Google Has A Way To Grow Again

Google (GOOG, GOOGL) has been treading water largely the past year as growth has seen some bumps while investors have questioned where the leviathan company may still have room to expand to. However, while Google is late to the diversification game, it is not out.

In fact, the company is posting healthy signs of potential expansion into a wide variety of non-search products that could be the key to sustaining and bolstering its growth for the near- and medium-term future.

Despite Google's "Cloudy" Financials, We Can Still See The Gems

Ever since the beginning of 2018, Google's market price has been in a zig-zag motion, as its price has bounced up and down and leaving it with essentially flat net growth. This has come amid a wide variety of reasons, ranging from broader technology market headwinds due to trade conflicts to government antitrust action and regulatory enforcement concerning data privacy.

While the company was frequently spoken of as a potential $1 trillion company as far back as early 2018, so far it has hovered close to that bar for now almost two years. The company's price remains slightly down year-on-year.

Data by YCharts

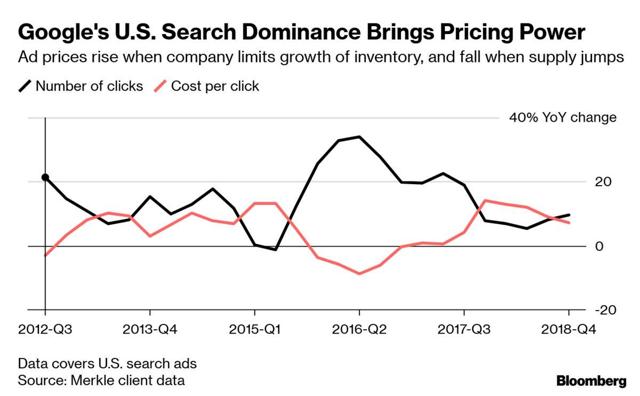

It has also been due to Google's own seemingly shaky financials and growth amid its non-transparent financials in which there is essentially no breakdown among the countless Google segments, products, services, companies, and activities that comprise the company's operations and continuing advancement.

This lack of transparency has real-world price impact, as Google's stock price fell as low as -8.8% immediately in the wake of Q1 2019 earnings due to revenue growth slowing below 20% and there lacking any explanation why.

Even if Google's shroud over its financials and operations remains intact, we can still likely extrapolate some measure of expectation for future more accurate and useful than just reading the tea leaves.

The Secret To Late-Stage Tech Behemoth Growth Is Diversification

Google is at the point where, like many other tech giants such as Apple, Amazon, Facebook, and others, it is expanding to a variety of products and services areas beyond its original core. For Google, that core remains its search engine - yet, even with the company's simple financials, we can see its non-search activities are growing in revenue.

As compared to Q2 2018, in Q2 2019, Google saw its "other revenues" segment increase from $4.425 billion to $6.181 billion for an astounding 39.7% year-on-year growth. The company made a mind-blowing $136.819 billion in revenue in 2018. However, much of the particularly interesting growth has come from non-search core of Google, such as its various hardcore products, software, and Internet services such as Google Maps, artificial intelligence operations, and more.

Google is still early on in, but on track to, follow the mold of other successful technology behemoths that ran into walls for growth and then broke through. Microsoft (MSFT) and Amazon (AMZN) both reached a $1 trillion market capitalization not through expansion of their core business segments but through utilizing a combination of network effects and intra-system benefit to diversify their revenue base and thus find new areas for growth.

For Google, its opportunity, and where it seemingly is on track to go, is that. In terms of its search engine, the company has, like Facebook (FB) for social networking, grounded a firm market lead that now seems all but unassailable. Facebook is now expanding into side services, often very high margin and easy growth due to being connected with its core social networking platform. Google has long remained entrenched primarily in its search engine core but now can, and is, broadening out to a large variety of other services and products that stand a chance of keeping its growth healthy and strong.

Amid all this, it is worth remembering that Google's price to earnings ratio is a mere 24.49. Microsoft's is 27.22, Amazon's is 74.86, and Facebook's is 30.65. Essentially, among the FAANG software/services-oriented behemoths, Google retains the lowest price-to-earnings ratio, and on the lower side, in general, for a technology company with a still-intact growth thesis. This means downside is low while growth remains possible still.

Even if growth dips below 20%, still adding say 10-15% EPS growth with a steady P/E ratio means the stock should similarly begin continuing to tug up 10-15% a year. If the P/E ratio expands slightly to be similar to other tech behemoths, which it might if Google begins winning more of its tech tug-of-wars in all these various non-search subsectors, a small P/E expansion could easily add another 5-10% annual growth on top of that.

Conclusion

Google's path to $1 trillion has stalled the past two years but it is no pipe dream. The company retains a firm base in search with steadily expanding explorations, opportunities, and products and services in a wide spectrum. These will be the key to the company's ability to keep expanding and growing as it follows the strategy that several other tech behemoths have successfully pursued for late-stage rekindling. Amid this, I still see optimism and great hope for Google.

Disclaimer: These are only my opinions and do not constitute investment advice.

I think #Google is undervalued. It's got its hands in a little bit of everything and will only continue to grow. It's uniquely positioned to thrive. $GOOG $GOOGL

Great insight.