Classic Banking Doesn’t Pay Off – TD And CIBC Q3 2020 Earnings Review

After reviewing Q3 2020 earnings for BMO and ScotiaBank, and then for National Bank and Royal Bank, it is time to look at what TD and CIBC had for us in their pockets.

Oh my, this is definitely not my best picture… but I did it on purpose mostly because TD and CIBC Q3 earnings have not been really exciting, to say the least. And this is exactly the kind of goofy faces I do when I’m bored.

I’ll tell you upfront, TD, and CIBC are not my favorites mostly because they are more targeted to classic banking, savings and loans. TD is doing well, CIBC not so much.

The Toronto-Dominion Bank (TD) (TD.TO)

Business Model

TD is the second largest Canadian bank by market cap and is often jockeying side-by-side for the 1st position with Royal Bank (RY). TD is the most classic bank in Canada with its business model focusing a lot on retail banking. Its portfolio is well diversified between Canada (61%) and the U.S. (30%). TD operates three business segments: Canadian retail banking, U.S. retail banking, and wholesale banking. The bank’s U.S. operations span from Maine to Florida, with a strong presence in the Northeast. It also has a 42% ownership stake in TD Ameritrade, a discount brokerage.

What’s the Story?

“TD colleagues around the world continued to deliver for our customers, clients, and each other throughout a period of unprecedented disruption. As economies across our footprint begin to re-open, the wellbeing and safety of our customers, colleagues and communities remains a top priority,” said Bharat Masrani, Group President and CEO, TD Bank Group.

Source: TD Press release

In the second part of his statement, TD CEO mentions their position of strength, their prudency, their good capital, and their strong liquidity.

To be honest, I’m pretty sure that they’re going to do well. They experienced good volume growth and properly managed credit provision. Overall, we got the same comments we had from Royal Bank and National Bank.

Now let’s dig into the numbers.

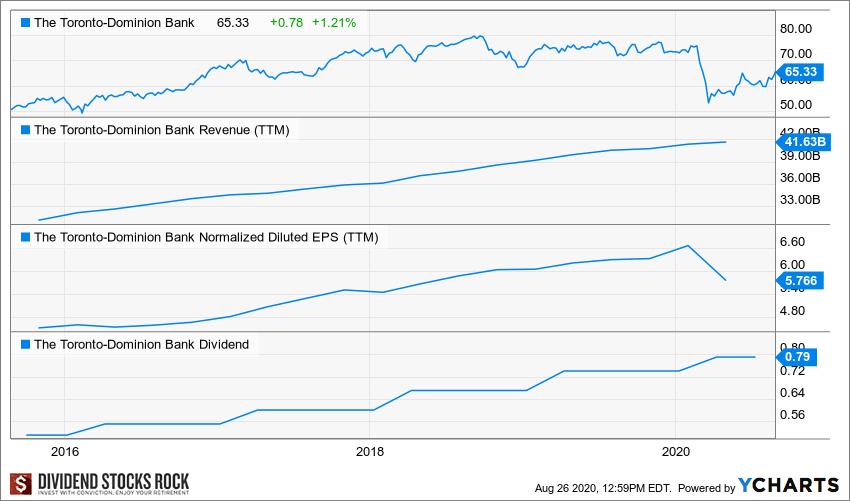

- Net income $2.3B, -30%

- Adjusted EPS $1.25, -30%

- CET ratio is at 12.5 (12 in 2019)

As it’s the case for most banks, net income earnings are down mostly because of the huge credit provision for credit losses ($2B). While it was at $3.2B in April, last year was at $655 million. This quite a number to digest for such business!

I’m impressed by their common equity tier 1 capital ratio, the highest of all banks. As it was at 12% last year, TD managed to improve it even during a recession.

TD shows that 7.4% of its loan portfolio is highly at risk due to COVID-19m which is similar to RBC with 7.1. While this is normal, their US exposure hurts. The US retail worth was down 64%, so that didn’t help.

On the other hand, the wholesale segment (about $400 million in earnings) was up by 81%.

Investment Thesis

A stronger economy from both countries led to TD’s stronger results between 2010 and 2020. TD keeps things clean and simple as the bulk of its income comes from personal and commercial banking. It has a large exposition in major cities like Toronto, Vancouver, Edmonton and Calgary, combined with a strong presence in the US. With about a third of its business coming from the U.S., TD is the most “American Bank” you’ll find on this side of the border. If you are looking for an investment in a straightforward bank, TD should be your pick. This bank is a good example of a perfect dividend triangle. Unfortunately, the pandemic will affect this triangle and you will have to wait until 2021 to see another dividend increase. Nonetheless, TD is a strong bank.

Potential Risks

The housing market has been a concern since 2012, but TD seems to be managing its loan book wisely. The Canadian economy has been remarkably resilient too. A higher insured mortgage level in the prairies seems adequate while TD continues to ride the ever-growing downtown Toronto housing market. Keep in mind that a housing bubble is always just around the corner. Now that interest rates have been cut by the Central Bank of Canada, it will be difficult for classic banks such as TD to thrive. The interest rate margin is narrowing. The green bank will have to find other growth vectors to please investors. Follow the bank’s provision for credit losses quarter to quarter during the pandemic.

Dividend Growth Perspective

TD is a Canadian dividend aristocrat (which permits a “pause” in the dividend increase streak). Management prefers to increase the dividend once a year and did so with a 12% increase in 2018 and a 10% increase in early 2019. However, management has been more prudent in early 2020 with just a 6.7% increase. Shareholders can expect a mid single-digit dividend growth going forward, but will have to wait until 2021 to see if the economy permits a raise. We expect Canadian banks to pause their dividend increases until the situation around COVID-19 is clearer.

