Twilio (TWLO) shares have been beaten down the last few years but it's still growing its business. This Zacks Rank #1 (Strong Buy) is expected to grow earnings by 31% this year.

Twilio operates a Customer Engagement Platform (CEP) that allows companies to build direct, personalized relationships with their customers worldwide. It covers sales to marketing to growth.

It operates across 180 countries and territories and, as of June 30, 2024, had 316,000 active customer accounts.

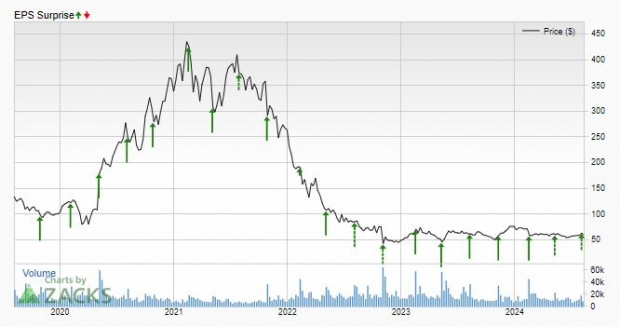

Another Beat by Twilio in the Second Quarter

On Aug 1, 2024, Twilio reported its second quarter results and beat on the Zacks Consensus by $0.16. Earnings were $0.87 versus the consensus of $0.71.

It was yet another earnings beat in an otherwise stellar earnings surprise track record. Twilio hasn't missed in 5 years and has put together large beats the last few years.

Image Source: Zacks Investment Research

Twilio saw a record quarter of revenue, up 4% year-over-year to $1.08 billion, with organic revenue growth of 7%. Communications revenue, the largest business unit, was up 4% to $1.01 billion, while Segment revenue was up 3% year-over-year to $75.2 million.

Free cash flow was $197.6 million, up from $71.9 million a year ago.

Twilio Raised Full Year Guidance

In response to the strong quarter, Twilio raised its non-GAAP income from operations range for the year to $650 - $675 million, up from $585 - $635 million previously.

It expects free cash flow to be in line with its full year 2024 non-GAAP income from operations. But it did narrow its full year 2024 organic revenue growth guidance to a range of 6% to 7% from is prior guidance of 5% to 10%.

As a result of the bullishness, analysts also raised their 2024 earnings estimates. 4 were higher after the earnings report, which pushed the Zacks Consensus up to $3.22 from $3.12.

That is earnings growth of 31.4% as Twilio only made $2.45 last year.

Analysts also expect another 12.2% earnings growth in 2025.

Image Source: Zacks Investment Research

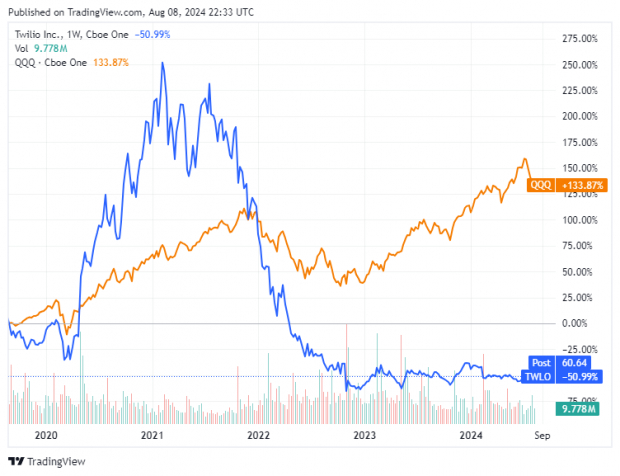

Is Twilio a Value Stock Now?

Twilio shares have gone nowhere the last 5 years. They're down over 50% during that time frame.

(Click on image to enlarge)

Image Source: Zacks Investment Research

Even in 2024, shares remain weak, down 20.1%.

Twilio has also gotten cheap. It trades with a forward price-to-earnings ratio (P/E) of just 18.3.

And as earnings rise, it now has an attractive PEG ratio, which measures the P/E ratio over the growth rate. The PEG ratio is just 0.6. A PEG ratio under 1.0 indicates a stock has both growth and value.

What is it doing with all that free cash flow?

Twilio has a big share buyback program. Originally a $1 billion program authorized in Feb 2023, the board authorized an additional $2 billion in Mar 2024.

Twilio has completed over $2.2 billion of the repurchases and expects to complete the remaining $0.8 billion left on the $3 billion authorization before the end of 2024.

For those looking for cheap growth, Twilio should be on your short list.

More By This Author:

Bear of the Day: Hooker Furnishings (HOFT)

How To Invest In Small Cap Value Stocks In 2024

Stocks At 52-Week Lows: Values Or Traps?

Comments

Log in or sign up to join the conversation.