Dividend Stock Analysis Of Johnson & Johnson (JNJ)

Johnson & Johnson (JNJ), together with its subsidiaries, is engaged in the research and development, manufacture, and sale of various products in the health care field worldwide. The company operates in three segments: Consumer, Pharmaceutical, and Medical Devices & Diagnostics. This dividend king has paid dividends since 1944 and has managed to increase them for 57 years in a row. Dividend increases have been like clockwork every year for decades.

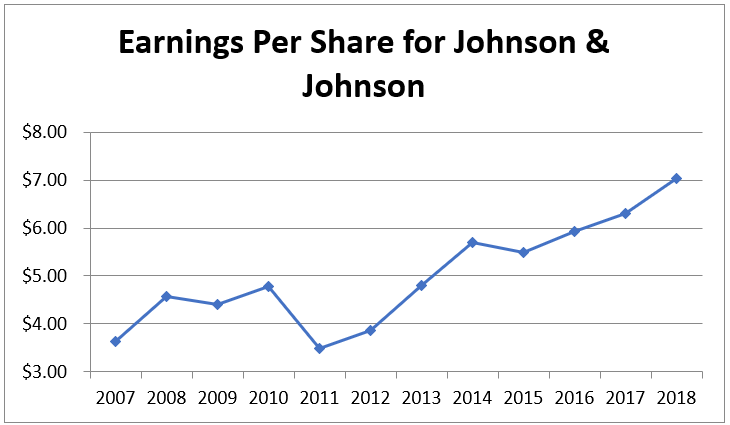

Johnson & Johnson earned $3.63/share in 2007 and managed to grow earnings to $6.31/share in 2017 (adjusted for the provisional amount of $4.94/share associated with the recent enactment of tax legislation as well as a 90 cent/share charge for intangible amortization expense). The company just announced its latest earnings for 2018, which come out to $7.03/share. The amounts include $1.42/share in annual intangible amortization expense. I add this back, because it is a non-cash GAAP requirement, which requires companies to amortize intangible assets such as trademarks for companies they acquired. In other words, you amortize an intangible asset mostly due to accounting rules, and that doesn’t really follow the economics of how trademarks work for example. There is another process, where intangible assets that lose all of their value are written off as an impairment, which is when it may make sense to adjust earnings for those events. Anyways, Johnson & Johnson is expected to earn an adjusted $8.53-$8.63 per share in 2019, which is up from $8.18 adjusted EPS in 2018. Adjusted earnings guidance excludes the impact of after-tax intangible amortization expense and special items.

Johnson & Johnson has a diversified product line across medical devices, consumer products and drugs, which should serve it well in the future. This makes the company somewhat immune from economic cycles. Investors looking fora safe and dependable earnings can look no further than Johnson & Johnson. In addition, the company has strong competitive advantages due to its scale, leadership role in various diverse healthcare segments, breadth of product offerings in its global distribution channels, continued investment in R&D, high switching costs to users of its medical devices, as well as its stable financial position.

Future profits growth could come from new product offerings, which are the result of continued investment in research and development, and through strategic acquisitions.

Recently, shares have been hit hard by an article claiming the company knew that its baby powder contained traces of asbestos, which is then linked to cancer. The company denies the fact that its ingredient talc contains traces of asbestos and denies that its product causes cancer. I believe that this negative news can provide an opportunity to add to this quality company at lower prices. If it drags on, long-term investors may be able to purchase more shares at even lower prices.

Another high profile case is linking Johnson & Johnson to the nation’s opioid epidemic. It is possible that the two high-profile cases listed above may offer steeper drops in share prices, which may provide long-term investors with good entry points.

Johnson & Johnson has managed to reduce number of shares outstanding over the past decade, which helped earnings per share growth. Between 2007 and 2018, the number of shares declined from 2,911 million to 2,728 million. The short bumps up were related to acquisitions. JNJ unveiled a 5 billion dollar share buyback in December, as a way to show confidence and reassure investors after recent cancer allegations on its baby powder.

The company managed to grow its dividends by 7.40%/year over the past decade. The company's latest dividend increase was announced in April 2019 when the Board of Directors approved a 5.60% increase in the quarterly dividend to 95 cents /share.

The dividend payout ratio has increased from 45% in 2007 to 50% in 2018. The ability to generate strong cash flows, have enabled Johnson & Johnson to reward shareholders with a higher dividends for 57 consecutive years. I believe that the dividend is safe today, but will likely be limited to future growth in earnings per share of 5% - 6%/year over the next decade. A lower payout is always a plus, since it leaves room for consistent dividend growth and minimize the impact of short-term fluctuations in earnings.

Currently, the stock is attractively valued at 15.90 times forward earnings, yields 2.90% and has a forward dividend payout ratio of 44%.