IBM Reports First Revenue Growth Since 2018; But Closer Look Reveals Usual Accounting Gimmicks

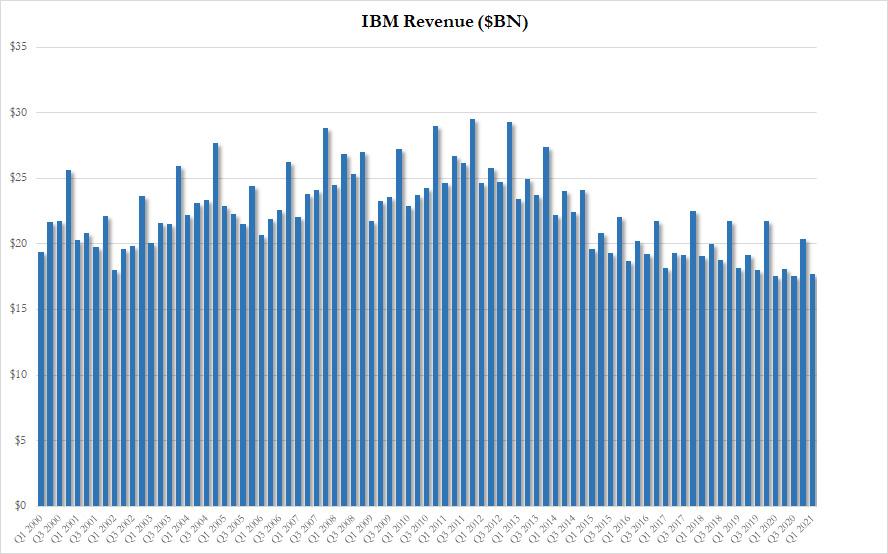

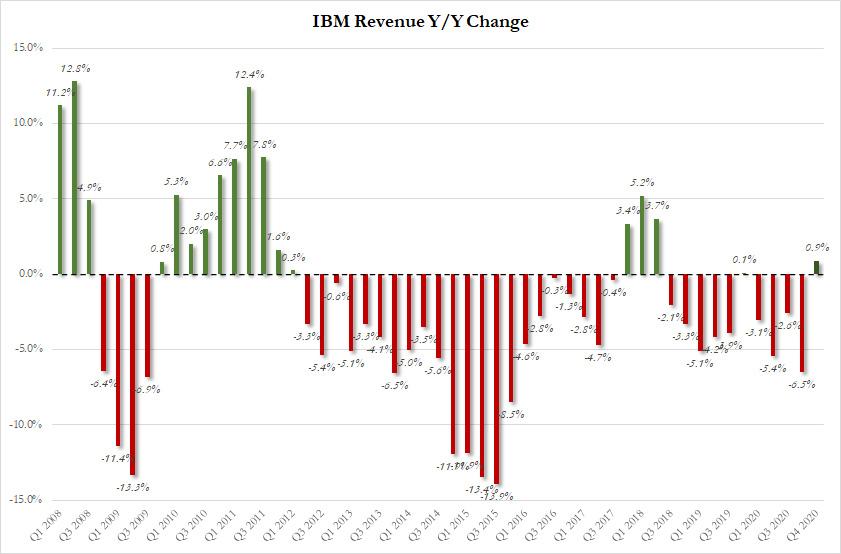

There was some hope last year that IBM was finally turning things around: after all, after 5 consecutive quarters of declining revenues, the company had just managed to grow its top-line for the first time since Q2 2018 - when revenue grew by a paltry 0.1% - and only for the 4th time in the past 8 years. Alas, those hopes were dashed for much of the pandemic plauged 2020 when the company reported three consecutive quarters of declining revenue.

However, in a glimmer of hope for Big Blue, moments ago IBM reported that in Q1 it generated revenue of $17.7320BN, which smashed expectations of a $17.32BN (which would have been the lowest quarterly revenue for the 21st century) and came above the highest analyst estimate for the quarter of $17.54BN.

More importantly, while modest, the Q1 revenue was actually a 0.9% increase compared to Q1 of last year, which made it the first revenue increase in 11 quarters, since 2018.

