High Dividend 50: 3M Company

3M Company (MMM) is a massive manufacturer, which is heavily diversified across product segments and has a strong global presence. The company is a Dividend King, as it has increased its dividend for 64 consecutive years.

The company has a high yield of 3.9%, well above its trailing decade average. This could be one indicator that the company is currently trading at a discount. However, this is just one detail in a sea of information.

In this article, we will analyze the manufacturing behemoth 3M Company.

Business Overview

3M is a leading global manufacturer, with operations in more than 70 countries. The company has a product portfolio comprised of over 60,000 items, which are sold to customers in more than 200 countries. These products are used every day in homes, office buildings, schools, hospitals, and others.

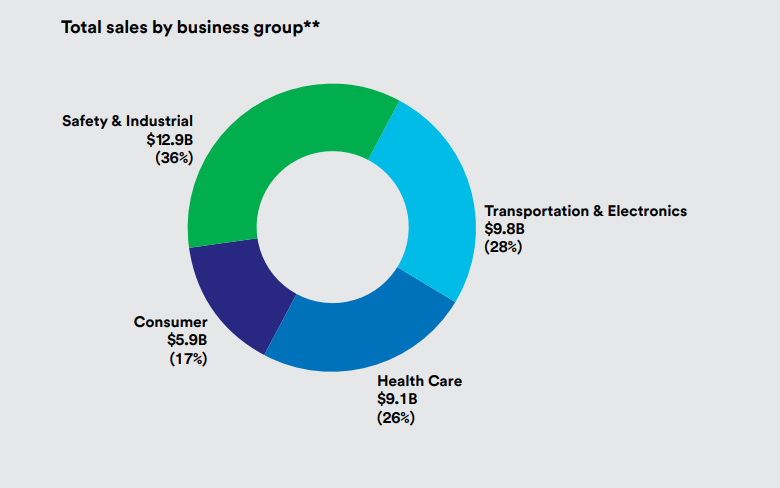

The company’s history can be traced back to 1902 when it was known as Minnesota Mining and Manufacturing. Today, 3M dominates in four significant business segments.

The Safety & Industrial segment produce personal safety gear, industrial adhesives & tapes, abrasives, and supply chain management software.

The Transportation & Electronics segment serves automotive and electronic EOM customers, by producing items such as fibres and circuits.

The Healthcare segment develops medical and surgical products, health information systems, and oral care technology.

The Consumer division sells stationary & office supplies, home improvement and home care products, and protective materials.

Source: 2021 Annual Report

3M reported Q4 and FY 2021 results on January 24th. For 2021, revenue grew 9.9% to $35.4 billion. Earnings-per-share of $10.12 was an 8% increase from the prior year. Adjusted EPS rose 14% though, from $8.85 in 2020 to $10.12 in 2021.

The company generated adjusted free cash flow of $6 billion in 2021. 3M decreased net debt by more than $1 billion compared to 2020. Net debt decreased from $13.7 billion to $12.6 billion by end of year 2021.

3M also returned $5.6 billion to shareholders by way of dividends and share repurchases.

The leadership provided 2022 guidance and sees total sales growth of 1% to 4%, organic sales growth of 2% to 5%, and earnings-per-share of $10.15 to $10.65. Our 2022 EPS estimate is currently $10.24.

Growth Prospects

With so many products in so many different sectors, 3M has the ability to focus on the right growth channels when it is advantageous. The company must allocate their capital and resources to what is most attractive at the time.

The company is currently prioritizing their investments in large, fast-growing sectors which have favorable factors all across the globe. Some examples are automotive technology, home improvement, personal safety, healthcare, and electronics.

The company is firing on all cylinders, with significant growth in its automotive electrification platform, biopharma business, and home improvement business. All four business segments saw high single-digit organic sales growth in 2021. These segments should all continue to grow meaningfully.

Additionally, 3M is likely to make strategic acquisitions, such as with the nearly $7-billion acquisition of Acelity, a leading global medical technology company that manufactures wound care and specialty surgical products. 3M also decided to divest and combine their food safety business with Neogen in 2021.

Competitive Advantages & Recession Performance

3M’s technology and intellectual property are its most significant competitive advantages. These unique advantages have paved the way for 3M to raise its annual dividend for more than 60 years without fail.

3M has more than 50 technology platforms and a team of scientists dedicated to generating innovation. Innovation has afforded 3M the ability to obtain over 100,000 patents throughout its history, which keeps many would-be-competitors at bay.

3M continues to invest heavily in research and development. The company aims to spend around 6% of annual sales on R&D. In 2021, the company spent $2.0 billion on R&D.

The company has done so well in creating new products that roughly 30% of annual sales came from products which didn’t exist five years ago. 3M has established itself as an industry leader across its product segments. The company has remained profitable, even throughout recessions, which can, in part, be credited to their competitive advantages.

Listed below are 3M’s adjusted earnings-per-share results before, during and after the Great Recession:

- 2006 adjusted earnings-per-share: $5.06

- 2007 adjusted earnings-per-share: $5.60 (10.7% increase)

- 2008 adjusted earnings-per-share: $4.89 (12.7% decrease)

- 2009 adjusted earnings-per-share: $4.52 (7.6% decrease)

- 2010 adjusted earnings-per-share: $5.75 (27.2% increase)

- 2011 adjusted earnings-per-share: $5.96 (3.7% increase)

Just because the company remained profitable, does not mean it is immune from recessions, and its earnings-per-share fell in 2008 and 2009. However, the consistent profitability afforded the company the ability to continue increasing the dividend. And EPS bounced back as early as 2010 and continued growing.

Dividend Analysis

3M is a Dividend King and has raised its dividend for 64 years straight. The most recent increase was a penny and a quarter increase, which represents a 0.7% raise. However, 3M has raised its dividend at a compound annual growth rate of nearly 10% in the last ten years, which is strong for such a mature company. But this has slowed as the 5-year CAGR for the dividend is 4.9%.

3M pays an annual dividend of $5.96, and at the current share price, has a high yield of 3.9%. The company has a ten-year trailing average payout ratio of 53%, which is not too concerning. However, the payout ratio has been creeping up slowly.

For 2022, we anticipate a payout ratio of about 58%. Considering the company’s dividend growth has slowed, but the possibility for mid-single-digit earnings growth is still intact, the payout ratio should decrease in the medium term.

The company’s 3.9% dividend yield is quite a bit higher than its trailing decade average of 2.8%, which may indicate shares are trading at a discount.

Final Thoughts

3M is a massive company with a global presence, and as a result, it is fairly reliant on the overall economy. While the company can feel the impacts of recessions and economic weakness, its durable competitive advantages afford the ability to remain highly profitable.

This profitability and strength of the company have allowed it to raise its dividend every year for the last 64 years. We anticipate a reduction in the payout ratio going forward as earnings outpace the slowing dividend growth. This prudence at the company causes us to believe the company will have little problem continuing on this incredible dividend increase streak.

Disclaimer: Sure Dividend is published as an information service. It includes opinions as to buying, selling and holding various stocks and other securities. However, the publishers of Sure ...

more