3 Undervalued Gold Miners To Buy On Dips

While most asset classes have started off the year with a strong performance, the Gold Miners Index (GDX) has continued to struggle. As we enter the back half of February, the index is sitting on a (-) 3% year-to-date return, which pales compared to the S&P-500 (SPY), up more than 5% year-to-date. Unfortunately, those hiding out in gold (GLD) haven’t fared much better, with the yellow metal down 4%. The bad news about this weakness in the gold price is that we’ll likely see less margin expansion for the miners next year. However, the good news is that many of these gold miners are already pricing in $1,700/oz and are sporting their most attractive valuations since the COVID-19 Crash lows. In this article, we’ll discuss three names that are paying investors to wait and are trading at very reasonable levels as we head into earnings season:

(Source: TC2000.com)

While the Gold Miners Index has several duds in it, which makes investing in the sector a tricky proposition, there are about ten great names in the index worth owning, that can help diversify a traditional equity portfolio. Prior to 2020, this was not the case as the industry did not offer much earnings growth nor yield, but this has changed with gold solidifying itself above $1,500/oz. In fact, the average million-ounce gold producer is paying a dividend that’s higher than that of the S&P-500, and two names on this list are paying dividend yields above 2.75%. The three stand-out names that are trading at deep discounts are Newmont (NEM), SSR Mining (SSRM), and B2Gold (BTG), with all three being either intermediate or senior gold producers with margins of 50% or higher. NEM is the most compelling for risk-averse investors with a $45BB market cap, a 2.75% yield, and a member of the S&P-500. Let’s take a closer look at all three below:

