Banco Santander – A Large Bank Doesn’t Mean A Good One

Summary

- Major changes undergoing for the European bank.

- Recent performance might be too volatile for some investors.

- Digitalization might be the key for SAN to boost its recently slashed revenues.

Banco Santander S.A. (SAN) is a well-known worldwide bank and built its operations since 1857. The Madrid-based company now has a network of branches worldwide, offering them multiple opportunities. While banks are often seen as a solid and somewhat sure investment for a portfolio, dividend-oriented investors really should look twice before going all-in. Pre-2015 figures were certainly more encouraging, since then, volatility seems to have taken over. The company does have some tricks up its sleeves, with their most recent attempt to build a whole new digitalized platform to scoop a wider customer base, growth might get a kick in the next few quarters!

Image by Albert Dezetter from Pixabay

Understanding the Business

SAN started its banking operations in 1857, granting them a good picture of today’s activities. The company built a notorious reputation in some of the biggest banking segments, working in 10 main markets. It is the 1st bank in Europe, deriving 52% of its underlying profit from the region while the remaining 48% comes from the Americas, where they are ranked 3rd. SAN underwent a digital transformation, Openbank, OnePay, and Superdigital to its lineup. In 2018 alone, SAN had 144M customers worldwide, stacking up 34.34B NOI, a 0.1% increase from 2017’s exercise.

Geographically speaking, SAN concentrated 26% in Brazil, 17% in Spain, 13% in the UK and the remaining throughout the world. Employing around 194k workers across their operations, the company now focuses on being the best open financial services platform.

Source: Santander’s website – Economic and financial review

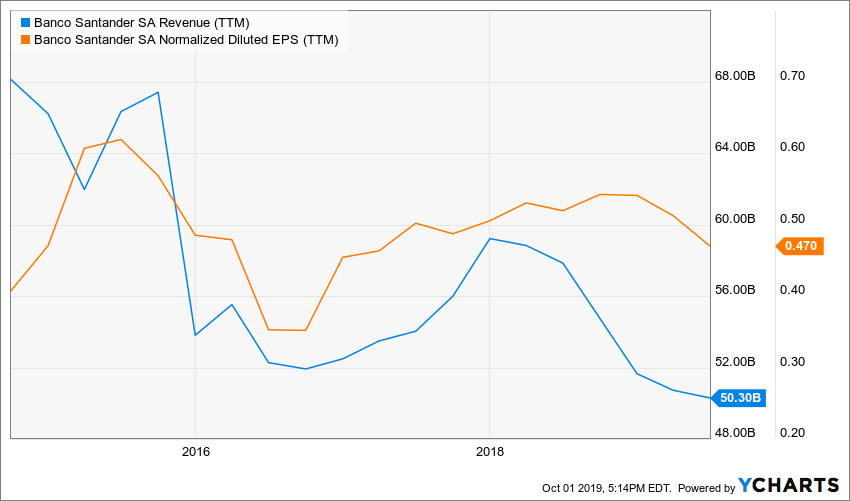

Growth Vectors

Source: YCharts

Sadly enough, banks are also limited on major growth avenues. While there are multiple ways to grow for them, competition often offers the same products with slight changes. Where SAN can get a head start, continuing on what they started these last few years is the digitalization of their operations. With the establishment of Openbank and ODS, global payments services and digital assets, the company could grow its customer base. This unified platform should put them in a favorable position in order to become “the leading Banking as a Service” platform.

