At last week’s FOMC meeting, Jerome Powell said, “We think financial conditions are weighing on the economy.”

His comments seem sensible, given the following:

- The Fed is reducing its balance sheet (QT).

- The Fed Funds rate is at its highest level in over 15 years.

- Mortgage rates are about 7%, 3-4% above pre-pandemic levels.

- Credit card interest rates are 20% or more.

- Auto loans range between 7% and 10%

- Consumer loan growth, excluding the pandemic, is down to levels last seen over ten years ago.

- Outstanding Commercial & Industrial (C&I) loans are declining.

Powell’s statement indicates that financial conditions are tight. However, they are easy based on the Fed’s definition of financial conditions. If Powell doesn’t appreciate the difference between financial and borrowing conditions, we must assume most investors do not either.

As we will explain, there is a big difference between financial and borrowing conditions. Equally worth considering is that the current combination of easy financial conditions and tight borrowing conditions makes monetary policy difficult for the Fed to balance.

What Are Financial Conditions?

The St. Louis Federal Reserve defines financial conditions as follows:

“Measures of equity prices (also commonly referred to as stock prices), the strength of the U.S. dollar, market volatility, credit spreads, long-term interest rates, and other variables.”

Financial conditions tend to be easy when investors are optimistic and speculative. Let’s look at the four critical measures in the St. Louis Fed definition to understand why financial conditions are easy today.

Equity Prices: The S&P 500 is up 38% since 2023 and 10% through the first three months of 2024.

U.S. Dollar: The dollar index has been relatively flat since 2023 and the year to date.

Market Volatility: The VIX volatility index has been hovering between 12 and 15 this year. That is about one standard deviation below the average VIX reading of 19.32 over the last 35 years.

Credit Spreads: The BBB investment grade yield is only 1% above a comparable maturity Treasury. Such is the tightest spread since the 1990s.

Long-Term Interest Rates: Long-term interest rates have been significantly higher than average over the past few years and at levels last seen before the financial crisis in 2008. However, they are about 1% lower than their peak last year.

Equity prices, market volatility, and credit spreads point to very easy financial conditions, and we might also characterize their levels as speculative.

The dollar has had little effect on financial conditions as it has been relatively stable.

Long-term interest rates point to tighter financial conditions, albeit easing over the past six months.

The bottom line is that financial conditions are easy in large part because robust sentiment in the equity and credit markets more than offsets higher interest rates.

As shown below, our proprietary SimpleVisor Sentiment indicator is at its maximum level, and the CNN Fear & Greed Index is closing in on extreme greed.

(Click on image to enlarge)

What Are Borrowing Conditions?

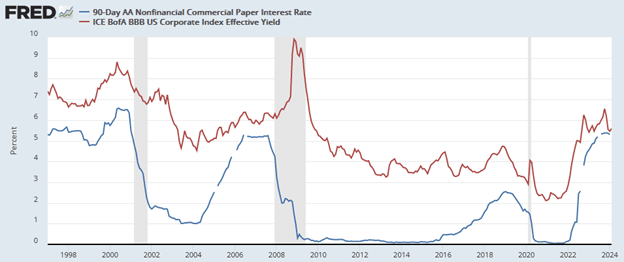

Unlike financial conditions, borrowing conditions are far from easy. The two graphs below highlight the financial stress on consumer and corporate borrowers.

Credit card interest rates are over 20% and about 5% above the highest in the past 24 years. Mortgage and auto loan interest rates are up to levels not seen in at least fifteen years.

The following graph shows that 90-day commercial paper loans and yields on BBB-rated corporate bonds are at their highest levels since the financial crisis.

What Can And Can’t The Fed Manage?

The Fed plays a crucial role in directing financial and borrowing conditions. At times, like today, financial and borrowing conditions can be at odds with each other, which makes the Fed’s job of managing monetary policy more difficult.

The market’s perception of the Fed’s stance, hawkish or dovish, and more importantly, forecasts of how they may change policy can heavily impact market sentiment and financial conditions.

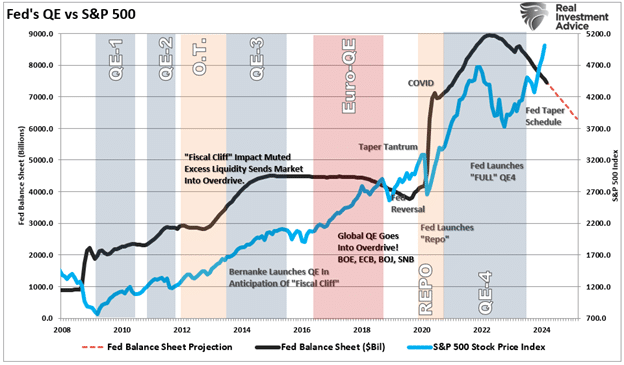

For instance, a strong correlation exists between QE and higher stock returns, lower volatility, and tighter credit spreads. The relationship occurs in part due to the psychology of investors. However, it’s also a function of the liquidity the Fed creates when conducting QE. For similar reasons, lower rates are thought to be beneficial for markets.

The Fed has a heavier hand in determining borrowing conditions. By managing its Fed Funds rate, the Fed sets the tone for long-term interest rates and significantly influences shorter-term rates. Further, QE and QT can add or subtract liquidity from the markets, directly affecting the supply and demand of liquidity available to all markets.

Powell’s Predicament

Financial conditions have eased considerably as investors priced out the odds of rate increases and have started pricing in rate cuts. The combination of lower interest rates and possibly less QT, coupled with robust economic growth, is the goldilocks scenario driving investors’ sentiment higher. This occurs despite extremely tight borrowing conditions and a hawkish monetary policy.