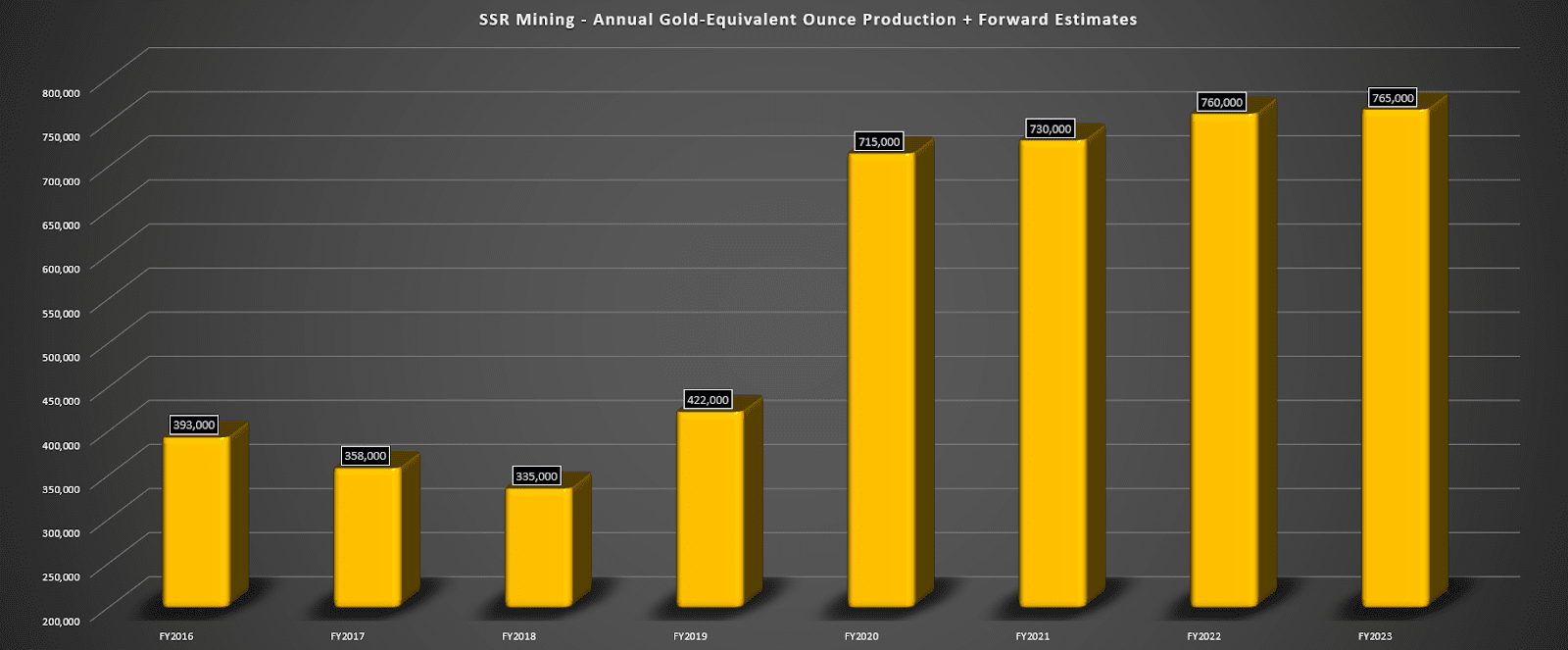

Beginning with SSR Mining, the company was previously mostly focused on Tier-1 jurisdictions, with a Nevada Mine, a mine in Saskatchewan, Canada, and some silver exposure in Argentina at its Puna Mine. However, the company merged with Alacer Gold, a gold producer based out of Turkey, and this has catapulted the company from 400,000-ounce producer status to near 750,000~ ounce producer status.

This significant increase should translate to a re-rating for the stock, with most intermediate and senior gold producers trading at closer to 10x earnings. However, SSR Mining has not received any re-rating, even though its margins have improved considerably with the addition of low-cost Copler operations in Turkey.

(Source: Author’s Chart)

While some investors might not be crazy about the Turkish exposure, it’s worth noting that Alacer Gold operated in Turkey for nearly a decade with no issues. Plus, the Copler Mine is partially owned by a Turkish operator, so there’s no reason for anxiety around the jurisdiction. However, due to perceptions about jurisdictional risk and poor sentiment in the sector, the stock has slid to below $17.00 per share, despite FY2021 annual EPS estimates above $2.30. This translates to a very reasonable multiple of just 7.3x FY2021 annual EPS estimates, and the company also sports a 1.0% dividend yield at current levels. While this discounted valuation doesn’t mean the stock can’t go lower, I see the sub $17.00 level as a low-risk area to start a small position in this mid-cap miner.

(Source: YCharts.com, Author’s Chart)

