetyNet Pro crunched the numbers, it came to the same conclusion.

StoneMor Partners is a master limited partnership (MLP). As an MLP, its dividends are called distributions.

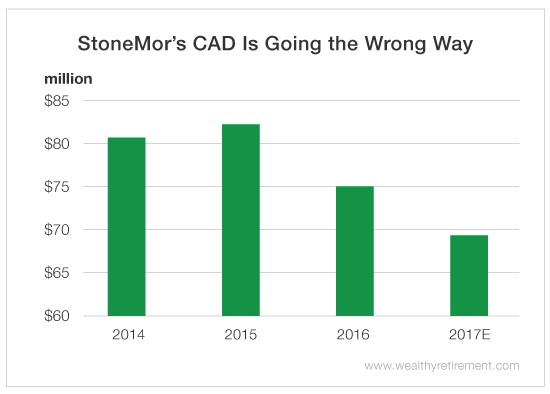

And a key metric for MLPs is cash available for distribution (CAD). It is essentially cash flow and represents all of the cash the company made and could distribute if it wanted to.

StoneMor’s CAD fell last year and is expected to do so again in 2017.

Obviously, you want to see cash flow or CAD growing, not declining.

This is a critical problem for StoneMor… Last year, the company didn’t generate enough cash to afford the dividend it paid to investors. And if the forecasts are right, that will happen again in 2017.

In 2016, StoneMor Partners paid out $2.5 million more in distributions than it generated in cash. This year, it is projected to pay out $70 million in distributions but generate $69.3 million in CAD.

As I pointed out in November, StoneMor has a lot of debt. And if CAD can’t even afford the distribution, paying down that debt is going to be difficult.

How much cash does the company have to pay the distribution and debt?

It’s anyone’s guess.

After years of speculation that its accounting was “aggressive,” to put it generously, StoneMor restated financial statements from 2013 through the first two quarters of 2016.

Then in March, the company said that it was unable to file its 2016 10-K on time. The 10-K is the annual report a company files with the SEC. It also has not yet reported first quarter 2017 numbers.

As a result, we have no idea how much cash it has or if previously reported CAD numbers are accurate.

The last figures were reported in the third quarter of 2016, when the company claimed to have $15 million in cash – but again, we don’t know whether that is correct.

Lastly, management cut its dividend in half in October, from $0.66 to $0.33. Its rationale? It was “working to regrow its sales force.”

While the company has not reported financial information, in April, it did say it added 17 more sales people than there were during the same time last year (though it lost 17 sales people in February).

The final nail in the coffin is only 671 out of 746 sales people made a sale in March. That compares to 692 out of 729 in March 2016.

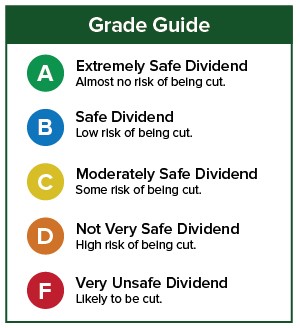

With declining cash flow, a recent dividend cut, and management that, at best, has no idea what it’s doing and, at worst, is hiding something… StoneMor’s dividend is extremely unsafe.

Dividend Safety Rating: F

Disclaimer: Nothing published by Wealthy Retirement should be considered ...

more