About That 'Message' From The Bond Market

After five days of wild, news-driven swings in the stock market, where the action was dominated by escalating trade tensions, the threat of a currency war, and the possibility that the next U.S.-China meeting scheduled for September may not happen, investors can't be blamed for starting the week with some questions. Not the least of which is if the trade war/currency spat could push the world economies into recession - and wind up dragging the U.S. down with them.

On that front, it wasn't at all encouraging to see the UK's economy shrink last quarter. Or the recent German Industrial Production report, which registered the largest annual decline in almost a decade. Or the fact that the OECD's US Composite Leading Indicator fell again in June to the lowest reading since 2009 (Source: Ned Davis Research) and registered its 14th straight monthly decline in the process. Or Goldman's weekend reduction in their outlook for U.S. GDP.

Next on the list of head-scratchers is last week's action by the Central Bankers, which, at the very least, seems to suggest that there is some concern out there.

For example, New Zealand surprised investors with a 50 basis point cut last week, which was twice what economists had expected. India's central bank lowered its rate by an unusual 35 basis points. The Philippine central bank cut on Thursday. And Thailand surprised market participants by cutting their benchmark rate by 25 basis points. This after Jay Powell & Co cut here in the U.S. and Super Mario promised he and his successor, Christine Lagarde, will soon take action on behalf of the ECB.

One and Done? Not Exactly

Here at home, Fed officials are starting to suggest that more action may need to be taken. According to the WSJ, Chicago President Charles Evans said trade and other global developments "have perhaps created more headwinds... and it would be reasonable to do more."

Look At Those Bonds!

And then there is the action in the global bond market. Apparently, this little "skirmish" between the U.S. and China, which has been going on for more than a year and a half now, is creating what is referred to as a "flight to quality." Or, maybe more appropriately in this case, a flight to your local government's bond market.

How else does one explain the yield on Portugal's 10-year at 0.16%? Or Ireland's 10-year dipping below zero, or Spain's 10-year at 0.13%? (And lest we forget, these three countries were all part of the infamous "PIIGS" that were responsible for much of the European debt crises a few years back.)

Looking at more stable economic environs, the yield on Germany's 10-year bund is trading at -0.594% this morning. France's yield hit -0.35% last week. Japan's 10-year is -0.221% today. And for those of you keeping score at home, Deutsche Bank tells us that the total amount of government bonds now trading with negative yields around the globe has ballooned to $15 trillion, which is about double the amount seen last fall.

Here in the U.S., the yield on the 10-year has plunged 1.56% since October (which is a decline of a cool 48.2%). Oh, and the yield curve is inverted. Super.

The "message" being taken from all of this is the global bond markets are screaming for attention. That something is wrong. And that the game is going to end badly for investors, ala a 2008-style collapse. Or so say our furry friends in the bear camp.

Those seeing the investing landscape's glass as at least half empty contend that the U.S. stock market has lost touch with reality and has no justification for the current levels. Ugh.

Maybe Don't Jump on the Doom & Gloom Train Just Yet

But before you run out and starting digging a hole in the back yard to bury your cash in or start loading up on those inverse ETFs, I'd like to offer up a at least a couple alternative scenarios regarding the current "message" from the bond market.

There can be no denying that an inverted yield curve and plunging yields should get your attention. However, I'm of the mind that old fashioned "money flows" are also at work here - in a pretty big way.

First of all, consider that we invest in a global world now. So, we have to think about the financial system on a global scale. And the bottom line is that I, for one, see a global chase for yields going on. Remember, money tends to go where it is treated best - especially during times of stress, fear, and/or crisis.

While I don't believe the current trade war has created a crisis state, it is pretty obvious that there is some "flight to safety" happening here. So, if you are a global investor, where do you stash your money? In Germany, with a guaranteed annual loss of 0.6% or the U.S. 10-year at 1.66%. Not much of a decision, right?

Shaking Hands With The Government

Next up is the old bond trading play, which suggest that when central bankers are easing or playing the QE game, it pays to "shake hands with the government."

From my seat, this helps "explain" at least a portion of the explosion in negative yields around the globe. For example, if the ECB cranks up the QE machine again, investors know there is going to be a buyer of bonds every month - for quite some time. Thus, you want to get in before the central bankers start buying. So, if you bought bonds with a yield of -0.4%, the ongoing demand for the bonds means yields will likely go lower still. And as such, you can expect a gain on your position. As long as somebody with deep pockets has to buy, it is relatively safe to buy here. Crazy, yes. But so goes the game of musical chairs in the bond market.