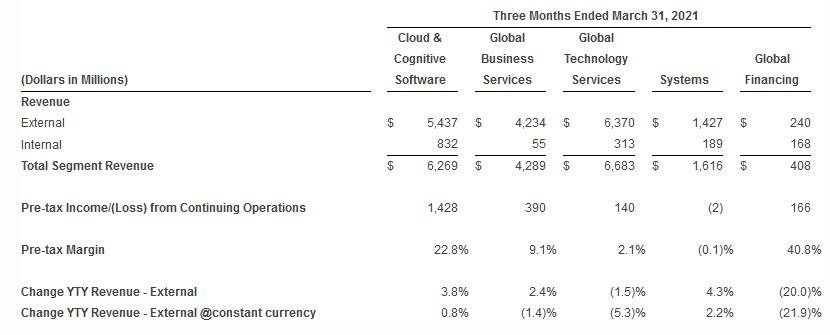

The top-line strength came on the back of solid performance by virtually all groups (only Global Financing revenue missed expectations), with total Cloud revenue of $6.5BN up 21%. IBM also reported Q1 revenue growth in three of its five business segments, including Cloud and Cognitive Software, the company’s biggest unit, which saw 3.8% growth in sales from a year earlier. The Global Business Services and Systems units, which includes hardware and operating systems software, also posted year-over-year sales increases of 2.4% and 4.3%, respectively.

- Cloud and cognitive software revenue $5.44 billion, beating estimates of $5.39 billion

- Global business services revenue $4.23 billion, beating estimates of $4.08 billion

- Global technology services revenue $6.37 billion, beating estimates of $6.23 billion

- Systems revenue $1.43 billion, beating estimates of $1.25 billion

- Global Financing revenue $240 million, missing the estimate $297.8 million

IBM also said revenue from Red Hat, which it bought in 2019 for $34 billion, gained 17% in the first quarter.

The breakdown visually:

IBM also reported that cloud revenue over the last 12months was $26.3 billion, up 19% which while high still lags badly similar offerings from Amazon and Microsoft.

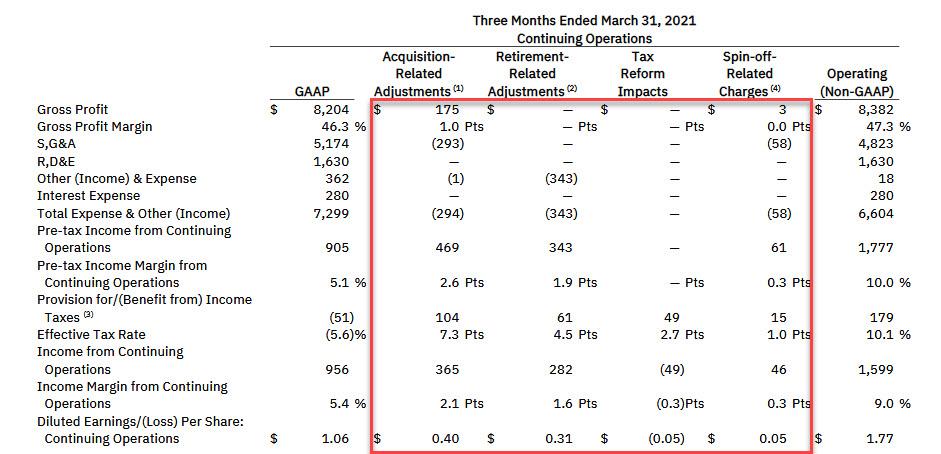

The top-line beat also translated into a beat on the bottom line with IBM reporting adjusted EPS of $1.77, just above the estimate of $1.65, and still down 4% Y/Y. And here is the actual "beat" in context.

There was more good news with the adjusted gross margin also coming in at 47.3%, or just above the 47.2% consensus estimate.

That was the good news.

As for the not-so-good news, there was plenty starting with the observations that IBM's accounting gimmicks were back front and center, starting with the company's effective tax rate, which in Q1 was a negative -5.6%! As a result, Net Income of $955MM was higher than pretax Net Income of $905MM. It was also down 19% from a year ago.

Elsewhere, it has long been known that only Watson can calculate IBM's "one-time non-recurring" charges, which are neither one-time non-recurring, which meant that the adjusted EPS of $1.77 was actually GAAP EPS of $1.06, a 19% drop Y/Y (even assuming the -5.6% tax rate was credible).

But wait there's more because the GAAP to the non-GAAP bridge was, as usual, ridiculous and a continuation of a "one-time, non-recurring" add-back trend that started so many years ago we can't even remember when, but one thing is certain: none of IBM's multiple-time, recurring charges are either one-time or non-recurring.

