5 Stocks To Watch During This First Peak Week Of Q1 Earnings Season

Banks unofficially kicked off the first quarter 2018 earnings season on Friday with results from JPMorgan, Wells Fargo and Citigroup. All beat due to a combination of volatile Q1 markets, tax reform, interest rate normalization and robust economic growth, but investors weren’t sure how they felt about those numbers, with those stocks initially rising on the news then falling..

Part of Friday’s fluctuations had to do with great expectations that are already baked. We’ve heard for sometime this is going to be the best earnings season in 7 years, so companies are going to have to put up some big beats to get anything out of these reports. Even meeting expectations might have a negative impact on a company’s stock when the stakes are this high. Earnings were always expected to do well as companies have a lot of cash on their balance sheets and the underlying economy is doing well, but the announcement of tax reform in December prompted 75% of S&P 500 companies to boost guidance even higher. Many have come out with detailed plans of how they will spend that money, meaningfully increasing Capex and R&D spending for the first time in years, improving employee 401k benefits and issuing one time bonuses, and increasing share buybacks and dividends.

The S&P 500 index is expected to see EPS grow 17.5% year-over-year (YoY) with revenues increasing 8%, the best numbers since Q2 2011. The sectors driving growth are energy and materials (still due to easy YoY comparisons), followed by financials and information technology, the two largest sectors by market cap. The sector with the lowest expected profit growth rate is consumer discretionary at 6%.

Current index levels and robust earnings expectations for 2018 suggest that stocks are fairly valued, maybe even cheap when adjusting for low interest rates. S&P 500 forward 12-mo P/E hovering around 17x, the 20-year historical average. If we stay at this level is heavily dependent on current earnings expectations being achieved.

5 Stocks to Watch this Week

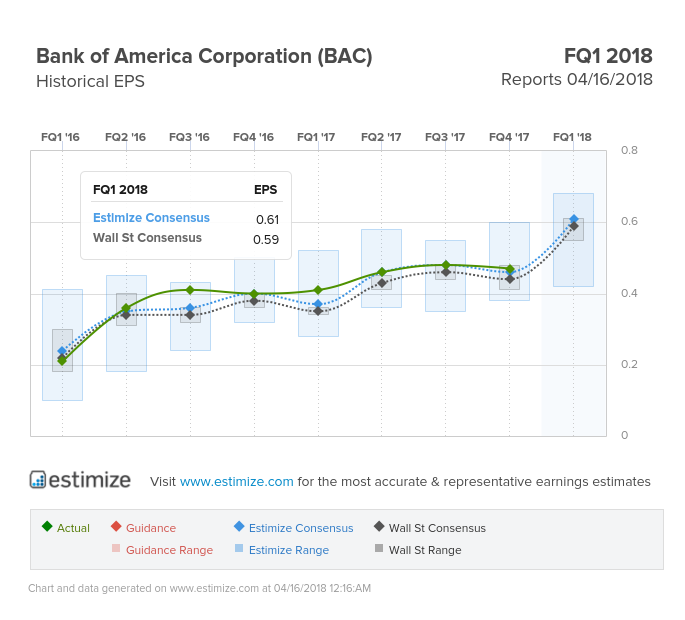

Bank of America (BAC)

Financials - Capitals Markets | Reports April 16, before the open.

The Estimize consensus calls for EPS of $0.61, two cents higher than the Wall Street consensus, with revenue expectations of $22.95B vs the sell side’s estimate of $22.91B. This suggests profit and revenue growth of 44% and 2%, respectively.

What to watch: Judging by how industry peers performed last week, it’s safe to say that Bank of America is in for a good report tomorrow morning. Like other big banks, BofA should have benefited from volatile trading in Q1, rising interest rates, tax reform and a strong underlying economy. The Estimize community anticipates that equity trading revenue and investment banking revenue will be up 6% and 13%, respectively YoY with FICC trading down 2%.