Forced Buying

Speaking of forced buying, let's also keep in mind that not too long ago, one of the no-brainer macro trades was to short bonds. Remember, yields were going to go higher in the U.S. - perhaps a lot higher. If memory serves, there calls for a 5% T-Bond yield.

And what happens to a short position when prices fall nearly 50%? That's right, margin calls. Forced liquidations. And fund blow-ups. All of which create the buying of bonds.

Although we haven't heard any specific names abruptly closing their doors, it is a pretty safe bet that "forced selling" (or in this case, forced buying to cover short bond positions) has been at work here. This is just what happens when a "no-brainer" macro call goes the wrong way, in a big way.

Then There's TINA

And finally, let's consider the idea of TINA - as in "there is no alternative." Let's keep in mind that if you are a big pension plan or an insurance company, your options regarding what you can invest in are limited. As a manager, you are forced to put money into instruments that might seem overvalued. But, since you really don't have a choice, you just keep buying when new money comes in.

In closing, my primary point on this fine summer morning is that the "message" from the bond market may not be quite as bad as the doom-and-gloomers contend. And while there can be no argument that the action in global bonds is a little nutty right now, something big is going to have to happen to change the current game.

And no, I do not know how this game ends. But for now, at least, it is probably best to follow the money and keep your eyes and ears open.

Weekly Market Model Review

Now let's turn to the weekly review of my favorite indicators and market models...

The State of My Favorite Big-Picture Market Models

It was a wild ride on Wall Street last week as we started with the biggest down day of the year and then enjoyed an impressive rebound Wednesday and Thursday. Through it all there wasn't any change to our Primary Cycle models as the board remains in pretty good shape. As I've been saying, the readings of the Primary Cycle and Fundamental boards suggests that investors should treat pullbacks as buying opportunities.

This week's mean percentage score of my 6 favorite models improved to 71.1% from 70.3%% last week (Prior readings: 84.1%, 79%, 83.9%, 81.1%, 73.5%, 62.9%) while the median also upticked to 70.0% versus 68.4% last week (Prior readings: 86.5%, 80%, 86.7%, 82.5%, 68.5%, 66.3%, 71.3%).

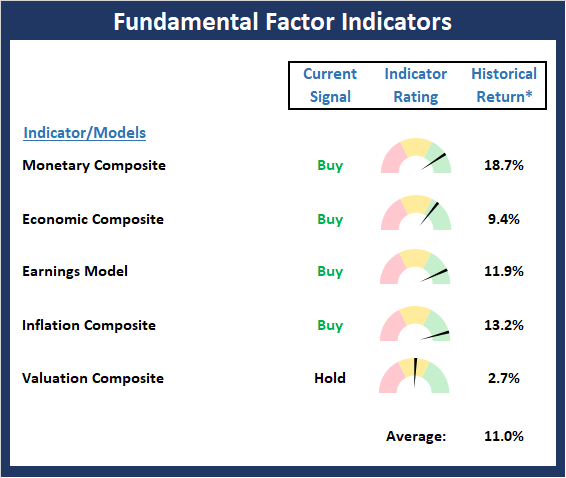

The State of the Fundamental Backdrop

Despite all the market hysterics seen over the past two weeks, there has been no change to the Fundamental board. The bottom line is the big-picture, fundamental backdrop remains positive with historical returns that are above average.

* Source: Ned Davis Research (NDR) as of the date of publication. Historical returns are hypothetical average annual performances calculated by NDR. Past performances do not guarantee future results or profitability - NOT INDIVIDUAL INVESTMENT ADVICE.

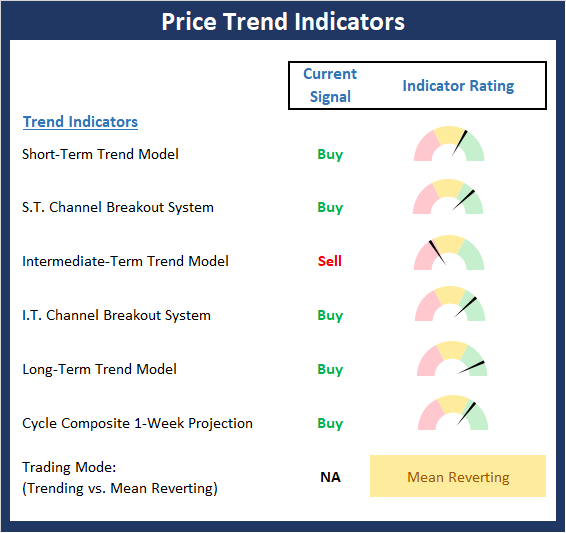

The State of the Trend

Although the headlines tout extreme volatility and fear, our Price Trend board actually improved last week. This is in response to the Short-Term Trend signal perking up, the S.T. Channel Breakout System flashing a buy on Wednesday, and the Cycle Composite pointing higher next week. However, my best guess is we're seeing a bottoming process play out, which means a test of the recent lows is more likely than not. But, I for one, will be looking to add to positions into any further weakness.

