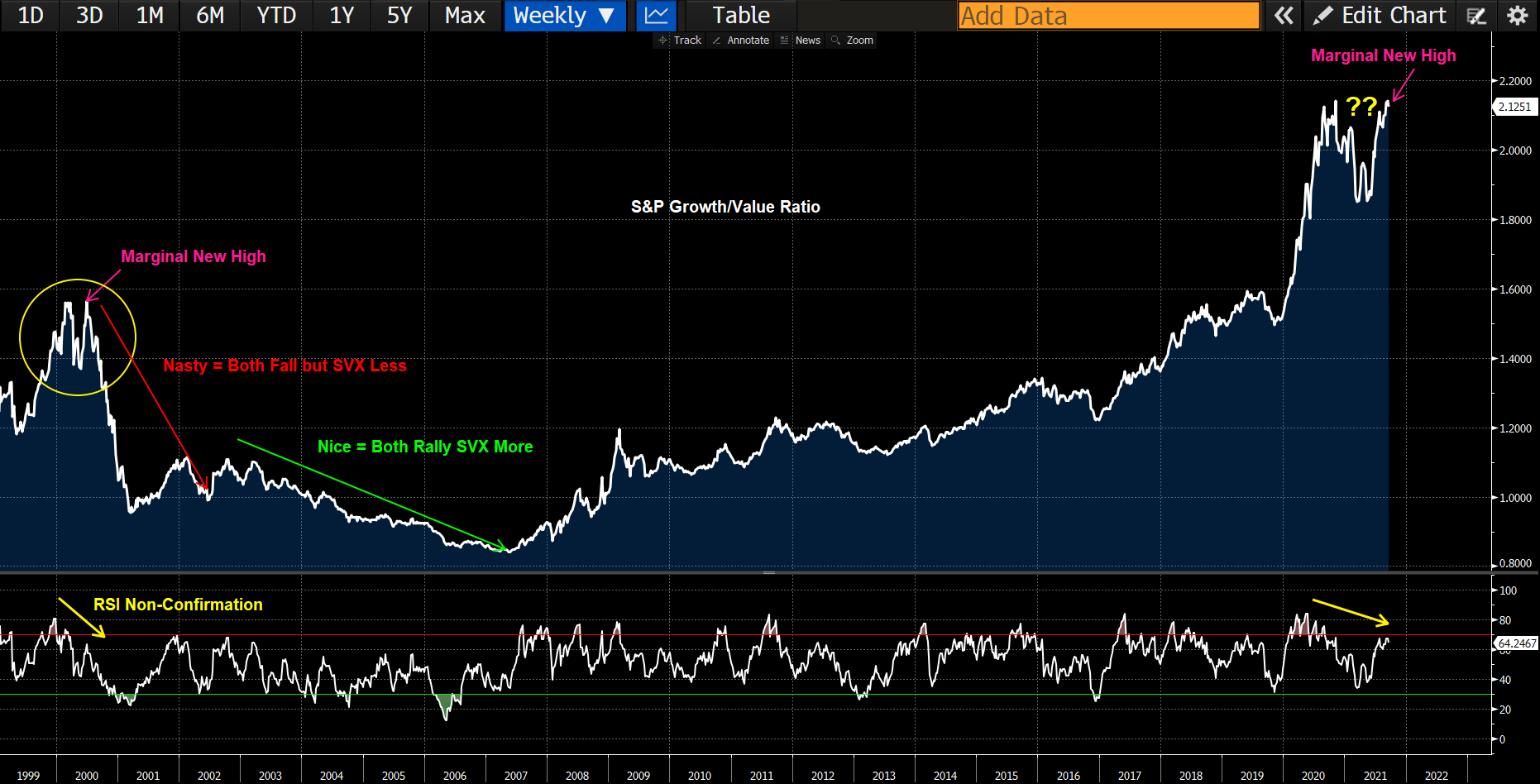

Growth/Value Spread At New Marginal High

The image above shows the S&P Growth/Value ratio. As you can see, this ratio has hit a new marginal high, to an all-time record. This means that the valuation spread between growth and value has never been more extreme. Interestingly, we saw a similar pattern occur in 2000, right before the Nasdaq began its plummet of roughly 80% over the next few years, while value had seven of its best years ever. I’m not a chartist, but charts can tend to show patterns of human behavior such as greed and fear. There have been no consequences for buying the dip, including in many of the most expensive stocks, in one of the most expensive market environments in history, for a very long period of time. I don’t believe that is sustainable over the long term, but predicting the timing of when that dam breaks is just not my game.

What I do know is that we are able to currently find investment opportunities in attractive businesses trading at less than 10 times normalized earnings and with dividend yields often over 3%. Importantly, these companies are growing earnings and are growing their intrinsic values per share. I believe that many of these companies will benefit from a higher interest rate environment, which would come if we see inflation stick a little higher than Fed officials believe it will. These are deep value stocks that have done well over time, just not as well as some of the highest-flying growth stocks have done, but I’d argue they are also far less risky, thereby offering a much more attractive risk/reward. Making 30% returns for three years, and then losing 80% is not a great long-term investment strategy; which is why simply chasing whatever is hot without looking at the underlying fundamentals, can be a very costly mistake.

One lesson I’ve learned whether it is business, investing, exercise, or just life, is that there are tremendous rewards in following the right process, not just in the destination. By investing in undervalued companies and using disciplined strategies, which enhance our risk/reward probabilities, we are positioning us to attain strong long-term investing returns. We tend to avoid the massive bubbles, which can lead to permanent losses of capital, as opposed to the inevitable mark to market losses, which are truly transitory in nature. It isn’t always easy, as greed and fear are ever-present emotions on the investing journey. “Let’s dial up the risk, as my neighbor just made 40% on this IPO or SPAC stock.” Or, “let’s sell everything as I just have a feeling the market is going to pop.” These are emotions that financial advisors such as us, hear on at least a weekly basis, and have heard over many years. If there was a crystal ball or prescient that accurately could predict those types of things, everyone would be following it, but if you look at who the best long-term investors are, they are the ones that stick with a well-researched process.

Every strategy has good and bad years, this year value has done fantastic, while last year was the worst ever for it. However, by sticking with the strategy in bad times, we were able to buy stocks at deeply undervalued prices, allowing us to capitalize on the recovery, which in our estimation, is still in the very early stages. The flip side to buying some of these growth names or the overall indices at current prices is that there will be periods when the market assigns a far lower multiple on earnings and cash flows on these same businesses. When that occurs, you can easily get a lost or negative decade of investment returns, like we saw after 2000 for growth and the indices, which was the most comparable period in terms of valuations. The value investors that looked like idiots back in 1999, looked really smart by not losing everything when that bubble crashed. We intend to carefully navigate what we believe to be almost an Everything Bubble, so that your hard-earned capital is protected and grown in an intelligent and thoughtful manner over the long term, with the full knowledge that we will look like idiots in some of those years, as is indeed an inevitable reality of the business. Our success will be best judged over the long term and in helping you and your families achieve your financial goals and objectives.