3-Steps To Holistic Financial Wellness

Investors tend to narrowly define wealth management as portfolios and products. Unfortunately, many financial professionals permit this shortsightedness as it aligns with their aspirations to sell investment vehicles, then move on to the next prospects.

However, this pervasive myopia is a tremendous oversight; investors and financial consumers miss out on the advantages of holistic financial processes and the robust long-term fruitful actions which follow.

We find that people who embrace holistic financial wellness make cogent decisions when it comes to savings rates, debt management, meeting or exceeding financial goals and yes, even portfolio risk management.

If you’re not fortunate enough to partner with a financial professional who can assist with the planning and questions that arise from holistic financial wellness, here are 3 ideas to consider.

First, define financial wellness from the grass roots, on your own terms. Make it personal.

For example, I define financial wellness as a place of security and inner peace; the flow is uneven as stages of wellness ebb and flow along channels of a human existence. It’s never perfect. However, there always exists a strong center or stasis that like a rubber band, snaps back in place after a period of deviation from self-defined financial norms.

In other words, wellness isn’t pretty, but there’s beauty in its consistency. It represents a soup of philosophies, experiences, ego, habits, perceptions and attitudes. Finances bolster with the victories, falter with the setbacks. The challenge is to assess and maintain alignment over time.

You don’t need to be as philosophical as I am about financial wellness. Keep it simple. Do you breathe a bit easier knowing there’s enough cash in an emergency reserve to cover unforeseen expenses? Do you have an active, holistic financial plan in place to realize the impact of a major life change on your wealth? Does the plan include the analysis of current insurance especially disability income coverage and other areas of required risk mitigation like long-term care? Then you’re experiencing financial wellness without even knowing it!

Is portfolio allocation, investment selection part of the equation? Sure, it is. However, it’s one piece of the puzzle. Along with the appropriate mix of stocks, bonds and cash, a portfolio management process should include a discipline to periodically rebalance or return to original asset allocation. In addition, a strategy to decrease stock exposure 3-5 years from retirement is an important consideration.

Ignore common misconceptions about savings, household debt, and the stock market.

Personal finance tenets you’ve heard before – regularly save 10% of take-home pay, diversification is a ‘free lunch,’ stocks always outperform bonds and debt-to-household income ratios of 36% are ‘admirable’, need to be ignored if you want to achieve financial wellness. You must dig deeper.

For example, take an example from the FIRE (Finance Independence Retire Early), crowd who believe that saving 25% of income annually is a more suitable standard. There are many in the FIRE movement who are disciplined enough to sock away 50% a year into a diversified portfolio.

And speaking of diversified…

You must consider portfolio diversification differently to achieve wellness.

According to Investopedia – An internet reference guide on money and investments:

- Diversification strives to smooth out unsystematic risk events in a portfolio so the positive performance of some investments neutralizes the negative performance of others. Therefore, the benefits of diversification hold only if the securities in the portfolio are not perfectly correlated.

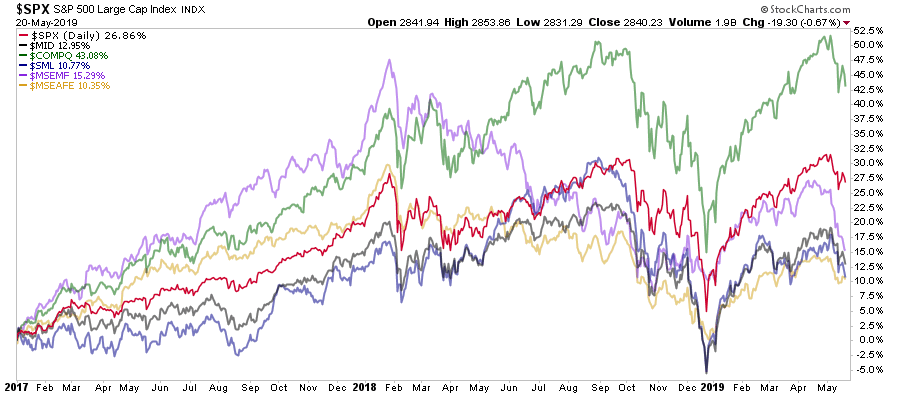

Per Lance Roberts: Diversification is less effective as stock markets have become more correlated (connected) over time.

Now let’s break down the lunch and examine how free it is.

Unsystematic risk – This is the risk the industry seeks to help you manage. It’s the risks related to failure of a specific business or underperformance of an industry.

To wit:

- This is a company- or industry-specific hazard that is inherent in each investment. Unsystematic risk, also known as “nonsystematic risk,” “specific risk,” “diversifiable risk” or “residual risk,” can be reduced through diversification.

- So, by owning stocks in different companies and in different industries, investors will be less affected by an event or decision that has a strong impact on one company, industry or investment type.

While this information is valid, the financial industry encourages you to think of diversification as risk management, which it isn’t.

Here’s what you need to remember:

Ketchup (consumer staples) and oil (consumer cyclicals) all run down-hill, in the same direction in corrections or bear markets.

Sure, ketchup may roll slower, but the direction is the one direction that inhibits wealth – SOUTH.

