Final Trading Day Of 2018 Is Met With Bearish Sentiment For 2019

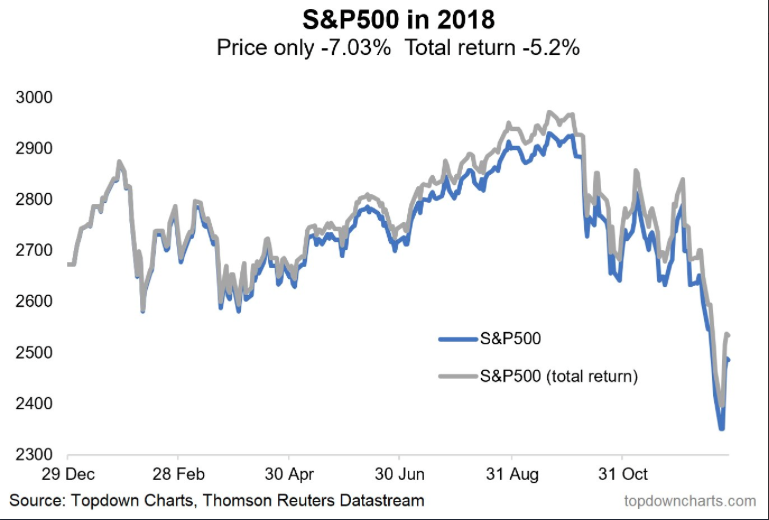

Good weekend to everyone and with the final trading day of calendar year 2018, I can’t help but desire the calendar year to end with some semblance of positivity. Last week kicked-off a holiday-shortened trading with much anxiety being created for investors on Christmas Eve and as the market meltdown continued. The S&P 500 (SPX) fell into bear market territory briefly and joining the Nasdaq (NDX) and Russell 2000 (RUT).

A sharp market snapback the day after Christmas helped bring the S&P 500 within normal correction territory, but we take the snapback rally with the grain of salt at the moment. Why? To answer that question we have to analyze what caused the market’s meltdown from the all-time highs reached in September of 2018. In order to do so we have to travel back to mid-September.

So what happened in mid-September, which proved to be the peak for the market in 2018? It’s really quite simple, the U.S. Administration imposed another $200bn in tariffs at a 10% tariff rate on Chinese imports. The announcement was made after the markets had closed on September 17, 2018.

Up until this moment, it was widely speculated that some deal would be reached between the two superpowers in an effort to de-escalate the growing tensions that were also spreading around the world. Nonetheless, the market had one last leg higher on September 20, 2018, and before giving way to a 4th quarter 20% decline.

(Click on image to enlarge)

If the trade feud escalation didn’t prove to undo the bull market on September 17th and with additional tariffs implemented, the FOMC only weighed on investor sentiment that much more and when the Fed raised rates.

Along with raising rates by .25 bps on September 26th, the Fed removed the “accommodative” language from its forecast while raising its economic outlook for Q4 2018 and for the whole of 2019. The removal of seemingly dovish language and raising its economic language seemed to put the Fed on rate hike autopilot, even as a global economic slowdown seemed inevitable in the months ahead. Europe was in political strife and China’s economic data showed a steady slowdown was at-hand. The yuan was tumbling and all the while the U.S. remained the beacon of light for investors. But then came October…

As depicted in the chart above of the S&P 500, the market immediately started to fall at the onset of October and likely under the weight of realizing the trade feud would not find favorable resolution in 2018 and the FOMC was decisively more hawkish and intent on raising rates further. The two factors proved too much to burden for investors in what was also the longest bull market in history. So what now?

January-Earnings Season

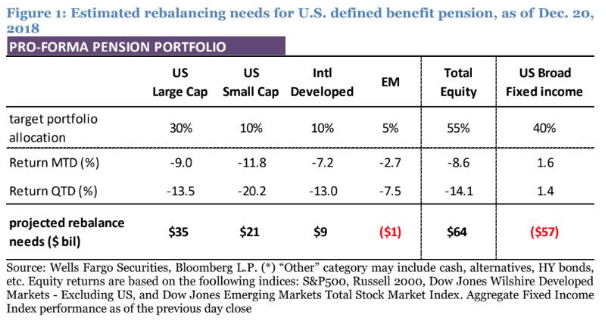

Before the New Year begins, pension funds take center stage. As of Dec. 20, Wells Fargo (WFC) estimated defined-benefit pension plans for U.S. corporations needed to shift around $64 billion of funds into stocks before the end of the year.

