Headwinds On The Active Horizon

Active managers’ performance was disappointing in 2020, despite the market’s heightened volatility. As the market continues to march upward in 2021, it’s natural to wonder if current conditions are favorable for stock pickers. We expect active managers’ difficulties to persist.

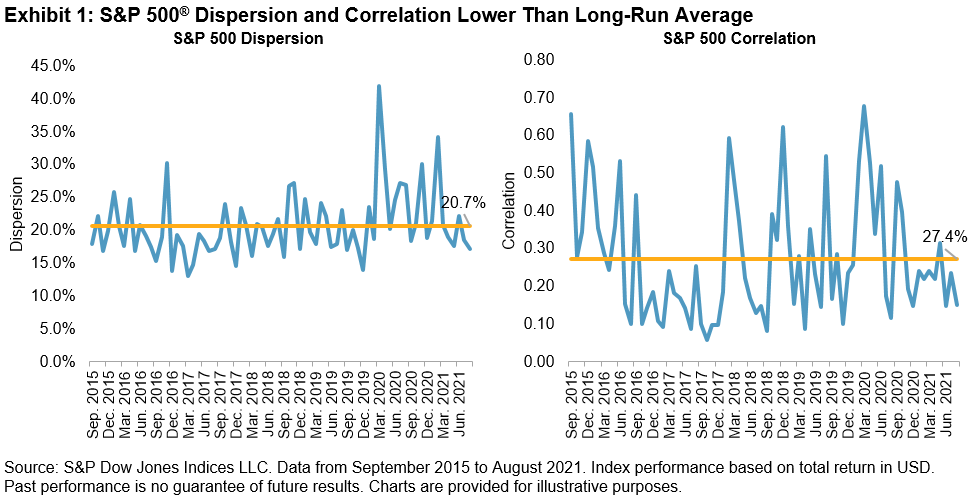

We can think of volatility in terms of its components: dispersion and correlation. Active managers should prefer above-average dispersion because stock selection skill is worth more when dispersion is high. At the same time, the price of an active strategy—in terms of incremental volatility—will be relatively small when correlations are high. Both correlation and dispersion are currently below average, as we see in Exhibit 1, indicating relatively inauspicious conditions for active managers.

(Click on image to enlarge)

As a result, the required incremental return for large-cap active managers has risen as correlations have declined, which means they are giving up a greater diversification benefit. Meanwhile, lower dispersion makes it harder to add value. We see similar results for smaller-cap active managers, signaling a relatively more challenging environment for active management.

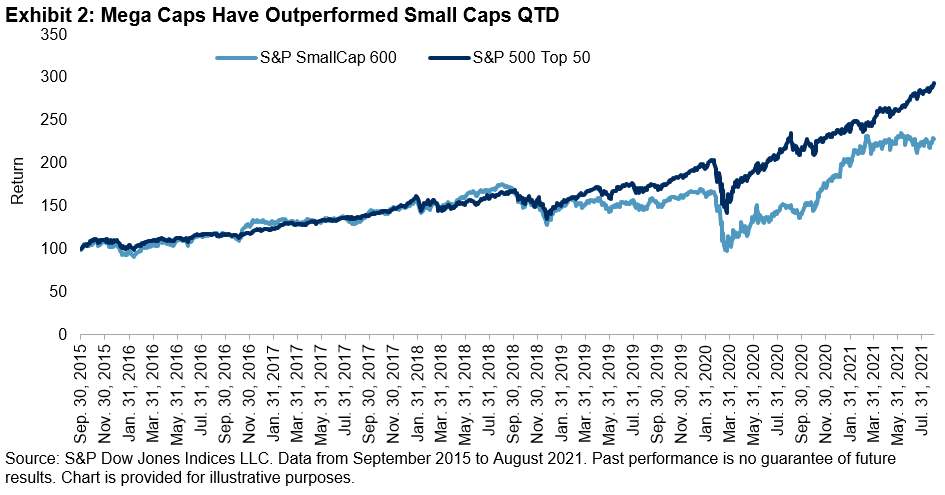

Large-cap active managers face an additional style bias hurdle. Most active portfolios are closer to equal than cap weighted, which means that they have an advantage when smaller stocks outperform. Unfortunately, Exhibit 2 shows that the largest names have recently been performance leaders.

(Click on image to enlarge)

The dominance of mega caps also hinders stock selection, as illustrated in Exhibit 3. In the first quarter of 2021, 59% of S&P 500 members beat the index, when smaller-caps were outperforming. Since then, the tide has turned, and only 34% of stocks outperformed the index, as mega caps outperformed during this period.

(Click on image to enlarge)

The current bleak environment does not bode well for active managers. We recall that 2020 was characterized by relatively favorable conditions for stock selection, and most active managers still underperformed, proving that genuine stock selection skill is rare. If these trends continue, when SPIVA results for 2021 become available, it would not be surprising if we saw lackluster active management performance once again.

Disclaimer: Copyright © 2021 S&P Dow Jones Indices LLC, a division of S&P Global. All rights reserved. This material is reproduced with the prior written consent of S&P DJI. Please ...

more