Currently, the Fed does not want financial conditions to ease further as the wealth effect of strong markets can have an inflationary impulse. They could hike rates or even talk of increasing rates to weigh on financial conditions. However, with tight borrowing conditions and the potential that the lag effect of prior rate hikes will ultimately cause a recession, they appear to be in no man’s land.

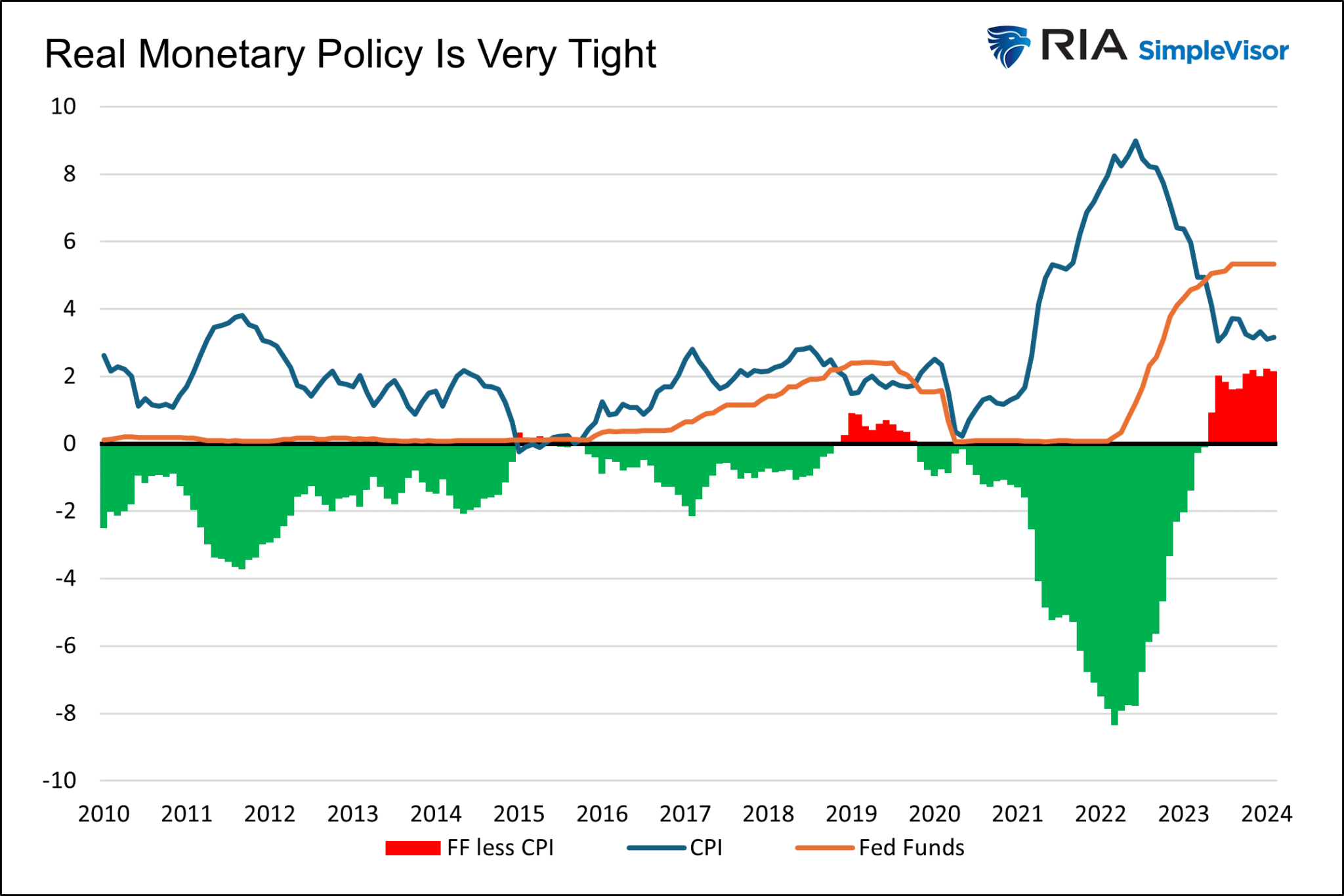

As we share below, on a real basis, the Fed’s policy stance is the tightest it has been in fifteen years.

Another Fed Predicament Coming Soon

Sentiment and liquidity drive markets in the short run. Both have supported higher stock prices and mania-like trading in AI stocks and cryptocurrencies.

However, that could be changing. As we note in Liquidity Problems, excess liquidity is rapidly draining from the financial system. The Fed knows the situation and may be called upon to deal with a liquidity shortfall. QT reductions and/or lower rates would ease liquidity concerns. But, doing so, especially if the economy stays robust and market sentiment is strong, would risk further easing of financial conditions, which in turn may keep inflation sticky at current levels.

Summary

The Goldilocks economy, coupled with the end of the rate hiking cycle, has investors giddy, which eases financial conditions. Ironically, while some of the easiest financial conditions in the last ten years have existed, borrowing conditions remain very tight.

The Fed must balance these two conditions, which is difficult as they can counteract each other. Threading the eye of this needle may prove problematic given that inflation remains too high and, more recently, is showing some signs of being sticky.

More By This Author:

QE By A Different Name Is Still QE

Liquidity Problems Are Closer Than You Think

Apple's Magic - Are Buybacks Worth Paying Up For?

Comments

Log in or sign up to join the conversation.