“There’s no question this is a historically large amount. We’ve been crunching numbers on pension quarter-end flows for a good part of seven years. This is frankly the largest rebalancing amount we’ve seen,” Boris Rjavinski, senior strategist at Wells Fargo Securities, told MarketWatch (see table below)."

When we enter the month of January, the market will either retest the most recent lows and/or be directed by earnings and FY19 guidance offerings during earnings season. Low-level retests are always a high probability, but they depend on many variables and as such are not guaranteed.

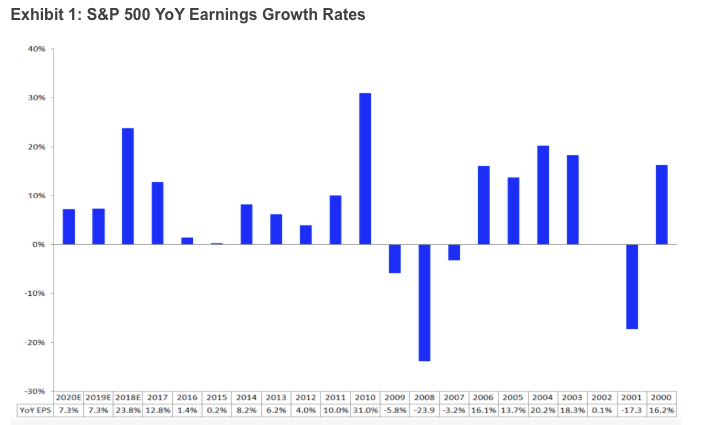

Earnings season is set to commence in earnest in mid-January. That gives the market 2 weeks to meander and contend with geopolitical and macroeconomic data. At present, Thomson Reuters estimated earnings growth rate for the S&P 500 for 18Q4 is 15.8 percent. If the energy sector is excluded, the growth rate declines to 13.8 percent.

When companies start to report earnings for the Q4 period, the S&P 500 is expected to see 2018 revenue increase by 8.7% and earnings to increase 23.8 percent. This is the highest earnings growth rate since 2010’s 31.0 percent. Quarterly earnings for 2018 have beaten estimates at a rate of 78.6%, which is on track to be the highest on record (through 1994). Some are quick to dismiss the earnings performance and over-attribute it to tax reform, which is expected to see the index’s effective tax rate decline to 20% from 26%; however, even if the tax benefits were backed out, earnings growth would be 14.3%, which would still be the highest since 2010.

Once Q4 earnings come into focus, FY19 guidance will prove to move markets in one direction or the other. Many are of the opinion the downdraft in the market, which values the S&P 500 at roughly 14.5% F12M PE, is compromised by the inevitable lowered earnings expectations. Thus far and leading up to earnings season, F12M earnings estimates have only come down slightly, from 8-10% a few months ago to roughly 7% presently. Historical evidence that suggests analysts are slow to revise estimates combined with expectations for stable pre-tax profit margins and recent company guidance seems to favor the idea that the market is likely predicting the FY19 will see downward revisions to EPS estimates and once earnings season gets underway.

What Man Has Done, Can be Undone

2018 could easily be characterized as one of the most geopolitically charged years of the 21st Century. From Brexit to Italy’s budget battle and the wagering of trade feuds around the world, most asset classes will finish in negative territory for the year.

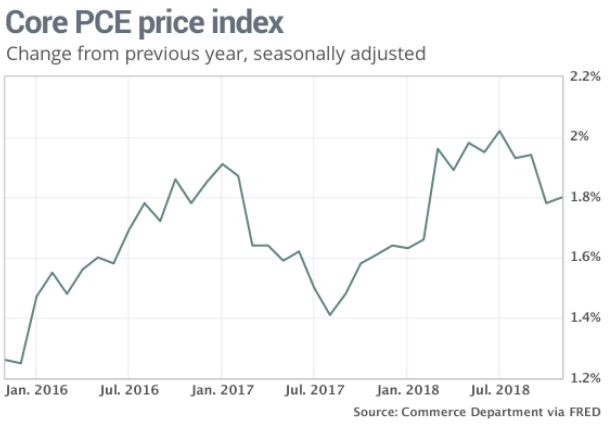

In 2019, investors will largely be looking to see if the FOMC and U.S. Administration can undue all that ailed the markets in 2018. The FOMC has already taken large steps to reassure the markets that “autopilot” doesn’t exist. The Fed Chairman has walked back any and all language that can be perceived as being autopilot-driven rate hike activities. Within the most recent FOMC meeting press conference, the Chairman declared the FOMC’s reversion to data dependency as the inflation mandate of 2% inflation was not achieved again in 2018. (See PCE chart)

