ACM Research (ACMR) , a Zacks Rank #1 (Strong Buy), develops cleaning equipment that assists semiconductor companies in removing particles, contaminants, and other random defects during the manufacturing process. ACMR shares are widely outperforming the market this year with the backing of a leading industry group. The stock is hitting a series of 52-week highs and displaying relative strength as buying pressure accumulates in this market leader.

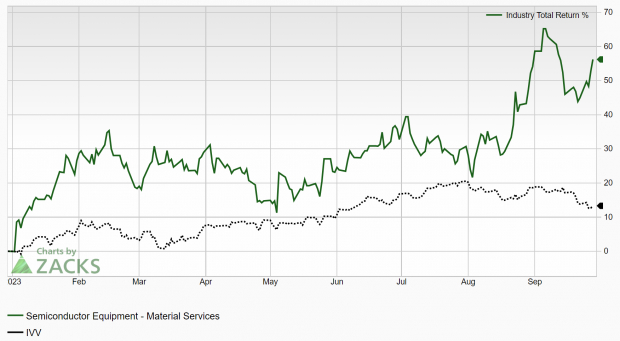

The technology company is part of the Zacks Semiconductor Equipment – Material Services industry group, which ranks in the top 1% out of more than 250 Zacks Ranked Industries. Because it is ranked in the top half of all Zacks Ranked Industries, we expect this group to outperform the market over the next 3 to 6 months. This industry has been steadily outperforming the market in 2023:

(Click on image to enlarge)

Image Source: Zacks Investment Research

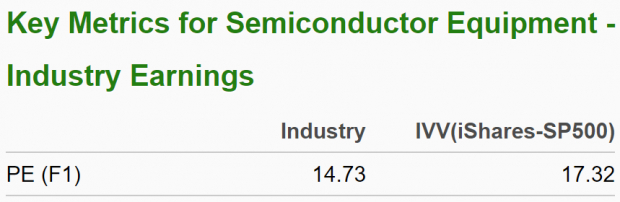

Also note the favorable characteristics for this group below:

(Click on image to enlarge)

![]()

Image Source: Zacks Investment Research

Historical research studies suggest that approximately half of a stock’s price appreciation is due to its industry grouping. In fact, the top 50% of Zacks Ranked Industries outperforms the bottom 50% by a factor of more than 2 to 1. It’s no secret that investing in stocks that are part of leading industry groups can give us a leg up relative to the market. By focusing on leading stocks within the top 50% of Zacks Ranked Industries, we can dramatically improve our stock-picking success.

Company Description

ACM Research produces and sells single-wafer wet cleaning equipment for enhancing the manufacturing process and yield of integrated semiconductor chips. Its technology delivers megasonic energy at a microscopic level, providing cleaning for 2D and 3D patterned wavers.

The company’s cleaning process uses less sulfuric acid and hydrogen peroxide, providing more efficient performance for advanced metal plating. ACM Research sells its products under the Ultra C brand name through direct sales forces and third-party representatives.

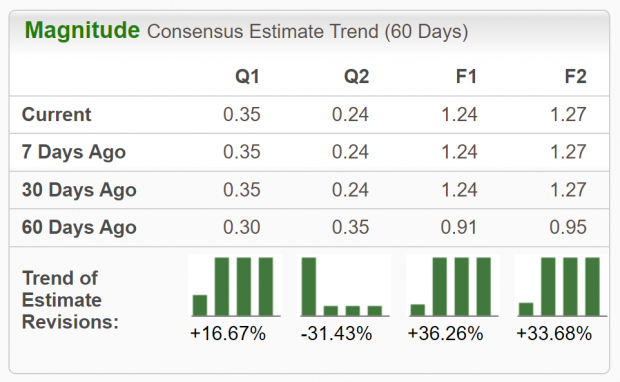

Earnings Trends and Future Estimates

ACMR has built up an impressive earnings history, surpassing earnings estimates in each of the last eight quarters. Back in August, the Fremont, California-based company reported second-quarter earnings of $0.48/share, a staggering 380% surprise over the $0.10/share consensus estimate. Earnings grew 118% year-over-year, while revenues of $144.58 million improved 38.5% from the year-ago quarter. ACMR has delivered a trailing four-quarter average earnings surprise of 210.26%.

Analysts covering ACMR are in agreement and have been increasing their earnings estimates as of late. For the current fiscal year, analysts have increased earnings estimates by 36.26% in the past 60 days. The 2023 Zacks Consensus EPS Estimate now stands at $1.24/share, reflecting potential growth of 49.4% relative to the prior year. Revenues are projected to surge 44.39% to $561.4 million.

(Click on image to enlarge)

Image Source: Zacks Investment Research

Let’s Get Technical

ACMR shares have advanced nearly 135% this year. This is the kind of stock we want to include in our portfolio – one that is trending well and receiving positive earnings estimate revisions.

(Click on image to enlarge)

Image Source: StockCharts

Notice how both the 50-day (blue line) and 200-day (red line) moving averages are sloping up. The stock has been making a series of higher highs. With both strong fundamentals and technicals, ACMR is poised to continue its outperformance.

Empirical research shows a strong correlation between near-term stock movements and trends in earnings estimate revisions. As we know, ACM Research has recently witnessed positive revisions. As long as this trend remains intact (and ACMR continues to deliver earnings beats), the stock will likely continue its bullish run this year.

Bottom Line

The future looks bright for this highly-ranked, leading stock. Momentum has picked up in recent months, even as the general market experienced a pullback.

Backed by a leading industry group and impressive history of earnings beats, it’s not difficult to see why this company is a compelling investment. Robust fundamentals combined with an appealing technical trend certainly justify adding shares to the mix.

More By This Author:

Panasonic (PCRFY) Surges 39.6% YTD: Will the Uptrend Continue?

Carnival (CCL) Q3 Earnings & Revenues Top Estimates, Rise Y/Y

2 Top Ranked Stocks With Sky High Earnings Growth Forecasts

Comments

Log in or sign up to join the conversation.