KB Home (KBH) continues to see strong demand for new homes and is able to navigate supply chain challenges heading into 2022. This stock is expected to grow earnings by another 49% this year.

KB Home is one of the largest home builders in the country with homes in 47 markets from coast-to-coast.

Photo by Hans Eiskonen on Unsplash

Another Earnings Beat in the Fourth Quarter of 2021

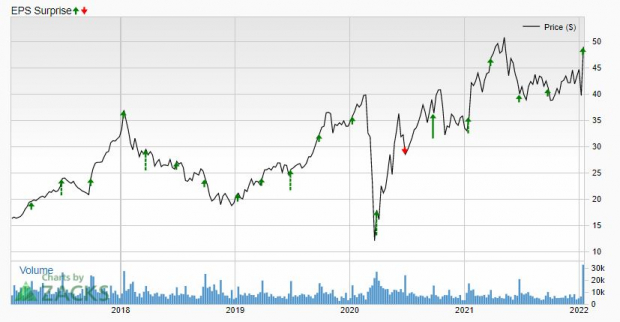

On Jan 12, KB Home reported its fourth quarter 2021 results and blew by the Zacks Consensus Estimate by $0.14.

Earnings were $1.91 versus the Zacks Consensus Estimate of $1.77. It was the 6th earnings meet or beat in a row.

But KB Home has a great track record of beating, with just one miss in the last 5 years and it was when the pandemic first broke out, which sent the home building industry into an initial spiral.

That initial hit on business quickly faded as demand returned with buyers even buying remotely after touring homes online. It has been red hot ever since.

(Click on image to enlarge)

Image Source: Zacks Investment Research

Revenue in the fourth quarter was up 40% to $1.68 billion as homes delivered jumped 28% to 3,679.

KB Home continued to have pricing power as demand remained strong with average selling price increasing 9% to $451,100.

Gross profit margin increased 230 basis points to 22.3%. Excluding inventory-related charges, the housing gross profit margin improved to 22.4% from 21%.

The improvement in gross profit margin was achieved through a favorable pricing environment due to strong demand and the limited supply of available homes for sale, and lower relative amortization of previously capitalized interest, partly offset by higher construction costs, particularly elevated lumber prices.

Ending backlog value jumped 67% to $4.95 billion as supply chain issues for things like garage doors and appliances have increased delivery times.

It was KB Home's highest fourth quarter backlog level since 2005. Each of the company's four regions generated increases which ranged from 53% in the West Coast to 106% in the red hot Southeast.

Total homes in the backlog rose 35% to 10,544.

For the year, revenue rose 37% to $5.72 billion as Americans moved during the pandemic and many wanted new homes.

Bullish on 2022

Despite Wall Street believing the demand for homes is "over" after a blistering 2-year period, KB Home said on its conference call that it believes demand will be strong again in 2022, as existing home inventory remains low and Millennials, the largest generation in American history, continues to buy homes.

KB Home's 2022 guidance was bullish.

It's looking for another big jump in revenue, in the range of $7.2 billion to $7.6 billion as the average selling price continues to move higher, in the range of $480,000 to $490,000.

KB Home said on the conference call that it wasn't worried about higher mortgage rates dampening demand.

Even with inflationary pressures and lumber prices on the move higher again, housing gross profit margin is expected in the range of 25.4% to 26.2% for the year.

Analysts Raise Earnings Estimates for F2022 and F2023

The analysts were equally as bullish as 3 estimates were raised for fiscal 2022 and one for fiscal 2023 since the earnings report.

The fiscal 2022 Zacks Consensus Estimate jumped to $9.03 from $7.88 in the last week. That's earnings growth of 49.3% as KB Home made $6.05 last year.

Fiscal 2023 also jumped to $11.04 from $8.87 over the last 7 days. That's further earnings growth of 22.2%.

Shares are Dirt Cheap

Shares of KB Home jumped 19.4% in the last week on the earnings report and are up 37.1% over the last year.

However, they haven't yet taken out the spring 2021 highs.

(Click on image to enlarge)

Image Source: Zacks Investment Research

Over the last 2-years, shares of KB Home have lagged the S&P 500, with KBH gaining 33.2% versus the S&P 500's gain of 57.7% during that time.

They remain dirt cheap with a forward P/E of just 5.4.

And with the expected earnings growth, KB Home has a PEG ratio of just 0.3.

Shareholders also get a dividend, currently yielding 1.2%.

Why Aren't the Shares Soaring?

The Street is worried about rising rates and "peak" earnings. Over the last year, they've been wrong.

For investors looking for a value stock with rising earnings estimates, KB Home is one to keep on the short list.

Comments

Log in or sign up to join the conversation.