Canadian Imperial Bank – CIBC (CM) (CM.TO)

Business Model

CIBC is a global financial institution that provides a range of financial products and services to approximately 11 million individuals, small business, commercial, corporate and institutional clients in Canada and around the world. CIBC operates through three segments: Retail and Business Banking, Wealth Management and Capital Markets. CM shows a more “classic” approach than its peers.

What’s the Story?

“We delivered solid financial results in the third quarter as our team maintained a tireless focus on our clients, helping make their ambitions a reality during a period of disruption for many,” said Victor G. Dodig, CIBC President and Chief Executive Officer. “The continued execution of our strategy and ongoing investments in our business, as well as disciplined expense management, have contributed to our resilience and positioned us well for the evolving macroeconomic environment. Our entire team is engaged and committed to supporting our clients and communities.”

Source: CIBC Press Release

What a boring comment! Basically, they state their solid financial results (which I believe were just okay). Maybe the problem comes from the fact we’re facing an oligopoly Canadian banks. The entire market or so is controlled by the big five.

That being said, CIBC is basically in the same situation as the other banks: business as usual. And this is one of the reasons why I tell investors that having four, five, six banks in their portfolio ends up in duplicating the same asset.

Now let’s dig into the numbers.

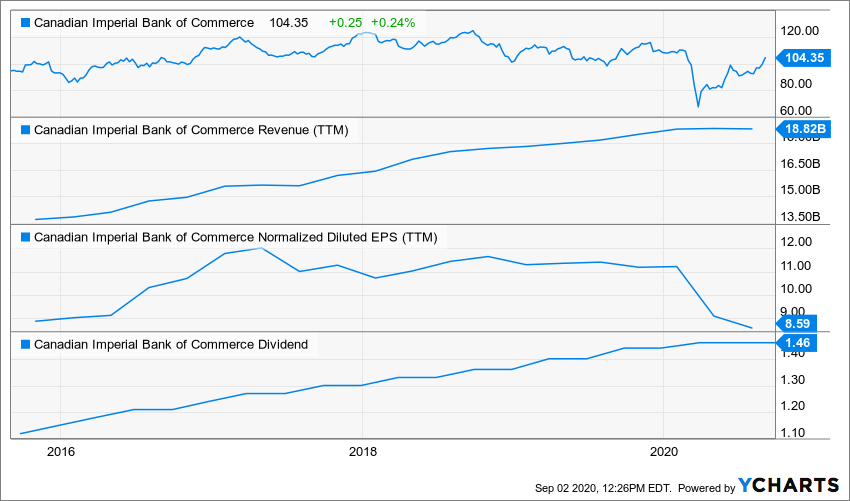

- Net income $1.24B, -12%

- Adjusted EPS $2.71, -13%

- CET ratio is at 11.8 (+40 points)

CIBC is healthy, they did a good assessment with their provision for credit loss, $525M, from $291M last year, but a lot lower than in April.

The bank has 11% of its portfolio in commercial real estate but its not telling you exactly which type of loans is at risk due to COVID-19. We know that they have 1% in auto lending, 1% in leisure entertainment and 2% in gas. We can therefore assume they’re in-line with the other banks with 5%-7% of their loans portfolio considered at risk.

While earnings are down, there’s nothing to worry about. What I want to highlight is that classic banking model doesn’t seem to pay off right now. I don’t expect it to pay off in 2021 as well. Canadian personal business is down 23%, Canadian commercial and wealth management minus 7% and then US commercial and wealth management is down 58%. Fortunately, they have a good portion of capital markets (up 67%)!

CIBS might not be the best in class but it’s not the worst either. Overall, it’s a very solid bank with a very generous and safe yield. The bank could fit very well in an income seeking portfolio. At the same time, CIBC looks limited in terms of stock appreciation and could be considered as a deluxe bond.

Investment Thesis

While CIBC lags behind the other banks on the stock market, it gives investors the opportunity to pick a 5+% yield without much risk. We like its idea to grow through its wealth management division, but the integration of Private Bank will represent a crucial step. If you are looking for additional income, CM is probably one of the best picks on the Canadian stock market, but don’t expect the stock to soar. CIBC is trading at a low PE ratio compared to its peers. The reason is simple: less growth perspective. At least the dividend is not at risk, and you will enjoy consistent paycheck raises.

Potential Risks

Put in easy words, ask your 5-year-old to choose a Canadian bank based on its logo and you get a good investment… if it’s not CIBC! The bank is one of the worst in terms of returns over the past 5 and 10 years, and is also the one with the least growth vectors. Its heavy concentration in the mortgage business could hurt CM results in the upcoming years as the housing market seems to reach a plateau and regulation tighten mortgage rules. Considering the unknown impact on the virus on the economy, we would rather go with larger banks such as Royal or TD.

Dividend Growth Perspective

CIBC is the most generous Canadian banks in term of yield. This is mostly because the bank trades at a lower earnings multiple compared to its peers. The bank has shown a steady mid-single digit dividend growth for many years. To me, CIBC may be a good choice if you look for income and treat it more like a “deluxe bond”. The dividend is safe right now, but we don’t expect any banks to increase their dividend in 2020 as we will go through an important recession.

Final Thoughts

Again, I believe Canadian banks’ dividends are safe. If you’re not a shareholder yet, you should consider adding one (not all)! Canadian banks are very strong and should continue to grow their dividend once the economy settles down.

As for TD and CIBC, we have a decent payout ratio and a robust balance sheet for both. They remain solid and healthy. However, they are less creative than their peers and show less growth vectors. Not to mention that classic banking is hurt more by the current recession. This is why I find them less attractive and prefer National Bank or Royal Bank.

Disclaimer: I do not hold shares of TD or CM.

Each month, we do a review of a specific industry at our membership website; Dividend Stocks Rock. In addition to have full access to 12 real-life ...

more