The FOMC’s second mandate on employment, however, was and continues to be achieved as record level low unemployment of 3.7% has sparked the economy. As it pertains to the Fed’s balance sheet unwind, this brought about new angst amongst investors until recent comments from Fed Governor John Williams also walked back the previous and seemingly hawkish stance on unwinding activity. Since peaking at just below $4.5trn, the Fed has been decreasing its balance sheet throughout 2018. Some view the Fed’s $50bn in Treasury run-off as another quarter rate hike.

“In an interview on CNBC’s “Squawk on the Street, ” Williams made it clear the Fed would be dependent on economic data and other signs of business activity and sentiment before making a decision on interest rates. He also said the Fed will go into next year with its “eyes wide open” and reconsider programs such as its balance sheet reduction, if necessary.”

Fed Governor Williams’ comments helped to, once again, reassure investors and markets that the FOMC would remain flexible with regards to policy and all other fiscal activities.

While the Fed is showing signs of flexibility going forward, it has forecasted 2 rate hikes for 2019. We believe the Fed has already been found to have impacted certain sectors of the economy negatively (housing), and slowed domestic growth expectations enough to suggest a pause in rate hikes. Additionally, the Fed has failed to achieve its 2% inflation target for 2018, which would otherwise spur the Fed to raise rates. If I were to grade the Fed’s tightening cycle performance under Chairman Jerome Powell, I would offer a C to the Fed. Communication has been ineffective and resulted in market stress/volatility. The message of raising rates with inflation under the Fed’s target goal and economic growth forecasts being lowered simply don’t align. The Fed may have a dual mandate, but communicating the actions through the validation of achieving such mandates has failed markets.

Moving beyond the FOMC’s more dovish stance and reduced rate hike outlook, investors are also looking for some positive news on the trade front. As it was with the FOMC, it is with the trade feuds; these are both manmade crises. Both can be remedied.

Over the weekend, headlines were once again skewed toward President Donald Trump’s twitter feed.

Xi was said to tell Trump that he hopes to push forward a Sino-U.S. relationship that is coordinated, cooperative and stable, Chinese state media reported.

Xi said teams from both countries have been actively working to implement the recently reached consensus between China and the United States, state-run Xinhua news agency said. He added that he hoped the teams could meet each other half way and reach an agreement that is mutually beneficial as soon as possible, the organization reported.

I am of the opinion that the latest headlines indeed sound more promising and with greater verbiage than previous headlines. This suggests that both parties are experiencing pressure from their underlying economies or capital markets. As I mentioned in previous reports, markets tend to guide policy.

If the powers that be can find the removal of the two biggest headwinds for the market in 2019, trade feuds and rate hikes, the market has a strong probability of gains in 2019. I won’t go so far as to say the S&P 500 will achieve a new high just yet, although the case could be made under the premise offered. But again, there is a great amount of heavy lifting to be done in order for all of the variables to align favorably for investors.

S&P 500 Near-Term

In early December I asked subscribers to finomgroup.com (for who I am employed) to review the following S&P 500 BOX. The box is presented in the chart below.

(Click on image to enlarge)

“The problem for the bulls and where we finished the week, at the lower zone, is a triple bottom tends to find a break lower and not higher. The set up is indicating RISK-OFF for the coming week. And for this reason we believe in the benefit of hedging one’s portfolio during the coming week.”

Unfortunately, the box did break and the S&P 500 found itself, briefly, in bear market territory. The S&P is still down roughly 15% from its all-time highs folks. What we opine will happen next, and after a rebound week that was, is that the S&P 500 will aim back higher, for the bottom of the S&P 500 Box. Even with a positive move opined near-term, I believe earnings will guide the way longer-term. Until I have some certainty from earnings guidance, risk off remains the more dominant theme amongst investors.

For the coming week, the markets will have a full trading day on New Year’s Eve, but the markets will be closed on New Year’s Day. With only 4 trading days in the coming week, the market is still expecting a good deal of volatility with the VIX above 28. The S&P 500 expected move for the week is roughly $84 in only 4 trading days. As such, we expected big moves in either direction this coming week, as realized volatility may prove greater than implied volatility. That basically means we do expect volatility to continue its decline this coming week supporting the general opinion that the S&P 500 will aim for 2,575 or so.