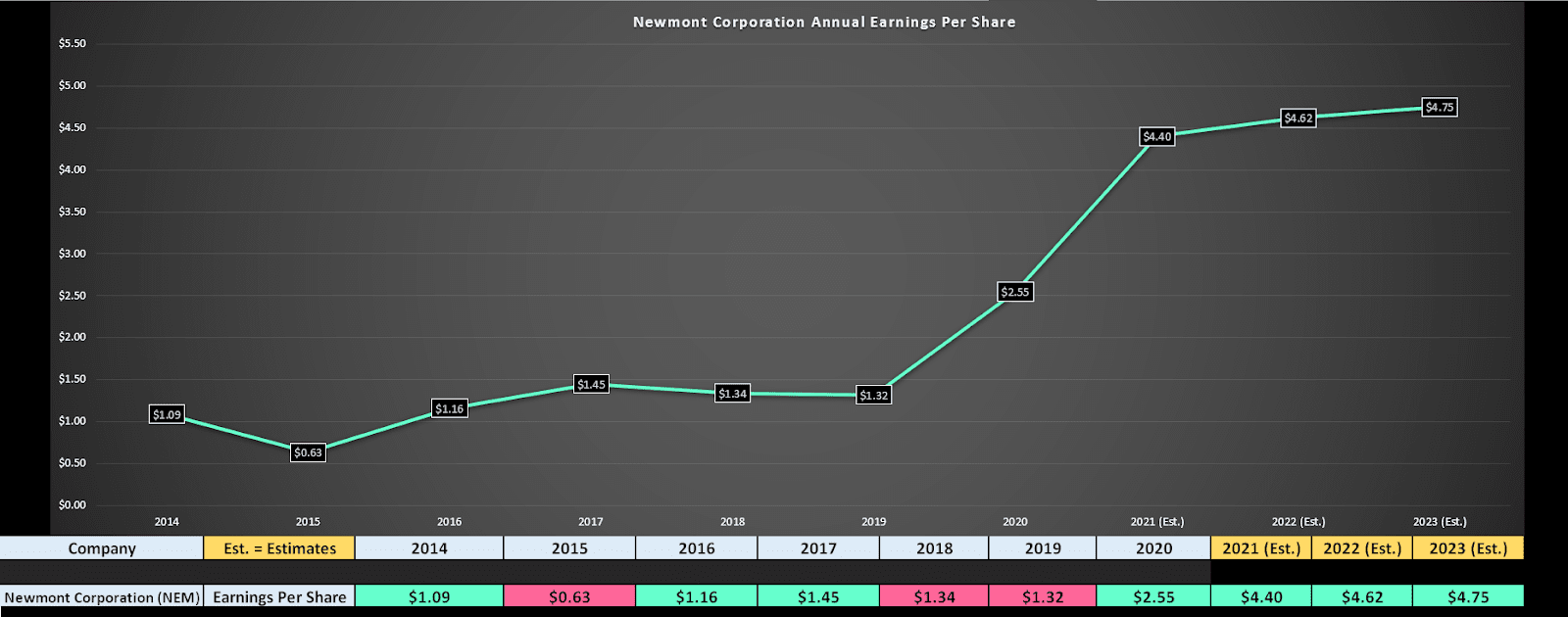

Moving over to the second name on the list, Newmont, we’re also seeing a deep discount relative to prior valuations. Just yesterday, the company announced its updated reserves with more than 94 million ounces of gold in the ground and over 600 million ounces of silver, making it the miner with the largest mineral endowment globally. For investors looking for gold exposure, Newmont offers 117 ounces of gold per 1,000 shares held, which translates to a valuation of over $210,000 vs. the cost of $60,000 to put 1,000 shares. Plus, the stock pays an industry-leading 2.75% yield, which is high even compared with both the S&P-500 and other cyclical industries.

(Source: Author’s Chart)

(Source: Author’s Chart, Company Filings)

Despite a strong report and projections for 70% growth in annual EPS in FY2021, Newmont is trading at barely 13.5x earnings, at a share price of $59.00 with FY2021 annual EPS estimates of $4.40. This is an insane valuation for a stock that typically trades at closer to 18x – 20x earnings, given that it’s the industry-leader with 6 million ounces of annual gold production and the fact that it has a mine life looking out to the 2040s conservatively. Similar to SSR Mining, a poor sentiment in the sector may drag the stock lower, but I have been buying in my long-term accounts to diversify my long-term holdings in broader market equities. At $57.50 per share, where I have been adding, the stock meets my criteria of below 13x earnings and a 2.75% plus yield, and I plan to continue to add on dips. Ultimately, I believe $4.40 in annual EPS is conservative if we can see some momentum return to the gold price later this year.

(Source: YCharts.com, Author’s Chart)