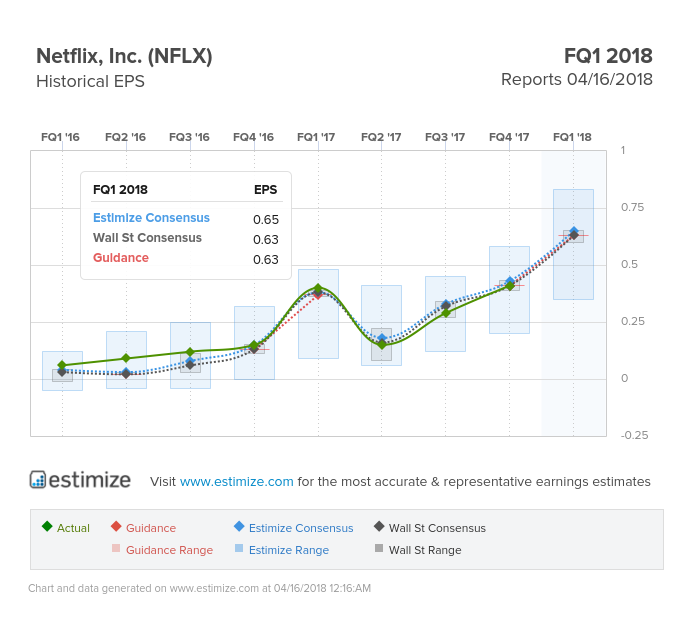

Netflix (NFLX)

Consumer Discretionary - Internet & Catalog Retail | Reports April 16, after the close.

The Estimize consensus calls for EPS of $0.65, two cents higher than the Wall Street consensus, with revenue expectations of $3.7B, in-line with the sell side. This suggests profit and revenue growth of 57% and 40%, respectively.

What to watch: While EPS and revenue will be important to watch when Netflix reports tomorrow afternoon, the metrics that drive the stock are subscriber growth numbers. The Estimize community is predicting that total streaming subscribers (domestic + international) come in at 123.2M, a 25% increase from the year ago number. This would mean total net additions of 5.6M. With a stock price that has continually beaten records this year, the company is going to need to put up good numbers to justify it’s high valuation, and unfortunately for Netflix the first quarter tends to be a bit slower. Investors should looks out for guidance on international subscriber growth as there still seems to be a huge opportunity there.

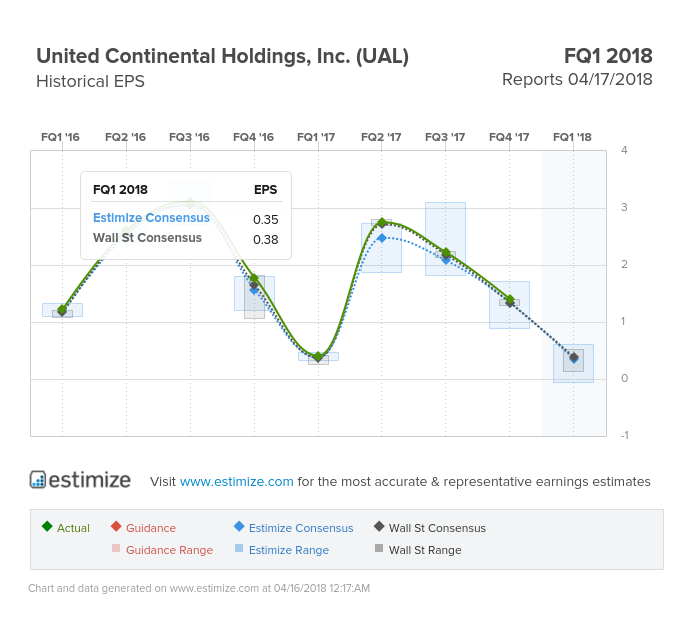

United Continental Airlines (UAL)

Consumer Discretionary - Airlines | Reports April 17, after the close.

The Estimize consensus calls for EPS of $0.35, three cents lower than the Wall Street consensus, with revenue expectations of $22.95B vs the sell side’s expectation of $9.0B. This suggests profit and revenue growth of -7% and 7%, respectively.

What to watch: United will be the second international carrier to report earnings this season, following Delta’s in-line results last week. In addition to EPS and revenue, investors will be looking at the airline’s passenger revenue per available seat mile (PRASM) report which has been reporting negative or only slightly positive YoY growth for the last several quarters. Analysts expect this quarter to be no different, with PRASM only anticipated to rise 1% YoY, but this is up from a prior forecast of 0%, prompted by an increase in guidance that United provided in March. Just last week the airline provided another increase in guidance when it said unit revenue rose 2.7% last quarter and that it’s adjusted pre-tax margin will be closer to 2%.

