Friendly Skies — For Airline Investors, Not Passengers

One of Warren Buffett’s few unsuccessful investments was buying convertible preferred stock of USAir in the late 1980s. For decades after that episode, Buffett would characteristically make fun of himself, while decrying the entire airline industry for its capital requirements and onerous competition.

As he put it in an interview, “If a capitalist had been present at Kitty Hawk back in the early 1900s, he should have shot Orville Wright. He would have saved his progeny money. But seriously, the airline business has been extraordinary. It has eaten up capital over the past century like almost no other business because people seem to keep coming back to it and putting fresh money in. You’ve got huge fixed costs, you’ve got strong labor unions and you’ve got commodity pricing. That is not a great recipe for success. I have an 800 (free call) number now that I call if I get the urge to buy an airline stock. I call at two in the morning and I say:

“My name is Warren and I’m an aeroholic.’ And then they talk me down.”

But Buffett seems to have changed his mind lately, and maybe so should other investors. In a Berkshire Hathaway filing from September 2016, almost three decades after the USAir debacle, three of the four airlines – Delta Air Lines, UnitedContinental, and American Airlines – appeared among the firm’s publicly traded holdings. By the final filing of that year, Southwest, the fourth in what Jonathan Tepper’s The Myth of Capitalism calls an oligopoly that now dominates the industry, appeared on the holdings list. All four have been there ever since, and it’s not because he 88-year-old Buffett has lost his marbles.

Somehow, a fragmented, intensely competitive industry plagued by unions and underfunded pensions, has become insulated enough from competition that Warren Buffett wants to own the major players. It’s not simply that Buffett now owns an airline. It’s that an investor whose calling card has been finding a company with a durable competitive advantage now owns four major players in an industry that are virtually indistinguishable from each other except for their ability to dominate hubs and routes and seemingly divide the industry among themselves against smaller competitors.

As Robert Kuttner wrote in the New York Times after an overbooking debacle made headlines, “air travel is far from a free market.” That because airlines, once heavily regulated, competed so hard after deregulation that they all went broke. In the 40 years and more than 40 mergers since deregulation in 1978, carriers divided up “fortress hubs,” maximizing pricing power and crushing smaller competition that tried to break into a hub. “An industry that is not naturally competitive went from being a regulated cartel to a brief period of ruinous competition, and then to an unregulated cartel. . . . [restoring] profitability, but at awful costs both to customer convenience and to economic efficiency as well,” says Kuttner. The solution is regulated competition, according to Kuttner, but the Justice Department now prefers “concentration and collusion” to regulated competition, according to another Times piece.