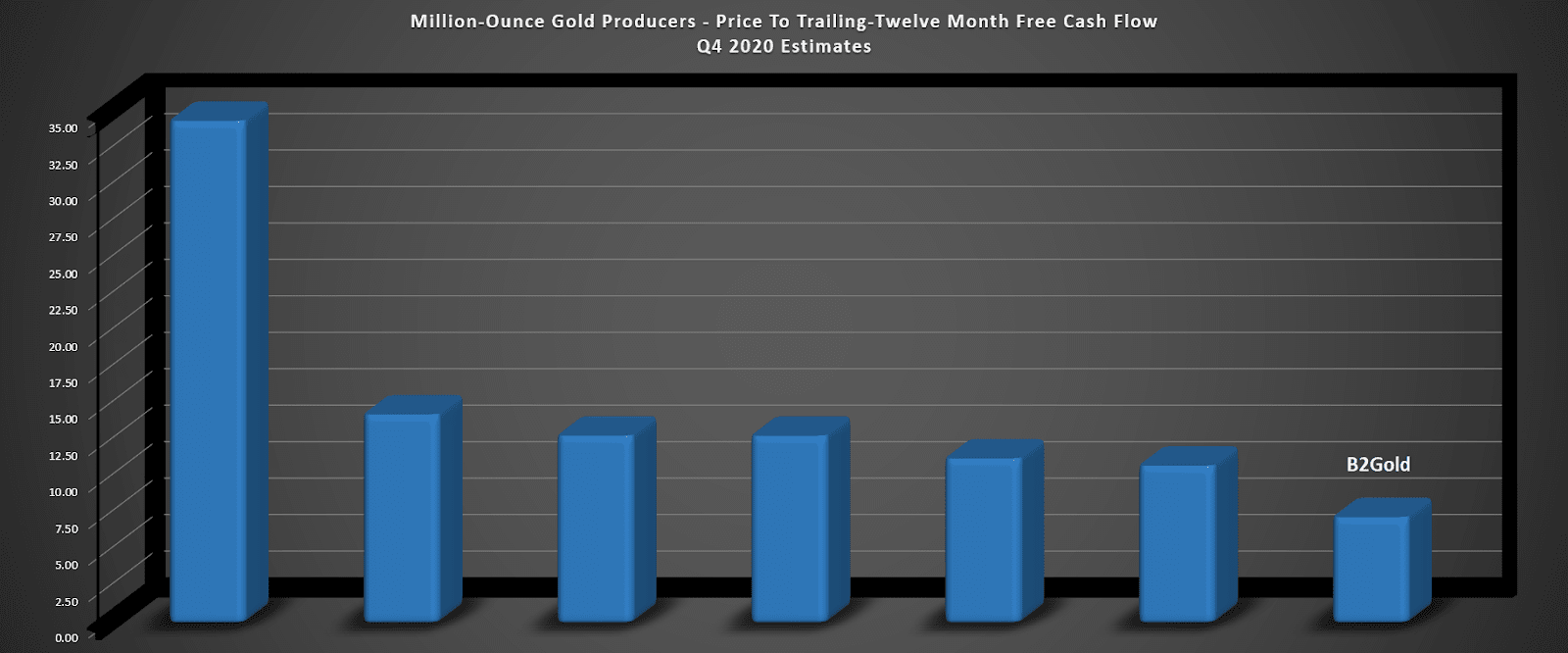

The final name on my list is a little more risky, given that none of its production comes from what I would label Tier-1 jurisdictions. These jurisdictions are defined as Canada, Australia, and the United States, and B2Gold’s production currently comes from Africa and the Philippines. However, the stock is now priced accordingly for this jurisdictional risk, trading at a valuation of barely 8x free-cash-flow and paying a juicy dividend yield of $0.16 per annum. At a share price of $4.95, this translates to one of the top-3 yields in the sector at 3.20%, just ahead of NEM.

(Source: Author’s Chart)

As shown in the chart below, BTG’s annual EPS growth is less exciting than its peers, with annual EPS that’s expected to be relatively flat in FY2021. However, this is coming after a year of double-digit annual EPS growth ($0.50 vs. $0.22), and the stock is currently trading at less than 10x FY2021 annual EPS estimates of $0.52. So, while there are risks to buying producers in less favorable jurisdictions, the stock meets my criteria here for long-term portfolios of below 13x earnings and above a 2.75% yield as well.

(Source: YCharts.com, Author’s Chart)

While there’s several miners in the GDX that I wouldn’t touch with a ten-foot pole, management at SSRM, BTG, and NEM have proven that they can navigate bear markets for the gold price and return significant value to shareholders during bull markets. This is precisely what they’ve been doing since 2016, but poor sentiment has pushed them to valuations that rarely appear outside of bear markets. So, at a time when I believe diversification is key with many equities trading at expensive valuations, I see these three names as one’s to keep at the top of one’s shopping list.

Want More Great Investing Ideas?

9 “MUST OWN” Growth Stocks for 2021

7 Best ETFs for the Next Bull Market

5 WINNING Stocks Chart Patterns

NEM shares were trading at $58.72 per share on Thursday afternoon, down $0.98 (-1.64%). Year-to-date, NEM has declined -1.95%, versus a 4.10% rise in the benchmark S&P 500 index during the same period.

Disclosure: I am long NEM, BTG, GLD

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes ...

more