Large, small, international stocks. Regardless of the risk within different industries, stocks are tightly correlated as Lance outlined in his chart.

So, think about it:

What are the odds of one or two companies in a balanced portfolio to go bust or face an industry-specific hazard at the same time?

What’s the greater risk to you? One company going out of business or underperforming – or your entire stock portfolio suffers losses great enough to change your life, alter your financial plan?

You already know the answer.

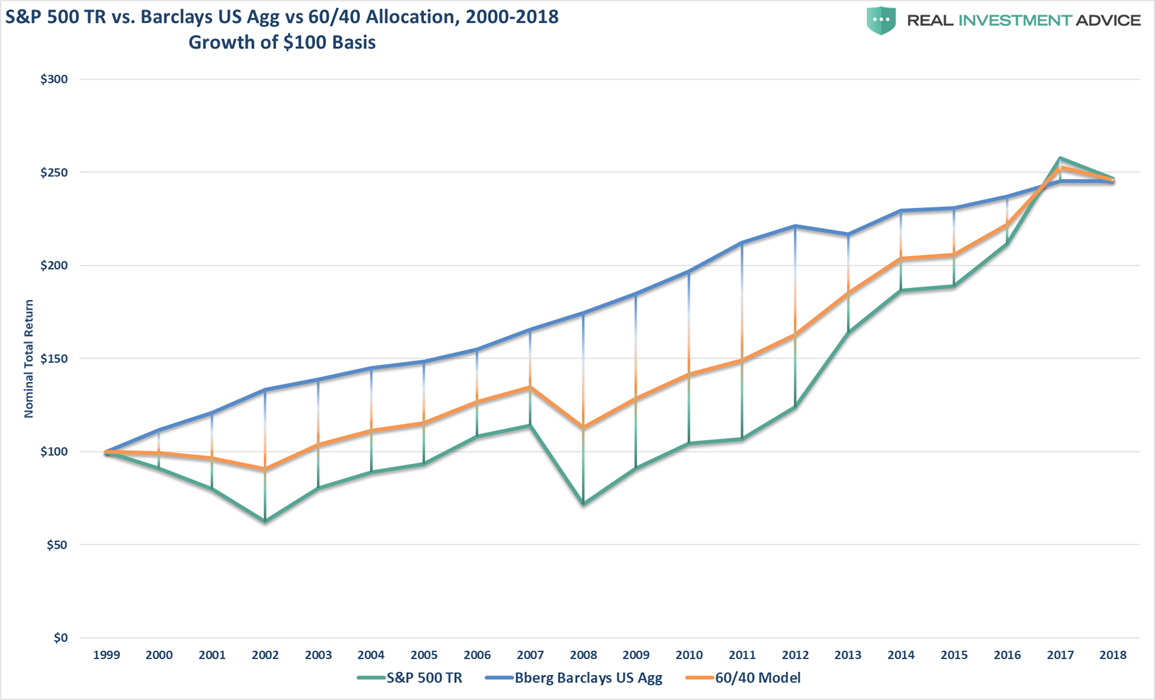

Investors with balanced portfolios over time achieved better risk-adjusted returns than those who bought into stocks exclusively as the solution to every financial shortfall. Bonds remain an important diversifier to a stock portfolio.

To calculate your household’s debt-to-income ratio divide total recurring monthly debt by monthly gross income.

Credit issuers prefer a debt-to-income ratio less than 36%. That’s fine for them; keep in mind a lender’s goal is to cover their asses yet place you into further debt. I’ve heard financial pundits preach this rule as ‘healthy.’ Healthy for whom? Why is this ratio considered healthy? Do not anchor to 36% as a definition for wellness.

My monthly debt-to-income ratio is 15%. It’s a target that defines peace and flexibility for me. Are you able to define then pursue what it takes to live within a ratio which provides financial breathing room? A percentage which generates internal relief and clear thinking derived from what I call ‘financial bandwidth.’ As an example, I’m secure enough to treat my daughter to a summer trip, purchase a shirt when I want it, take care of a veterinary expense – all without the distress of living paycheck to paycheck or wondering how I’m going to handle a financial emergency. That feeling of security is worth more than some ratio a lender deems adequate to pile more debt onto my household balance sheet.

Focus on simple efforts to achieve big results in the future.

Small improvements have potential to forge big mental victories on the path to financial wellness. Since I listen to podcasts and subscribe to Amazon music, I recently made the decision to cancel a Sirius radio subscription. The $120 bucks I’ll pocket annually from the cancellation won’t make or break me. However, the confidence which arises from being proactive bolsters my determination to remain vigilant over money decisions.

Discipline to re-direct discretionary cash into savings (in lieu of spending), ‘brown bagging’ lunch at work, maintaining a budget; even the curb of a daily coffee purchase habit (which doesn’t budge the needle to build wealth), can nonetheless generate feelings of well-being and positively impact future financial decision making.

Financial wellness is achievable; however, it takes thoughtfulness and discipline to set rules and adhere to them. It also takes a dose of healthy skepticism in mainstream financial advice as much of it is designed to serve the industry, not the end users.