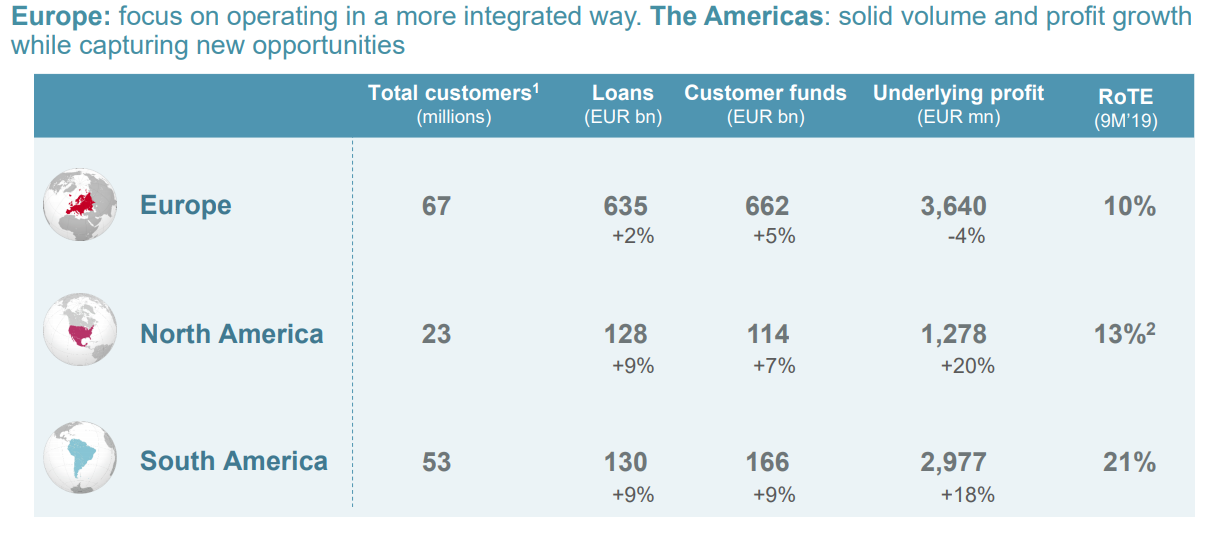

SAN focuses on higher growth prospects such as Brazil and other South America countries. Since the bank does business across the world, it enjoys a more stable stream of income. Using stability to its advantage, it can take higher risks in more volatile markets. When this goes right, the bank makes a lot more money.

Source: Investors presentation

The company is also undergoing organizational structure changes, realigning the company’s mission with Europe, North America, and South America’s segment. Customer retention without a branching network is in the center of their plan.

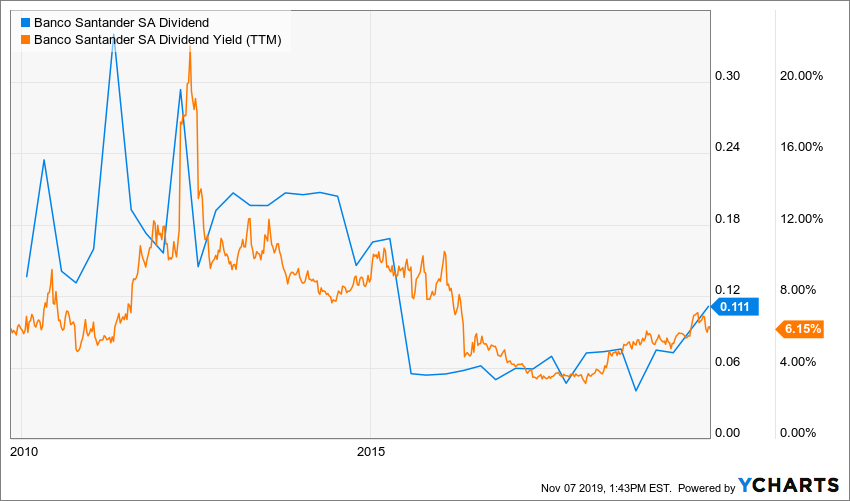

Dividend Growth Perspective

As you can see, the dividend is everything but steady. This is because the bank pays its distribution in Euros and then, we receive it in USD. SAN pays a dividend twice a year (2 different amounts). This explains the seesaw movement.

Source: YCharts

Comparing to its banking peers, SAN is doing decent. Recently recording a ~6-7% yield while the industry average mostly hovers around 2.67%. As mentioned above, dividend stability seems to be an issue, so dividend yield will be volatile. Also, the bank offers a high yield mostly because the stock lost about 50% of its value over the past 5 years. When there is a high yield, there is a red flag.

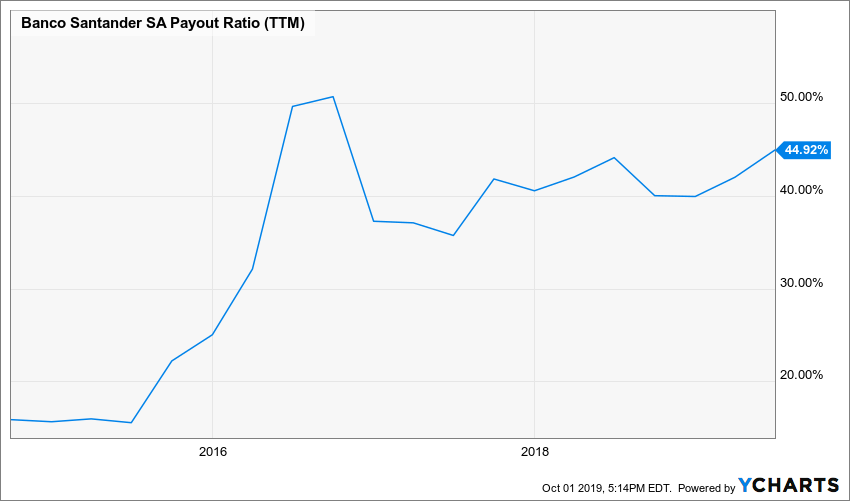

Source : YCharts

On a payout basis, SAN records nearly 45%, meaning almost half of their available earnings are being given back to shareholders. As the figure above shows, late 2015 saw a notable spike, following revenue decline during the same period. Again, stability seems to be missing here for investors to be comfortable.