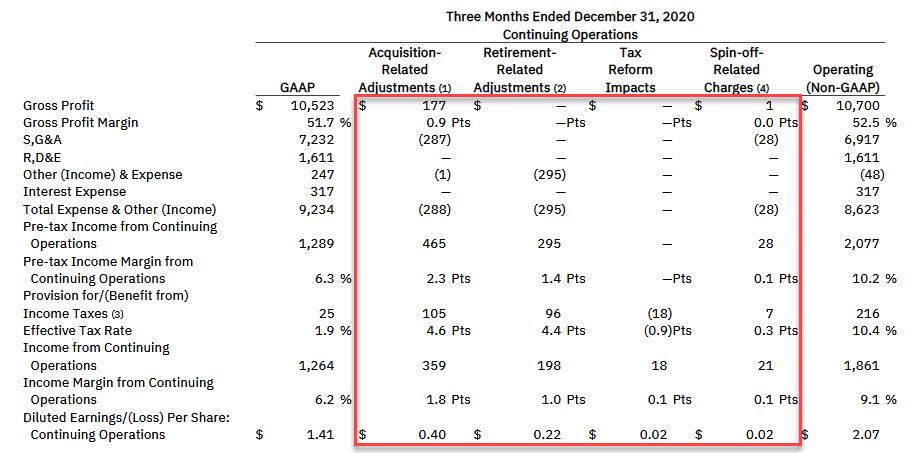

We have said it before, but we'll say it again: here is IBM's "one-time, non-recurring" items In Q4...

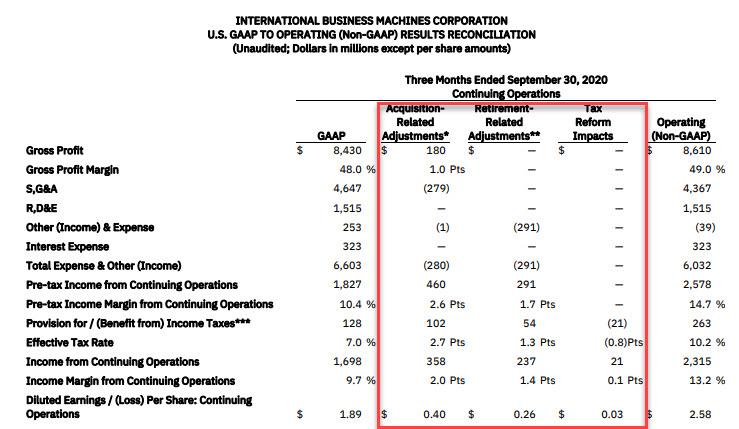

... and in Q3 ...

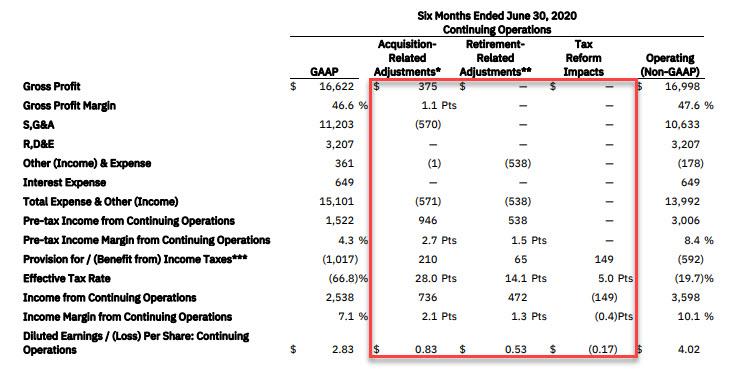

... and in Q2 ...

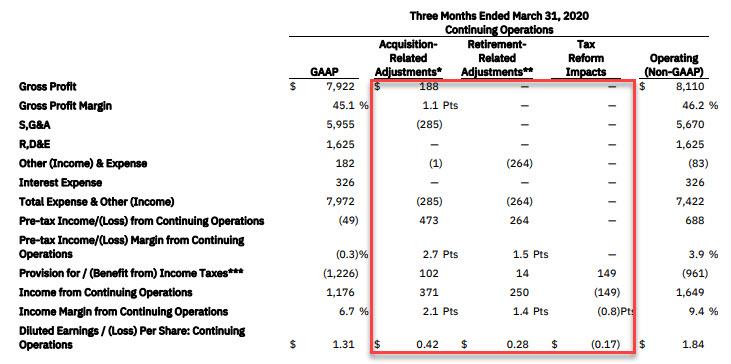

... and Q1 2020...

Commenting on the quarter, Chairman and CEO Arvind Krishna noted "strong performance this quarter in the cloud, driven by increasing client adoption of our hybrid cloud platform, and growth in software and consulting enabled us to get off to a solid start for the year” He added that “while we have more work to do, we are confident we can achieve full-year revenue growth and meet our adjusted free cash flow target in 2021.”

Maybe... although like in the past four quarters, IBM did not have enough "visibility" into the future to give any guidance for 2021.

