Danger Zone: Tuesday Morning (TUES)

Discount retailer Tuesday Morning (TUES: $16/share) is in the Danger Zone this week. Brick and mortar stores continue to struggle against the onslaught of online retailers, and TUES is not positioned well to meet this challenge. With no online store, inferior operational metrics to its peers, and an ill-defined target market, TUES should struggle just to stay afloat. Add in an expensive valuation, and this is one stock investors should steer clear of.

Declining Profitability

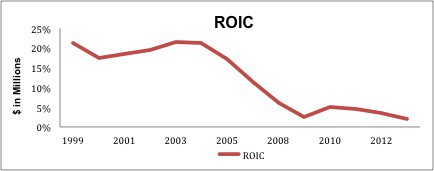

Online retailers have already taken their toll on TUES. Return on invested capital (ROIC) has declined for the past three years, from 5% to 2%. It’s hard to believe that only a decade ago this company earned a 21% ROIC. Figure 1 shows just how steep this decline has been.

Figure 1: ROIC in Decline

Sources: New Constructs, LLC and company filings

Most of the drop in ROIC comes from the decline in TUES’s after-tax profit (NOPAT) margins, which dropped from 2.5% in 2010 to 1% in 2013. The apparent increase in TUES’s margins for the first two quarters of 2014 is illusory. A $42 million write down was included in TUES cost of sales for 2013, which artificially decreased its gross margin for that year. Removing the effect of this write down, we see that TUES’s gross margin actually has continued to decline from 36% in 2013 to 35% for the first six months of 2014.

At the Bottom of Its Industry

TUES lags behind its industry peers in almost every category. Among discount retailers, TUES ranks dead last in terms of bothROIC and NOPAT margin. Expand that group to all multiline retailers, and only Sears (SHLD) and JC Penney (JCP) rank behind TUES. Those are not companies anyone wants to be compared to right now.

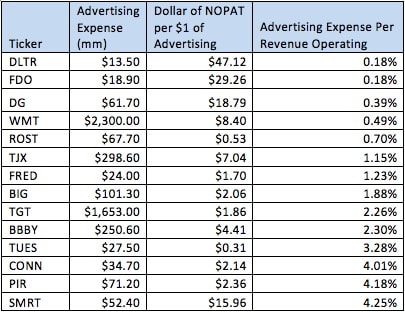

As we dig deeper into TUES’s numbers, they look worse. TUES spends 3.3% of its revenue on advertising, proportionally more than almost any of its competitors. However, it gets back only ~$0.30 of NOPAT for every dollar it spends on advertising. That’s a poor return. By comparison, competitor Pier 1 Imports (PIR), which spends slightly more on advertising, earns ~$2.40 of NOPAT for every dollar it spends. Figure 2 shows the breakdown TUES and its competitors. Note that TUES has the very worst return in terms of NOPAT per dollar spent on advertising.

Figure 2: Advertising Efficiency

Sources: New Constructs, LLC and company filings

TUES also ranks at or near the bottom of its industry in metrics like inventory turnover, gross margin, and revenue growth. TUES is struggling to keep up with its competition, and it’s not hard to see why.

