Is Facebook Worth Its Current Price?

All assets are worth the present value of their future cash flows. Even if you haven’t been to business school and heard this financial theory, you probably have some intuitive sense that if you buy a piece of real estate as an investment, you know that the income that property produces relative to the price you’re paying for it is important.

The problem with a “discounted cash flow” approach (forecasting future cash flows and applying a discount rate to them to arrive at a present value) is that people rarely know what future cash flows will be, and nobody knows how to discount them properly to arrive at a present value. Regarding discounting, Warren Buffett likes to apply the rate on the 30-year U.S. Treasury. Others like to apply a discount rate as a “hurdle rate” that reflects the return they’d like the investment to deliver – say, 10%. As Buffett’s sidekick, Charlie Munger, says, valuing an asset isn’t supposed to be easy. And that makes sense since skill at valuation is lucrative.

But instead of estimating cash flows and applying a discount rate to see what an asset is worth, sometimes it can be useful to understand what future cash flows the market is anticipating by awarding a stock its current price. When you back into, or reverse engineer, the future cash flow assumptions the market is making, you can sometimes decide if Mr. Market is off his meds or not.

(Discounting a cash flow is the opposite of compounding it the way you might do a compounded interest calculation. It involves dividing the cash flow by your chosen interest rate for each year in the future the cash flow occurs. So an assumed $100 payment next year discounted at 10% is worth $90 today. An assumed $100 payment in five years is worth $62 today, or $100/(1.1^5).)

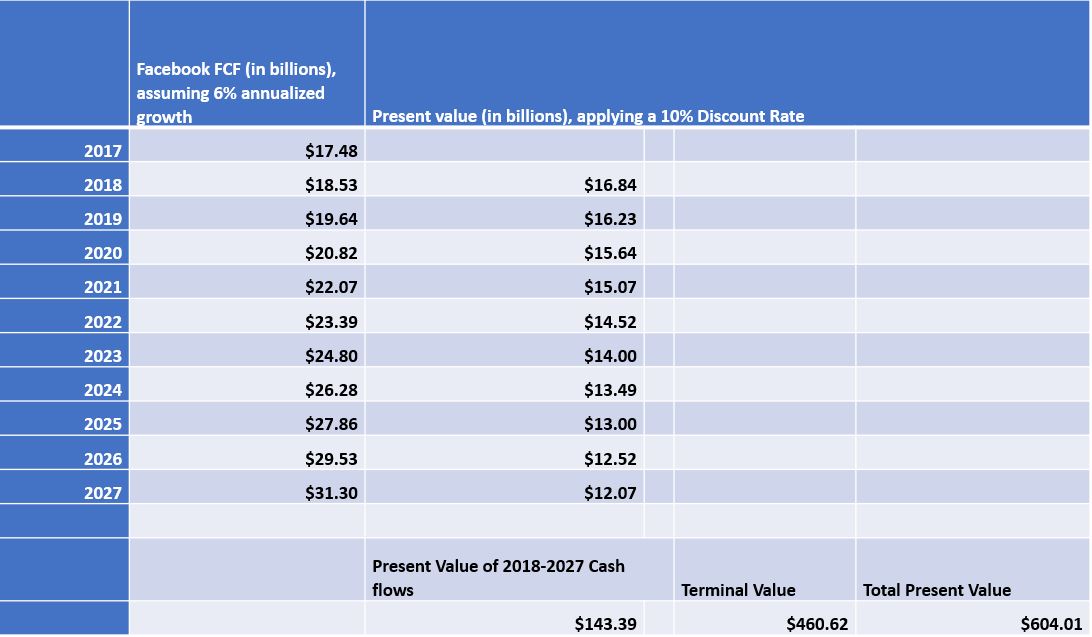

So what future cash flows is the current ~$600 billion market capitalization of Facebook anticipating, and are those future cash flows achievable? Let’s try to find out.

From 2013 through 2017, Facebook’s revenue has grown remarkably from under $8 billion to more than $40 billion. Also, free cash flow, as Morningstar calculates it has gone from under $3 billion to nearly $17.5 billion over the same time. That’s around a 55% compounded annualized growth rate.

It turns out that if Facebook can grow its free cash flow by 6% annually for the next decade, and then we assume its return on invested capital equals its cost of capital after that (meaning it loses it competitive advantage), we arrive at a present value roughly equal to its current $600 billion market capitalization, using a 10% discount rate.

(Click on image to enlarge)

Facebook has converted $0.40 of every $1.00 in revenue into free cash flow over the past few years. Assuming that prodigious profitability continues, Facebook would have to increase its revenues by more than 12% annually for the next decade to justify the current stock price. Its 5-year revenue growth rate, according to Morningstar is 20%. A drop-off is inevitable, but it’s difficult to know how much of a drop-off to expect. How mature is Facebook? That’s a big question for an analyst.

To put that revenue growth in perspective, compounding its current $40 billion revenue by 12% annually (not quite enough to get to 6% FCF growth at the current 40% conversion rate of revenue to FCF) would result in more than $120 billion in revenue in 2027. That’s more than Google’s $110 billion in revenue and a little more than half of Apple’s $229 billion in revenue. Can Facebook achieve that revenue growth? That’s another tough question for an analyst.

Facebook’s business model is an advertising one, and I haven’t said anything about the online advertising market. An analyst would have to know how big it is, how much of it Google owns, or whether Facebooks can, or needs to, capture some of Google’s share to justify its current price. At first blush though, growing revenue by 12% or more for the next decade seems like a tall order. Since I don’t know the online advertising market, I can’t say it’s impossible though. Also, one needs to make a judgment about whether Facebook will suffer from competition. Will another platform make inroads into Facebook’s business, or does it benefit from a kind of network effect whereby enough people are already on Facebook that others have to join to be involved in social media?

But this is the type of analysis you have to do if you’re going to invest in a stock – and it’s not even the bare minimum since I haven’t looked at the online advertising market. Buying shares of Facebook because your friends and neighbors own it or because you just think “it’s going up” isn’t really an investment rationale.

At least this analysis shows what kind of revenue and free cash flow growth the market is pricing in. We could have done a sensitivity analysis, adjusting discount rates and the growth trajectory instead of just assuming an even 6% free cash flow growth every year. Still, this simple step gives us some idea of what the market is forecasting for Facebook. I wouldn’t short Facebook, but you have to be optimistic to invest at this price.

John, thank you for this indepth look into FB. My primary concern with FB is its user metrics. According to recent numbers, FB's user growth has slowed significantly. This is a major sign of weakness going forward. I suspect this is the result of an accumulation of the more recent events that FB had to deal with. I'm also not impressed with FB's management decisions on content handling.

While I believe $FB is overvalued, you answered your own question when you wrote:

"Will another platform make inroads into Facebook’s business, or does it benefit from a kind of network effect whereby enough people are already on Facebook that others have to join to be involved in social media?"

Facebook it too big to worry about competition from a new competitor. A social site only works because everyone you know is already on it. The only real contender would have been Google which already tried and failed with Google Plus. If they couldn't make even a dent in Facebook, why would any other company be able to.