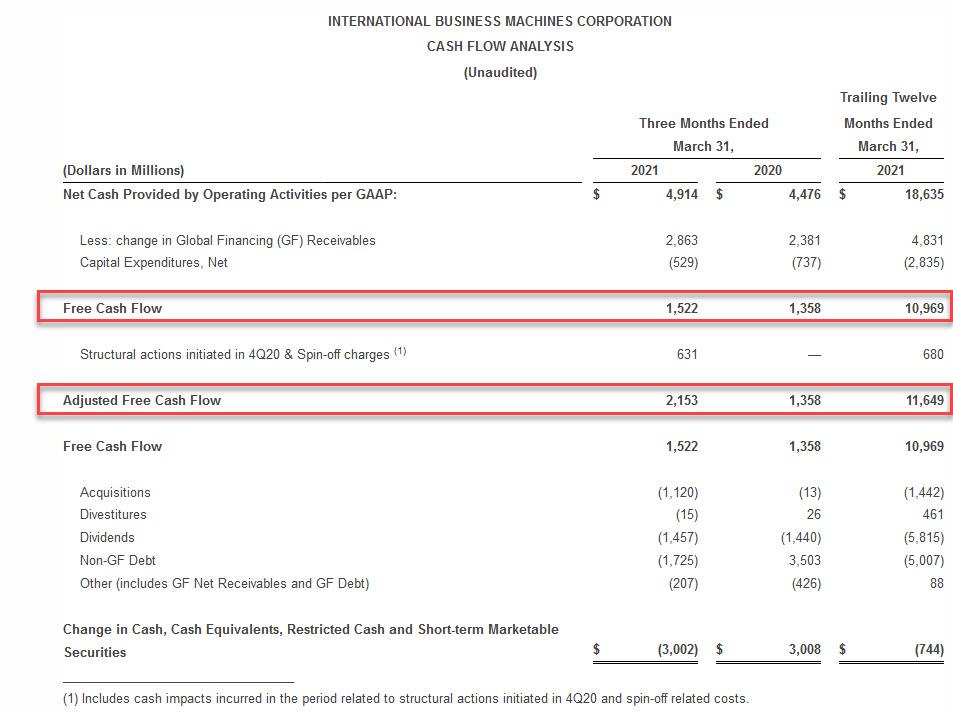

As for IBM meeting its cash flow target, it will have to work extra hard in the rest of the year, because the actual Free Cash Flow in Q1 of $1.522BN was barely higher compared to a year ago.

That said, the adjusted FCF was a little big higher, at $2.153BN, which means that the company did not return all of that to shareholders; instead, it handed out just $1.5 billion in dividends.

So where did the remaining cash go? “In the first quarter we continued to improve the fundamentals of our business model," said James Kavanaugh, IBM's chief financial officer. "With strong cash generation and disciplined financial management, we increased investments in our hybrid cloud and AI capabilities, while significantly deleveraging in the quarter and supporting our commitment to a secure and growing dividend.”

Speaking of cash flow, IBM ended the second quarter with $11.3 billion of cash on hand which includes marketable securities, down $3 bilion from Q4. Debt, including Global Financing debt of $20.9 billion, totaled $65.4, up from $64.7 billion.

And some more good news: for the second consecutive quarter, IBM paid down its debt, which, including Global Financing debt, totaled $56.4 billion, down $5.1 billion in Q1 and down $9 billion since Q3 2020.

In other news, as Bloomberg notes, April marks a full year at the helm for Krishna, who took over the role of CEO from Ginni Rometty with plans to focus on artificial intelligence and the cloud to revive growth after years of stagnation. Krishna has reorganized the 109-year old tech giant around a hybrid-cloud strategy, which allows customers to store data in private servers and on multiple public clouds, including those of rivals Amazon and Microsoft.

Last October, Krishna spun off IBM’s managed infrastructure services unit into a separate publicly traded company, which will be called Kyndryl and be based in New York. The division, currently part of IBM’s Global Technology Services division, handles day-to-day infrastructure service operations like managing client data centers and traditional information-technology support for installing, repairing and operating equipment. The unit has seen business shrink as customers embraced the shift to the cloud, and many clients delayed infrastructure upgrades during the pandemic. It was one of only two of IBM’s units to see revenue decline in the first quarter, with sales down 1.5%. The spinoff is scheduled to be completed by the end of this year.

Bottom line: while IBM's core business remains a melting ice cube, in Q1 the company managed to extract some blood from the ice, thanks to some solid performance in Cloud, which led to the first increase in revenue since 2018, even if the company's bottom line was the usual accounting gimmickry meant to beat analyst estimates at all cost. What is more troubling is that now that IBM is in cash paydown mode, it means little to no growth opportunities, and after algos read through the boilerplate, we expect that the modest rebound in stock after hours will be quickly reversed.

Disclaimer: Copyright ©2009-2021 ZeroHedge.com/ABC Media, LTD; All Rights Reserved. Zero Hedge is intended for Mature Audiences. Familiarize yourself with our legal and use policies every time ...

more