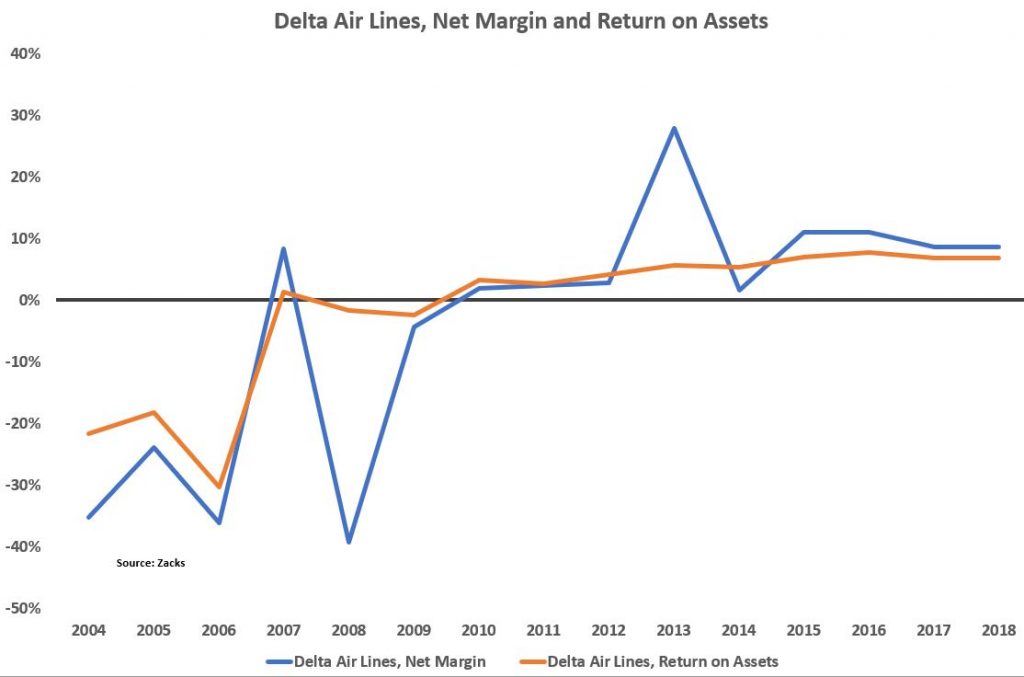

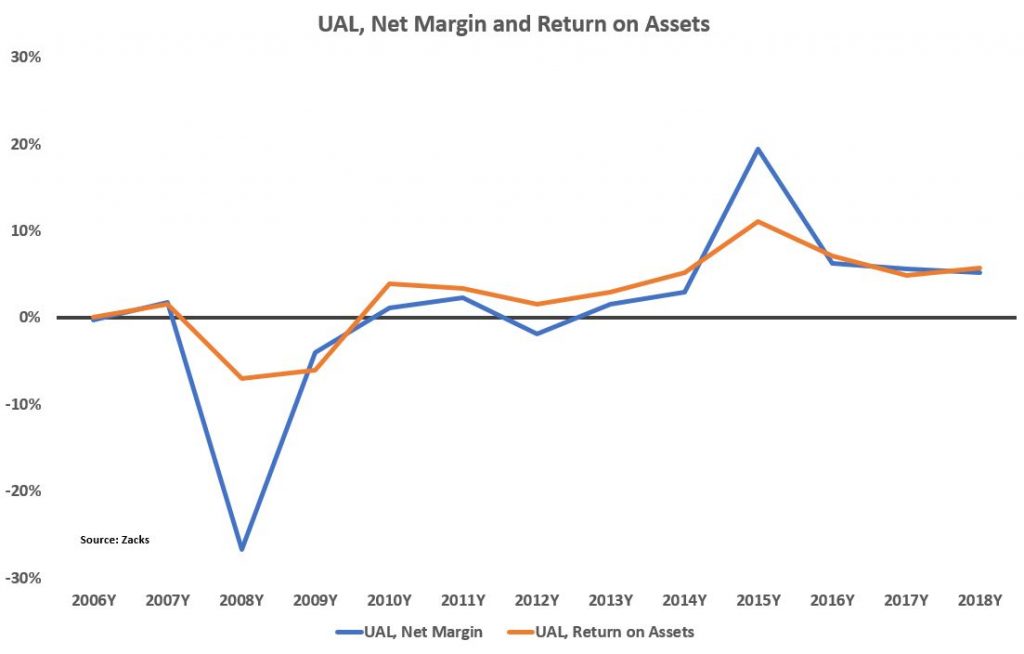

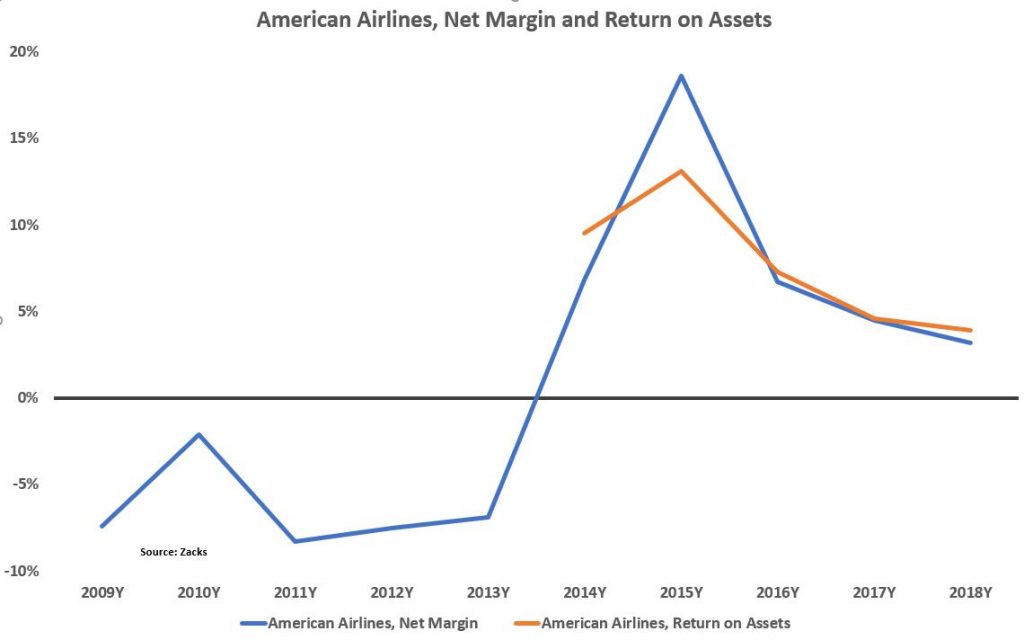

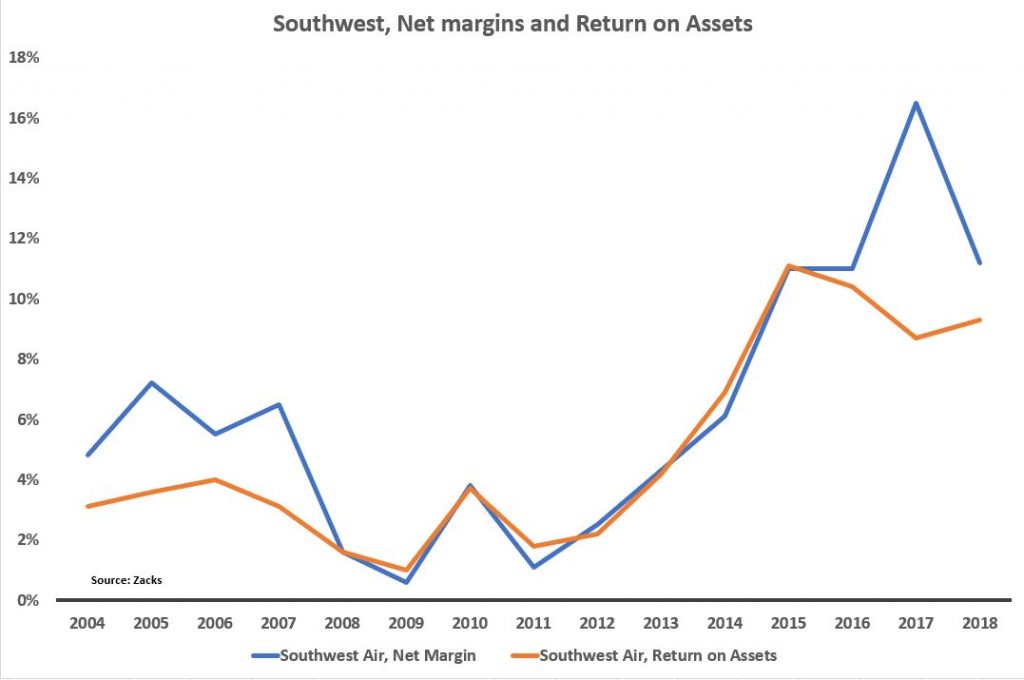

Airline profitability is also now evident in the numbers. After mostly burning capital from 2004 through 2010, Delta has settled into a remarkably stable mode of posting positive margins and posting respectable returns on assets year-in and year-out. The same general pattern exists for the other big three in the industry.

If you’re concerned that the Justice Department will start to take a harder look at all the mergers that have occurred over the past 40 years, this investment isn’t for you. If you think the Justice Department will continue to remain asleep at the switch, then the airlines are eminently investable. Profits and returns on assets are not mind-blowing compared to some information technology companies, but they have turned positive for the foreseeable future. Oligopolies and the collision — even if tacit — that usually occurs within them usually make for a healthy investing situation. It’s probably best to follow Buffett and own the whole group though.