* Source: Ned Davis Research (NDR) as of the date of publication. Historical returns are hypothetical average annual performances calculated by NDR. Past performances do not guarantee future results or profitability - NOT INDIVIDUAL INVESTMENT ADVICE.

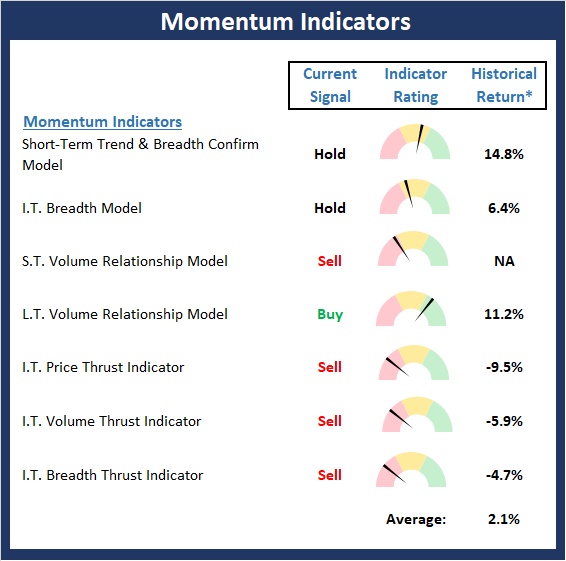

The State of Internal Momentum

If you are looking for reasons to be be cautious on the stock market, the Momentum board is it. While the Short-Term Trend & Breadth Confirm model upticked within the neutral zone last week, the Intermediate-Term model went the other way. In addition, the L.T. Volume Relationship model is sagging and all three Thrust indicators are solidly negative. The good news is that the bulls can rally, most of these ills can be remedied in short order. But for now, this board gives the bear camp the edge in the near-term.

* Source: Ned Davis Research (NDR) as of the date of publication. Historical returns are hypothetical average annual performances calculated by NDR. Past performances do not guarantee future results or profitability - NOT INDIVIDUAL INVESTMENT ADVICE.

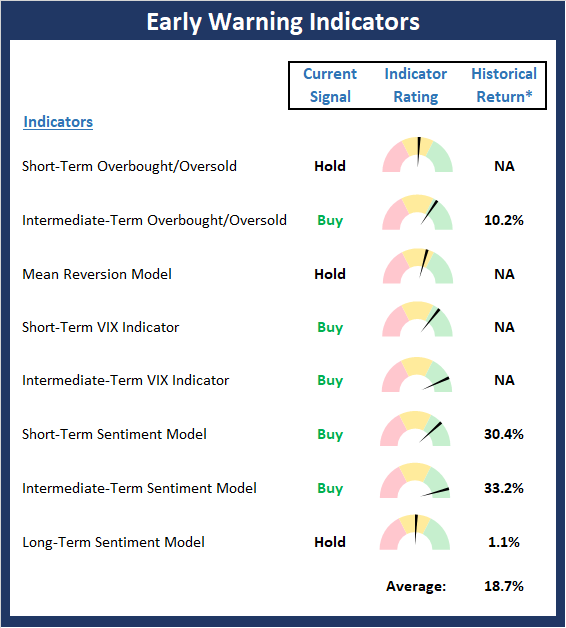

The State of the "Trade"

While I would not classify the current state of the Early Warning Board as a "table pounding" setup, it is clear that the wind is now blowing at the bulls' back. So, unless the bears can push the indices to new lows, we would view any downside testing as an opportunity - especially if the declines are "bought" intraday over a period of a few days.

* Source: Ned Davis Research (NDR) as of the date of publication. Historical returns are hypothetical average annual performances calculated by NDR. Past performances do not guarantee future results or profitability - NOT INDIVIDUAL INVESTMENT ADVICE.

Disclosure: At the time of publication, Mr. Moenning held long positions in the following securities mentioned: none - Note that positions may change at any time.

The opinions and forecasts ...

more