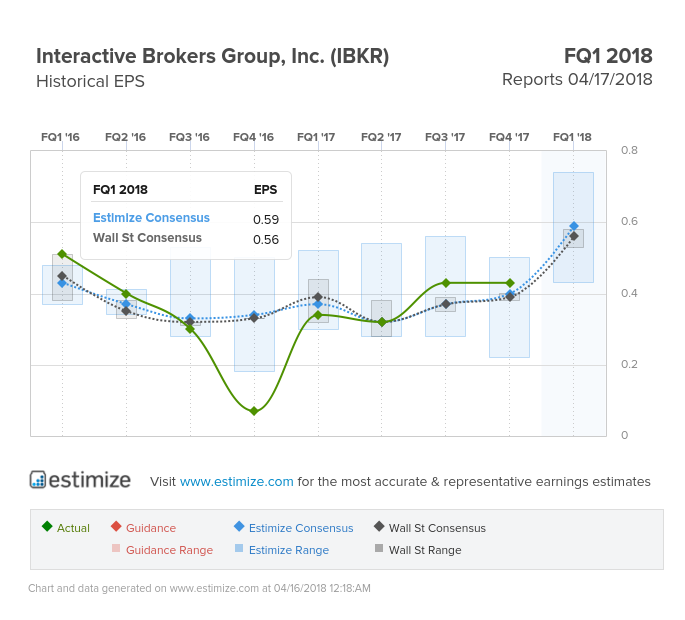

Interactive Brokers (IBKR)

Financials - Consumer Finance | April 17, after the close.

The Estimize consensus calls for EPS of $0.59, three cents higher than the Wall Street consensus, with revenue expectations of $501.4M vs the sell side’s expectation for $477.5M. This suggests profit and revenue growth of 65% and 28%, respectively.

What to watch: For companies set to report this week, Interactive Brokers has one of the highest delta’s between Wall Street estimates and Estimize estimates. That, paired with high expected growth and momentum heading into the report may foreshadow good things come tuesday. Since the company last reported, analysts have raised EPS estimates 34% and revenue estimates by 21%. IBKR recently announced they are shuttering a majority of their Market Making operations in order to focus on the Electronic Brokerage segment which should lead to sustained bottom-line growth in future quarters.

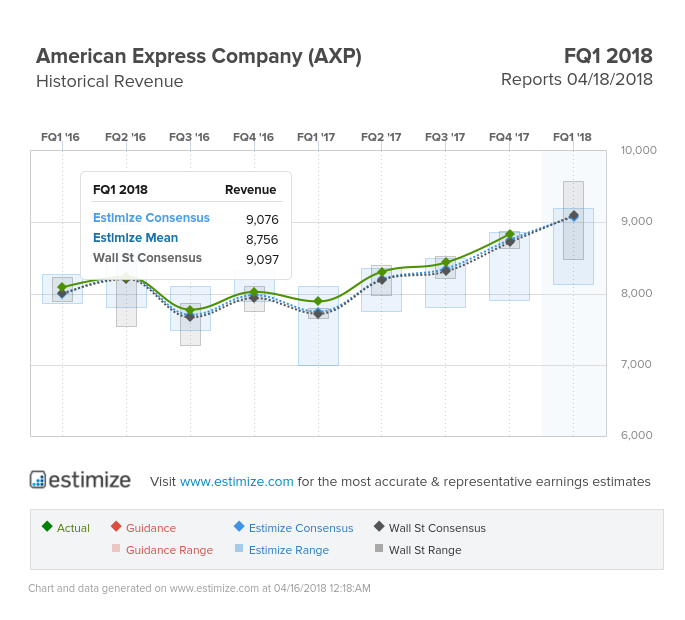

American Express (AXP)

Financials - Consumer Finance | Reports April 18, after the close.

The Estimize consensus calls for EPS of $1.73 and revenues of $9.0, both in-line with the Wall Street consensus. This suggests profit and revenue growth of 29% and 15%, respectively.

What to watch: Amex should continue to benefit from strong consumer sentiment during the first quarter, bolstered by low unemployment and wage growth. The payment processor currently carries a forward 12 month P/E that is below 12, potentially making it a good opportunity going forward.

Disclosure: There can be no assurance that the information we considered is accurate or complete, nor can there be any assurance that our assumptions are correct.