Corporate Strategy is Poor

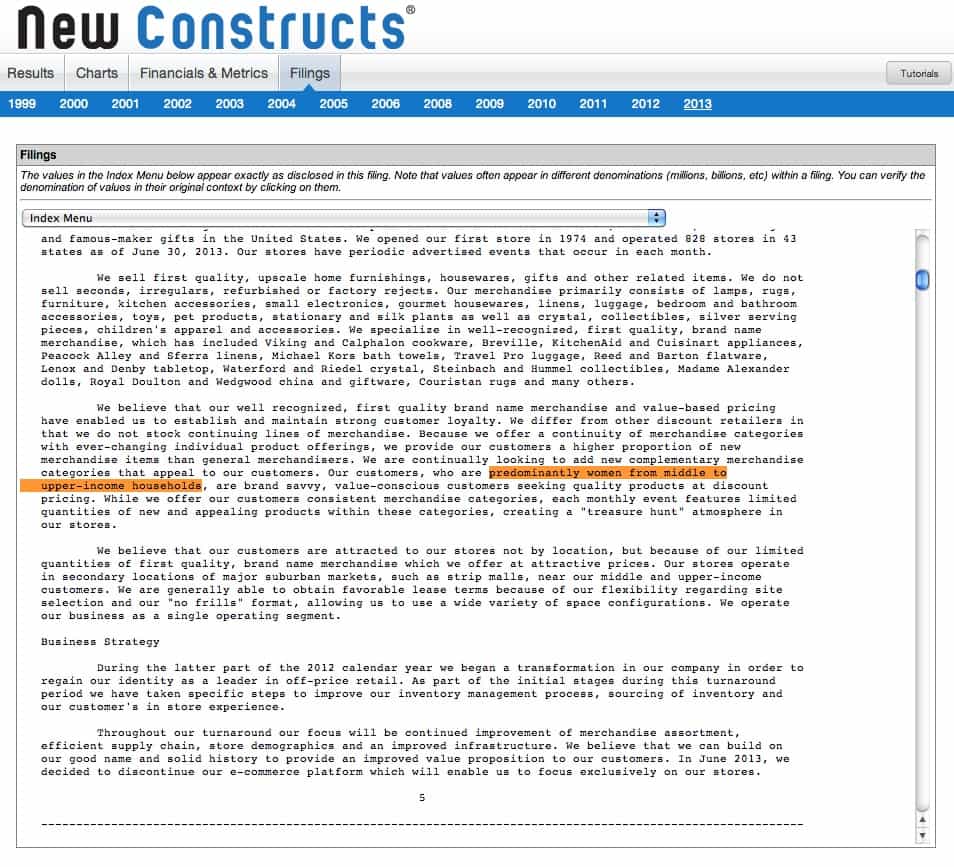

There seems to be a fundamental disconnect between the company’s expressed strategy and the condition of its stores. TUES describes its customers as “predominantly women from middle to upper-income households.” One would expect that a store pursuing middle to upper-income shoppers would try to create an appealing, upscale experience, but that does not seem to be the case. Seeking Alpha contributor Retail Maven wrote of the stores: “Tuesday Morning stores are disorganized; merchandise poorly is displayed; packaging is tattered; and the stores are staffed by inexpert personnel.” One of our own analysts visited stores in the area and came to the same conclusion, adding that they look more like Goodwill than a Home Goods (TJX) or Pier 1 store.

TUES seems to be focusing its efforts to compete based on price, and while its prices are lower than some of its competitors, competing on price against the Amazons (AMZN) and Wal-Mart’s (WMT) of the world is a poor strategy when you cannot match their scale or cost advantages. If TUES cannot offer a quality customer experience in its stores, we are left to wonder why they expect to be in business.

Moreover, TUES doesn’t have an online offering to compete with online retailers. It tried e-commerce for a while, but they shut down their online store in June of 2013 when it only generated just 1% of revenue. The lack of an online store, as well as the 50% decline in visitors to its home website in 2013, put TUES at a disadvantage going forward.

Bulls see opportunity for TUES to get more aggressive on pricing and redo store layouts, but the opportunity here is overstated. TUES’s margins are so thin that it’s hard to see how they can go lower with prices. With no excess cash and ~$160 million (24% of market cap) in adjusted total debt, I don’t think they have the resources to attempt a major store overhaul.

Turnaround Is Already Priced In to the Stock

The final nail in TUES’s coffin is the fact that, even if the company does manage the turnaround that bulls are hoping for, that growth is already priced into the stock. Up 93% in the past year, TUES has more than overshot its fair valuation.