Potential Downsides

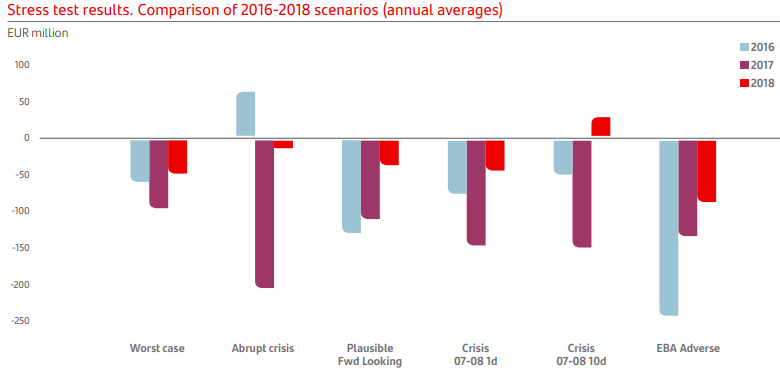

As any financial institutions with major personal loans and mortgages portfolios, credit risk is an inherent operational risk. Credit risk, on a risk-weighted asset base (RWA) racks up an impressive 86% of SAN’s risk. Looking at the figure below, even putting aside an abrupt crisis scenario aside, the company’s balance sheet is looking at solid hits. Although SAN benefits from a healthy sectors diversification, mitigating potential impacts of such events, sectors downturns tend to overlap on others. Squeezing more on liquidities can quickly harm any undergoing growth projects such as acquisition and new product development.

Other operational risks include external frauds, practices with customers and failures in the business channels themselves. While not as prominent as credit-oriented risks, they are not to be taken lightly as a simple data breach can also end up in a costly settlement.

Source: Banco Santander’s 2018 annual report – Risk Management

SAN strong exposure to Latin America is a double-edged sword. If the economy goes well, SAN will thrive. On the other hand, it seems that we are heading towards a bumpy road in those countries. Over the next couple of years, I doubt this exposure will result in growth.

Valuation

Using the Dividend Discount Model (DDM) to give a value to a foreign stock is always a difficult task. Once converted into USD, SAN shows a hectic dividend policy. We have used data from Seeking Alpha ($0.30/year as of November 2019) to start our analysis.

Using conservative numbers, we get a fair value of around $4.50. Considering the hectic payment and the fact there are other great banks with a more stable business model, I don’t see the interest to invest in Santander.

| Input Descriptions for 15-Cell Matrix | INPUTS | |||

| Enter Recent Annual Dividend Payment: | $0.30 | |||

| Enter Expected Dividend Growth Rate Years 1-10: | 3.00% | |||

| Enter Expected Terminal Dividend Growth Rate: | 3.00% | |||

| Enter Discount Rate: | 10.00% | |||

| Discount Rate (Horizontal) | ||||

| Margin of Safety | 9.00% | 10.00% | 11.00% | |

| 20% Premium | $6.18 | $5.30 | $4.64 | |

| 10% Premium | $5.67 | $4.86 | $4.25 | |

| Intrinsic Value | $5.15 | $4.41 | $3.86 | |

| 10% Discount | $4.64 | $3.97 | $3.48 | |

| 20% Discount | $4.12 | $3.53 | $3.09 | |

Please read the Dividend Discount Model limitations to fully understand my calculations.

Final Thought

I understand why income-seeking investors could be interested in SAN. A large bank present in so many countries could have some appeal. Bring a high yield opportunity and you get investors running after this “dividend gem”.

What I see when I look at SAN is a bank taking a bet in undeveloped countries. While this could be a winning strategy, I prefer Canadian banks. In general, they enjoy a more stable business model (due to their oligopoly situation in Canada) while expanding their business in other countries. Plus, they are great dividend growers! What do you think?

Disclosure: We do not hold SAN in our DividendStocksRock portfolios.

Additional disclosure: The opinions and the strategies of the author are not intended to ever be a recommendation to buy or ...

more