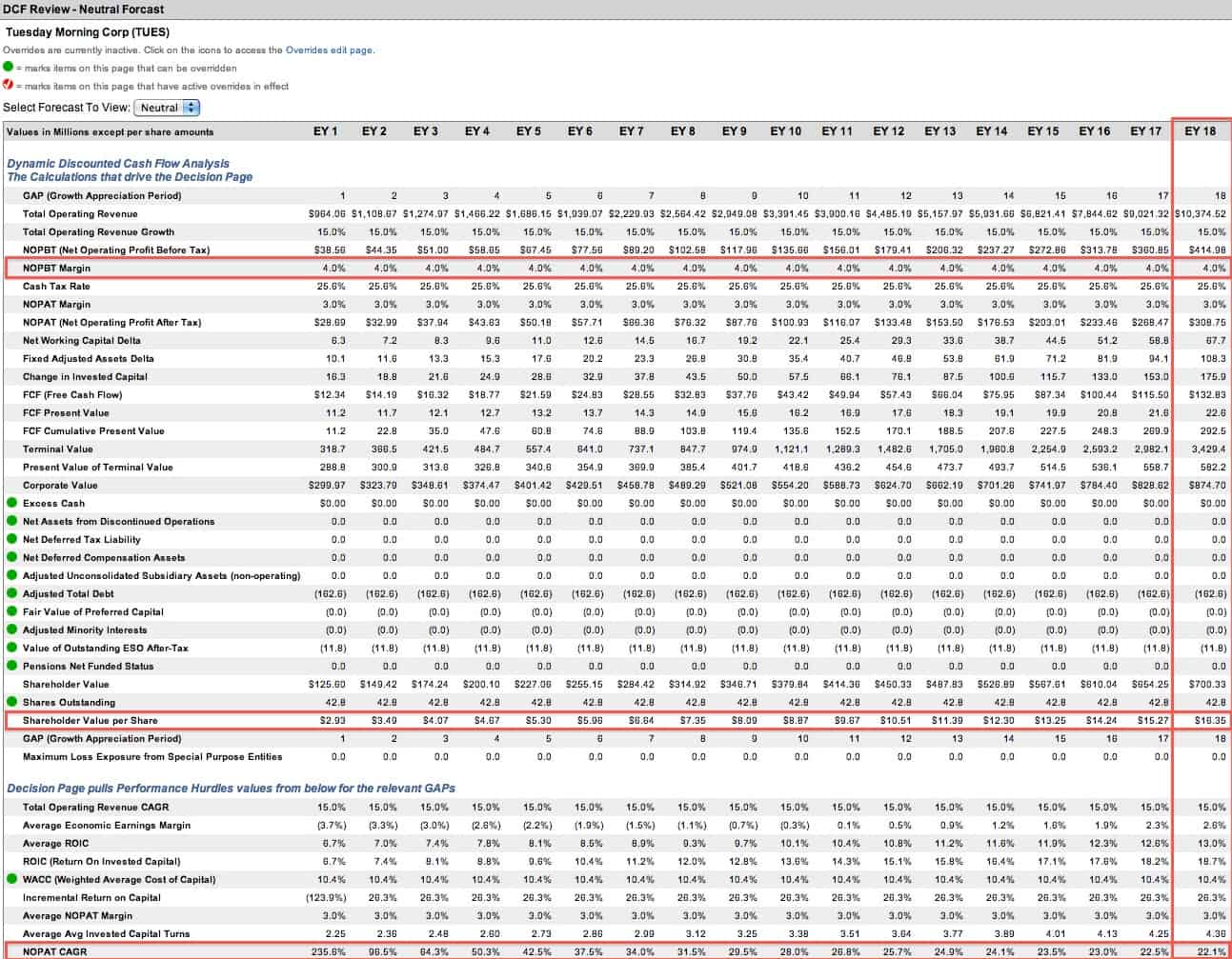

TUES’s valuation of ~$16/share implies that the company’s pre-tax margins will nearly triple starting this year and that it willgrow NOPAT by 22% compounded annually for 18 years. Even the most ardent bull wouldn’t argue that TUES is capable of that kind of growth.

There are a number of issues lurking that could send this stock back down. The poor liquidity position was mentioned above, but of even greater concern is the high turnover in executive leadership. TUES has had four CEO’s in the past two years, and one of those former CEO’s, Kathleen Mason, sued the company for discrimination. Further turnover in executive positions could have a negative effect on the stock as poor leadership only gets worse.

More write-downs like the $44 million inventory write down last year could also send the stock downward as investors finally tire of seeing value destruction instead of value creation.

Expectations of a turnaround are so high that any further setbacks should cause the stock to drop significantly.

Any brick and mortar retailer carries some risk in this environment, but investors who really want exposure to this sector should look for higher quality companies than TUES. Other retailers have superior profitability metrics, better branding and e-commerce capabilities, and a cheaper valuation. The only reason to touch TUES is to short it.

Feature Photo Credit: Nicholas Eckhart (Flickr)

David Trainer, Sam McBride, and German Perez-Vargas receive no compensation to write about any specific stock, sector, or theme.

{kind=link}

{kind=link}