2021 Active Management Outlook: Will The Rebound Continue?

Is the active management rebound likely to continue?

In a previous blog post, we emphasized our belief that strong stock picking from multiple differentiated skilled active managers, combined with a disciplined approach to valuation, is an approach well-positioned to continue its recent, strong outcomes. While these types of money managers have benefited greatly from the recent rotation to reopening, the question remains, where can we go from here?

In this post, we take a deeper dive into the gauges we monitor for the active management environment and discuss how this can play out in a well-sourced, risk-managed multi-manager fund. The bottom line is we remain bullish on the opportunity set for skilled stock pickers and their ability to generate excess returns in this environment.

Mean reversion: It’s still a thing

Throughout the late 2010s, active managers faced three major headwinds:

- Unprecedented levels of market concentration

- Low levels of cross-sectional stock volatility

- Higher levels of stock vs. stock correlation

These factors are the main contributors to what some have labeled the Active Management Recession. The onset of the pandemic dramatically increased these headwinds to historic levels. Given the extremes, we expect some level of mean reversion. As the world heals, disciplined money managers are increasingly finding a market that rewards a company’s underlying fundamentals.

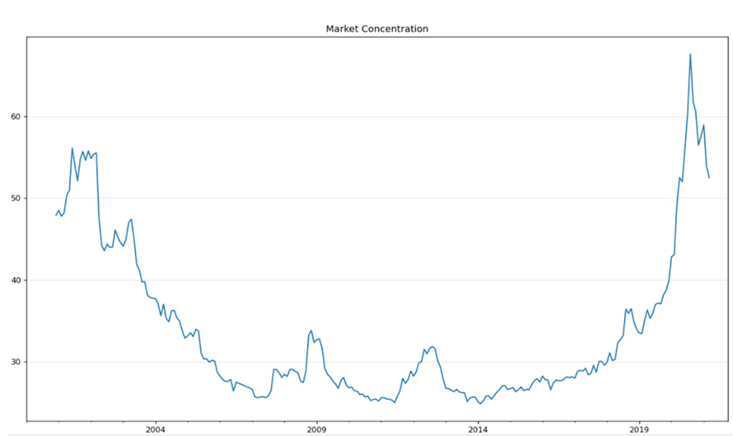

Market concentration

If you didn’t hold exposures to the largest tech names in 2020, you were likely left behind. A limited number of stocks driving markets creates a difficult environment, even for skilled stock pickers. In this case, it was especially difficult for managers with any kind of valuation discipline. The chart below shows just how concentrated markets became in 2020.

Since the first news of effective COVID vaccines came out, concentration has fallen, albeit still at a historically high level. Additionally, we see increasing scrutiny from just about every major government challenging the dominance and monopolistic power these mega cap tech firms exert over just about every stakeholder. We believe this improvement gives active managers an increasingly favorable opportunity to generate excess returns through stock selection, as the breadth of stocks outperforming their benchmarks increases.

(Click on image to enlarge)

Source: Herfindahl-Hirschman Index as of 31 March 2021. Source: Russell Investments, FactSet, MSCI.

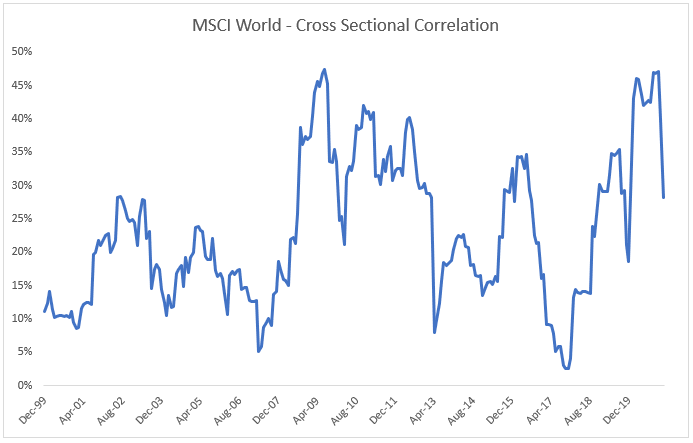

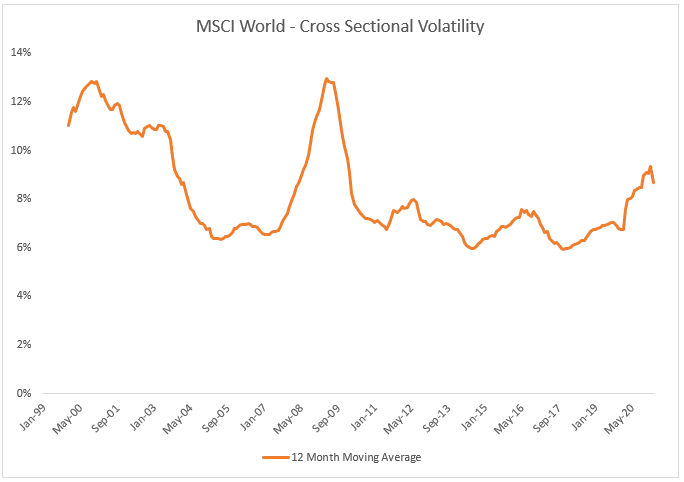

Cross-sectional volatility and cross-sectional correlations

Much like the market concentration chart, trends in cross-sectional volatility and cross-sectional correlations show encouraging signs for active managers. As correlations fall, the breadth of idiosyncratic opportunities increases. And as stock vs. stock volatility rises, the excess return opportunity becomes more pronounced. An environment where cross-sectional correlations are falling and cross-sectional volatility is rising is like a magic quadrant for active managers.

The early 2000s is a great example, with an extended period of low correlations and higher volatility that proved to be a highly effective stock-picking environment. Fast-forwarding to 2021, the gradual return to normalcy has driven both these measures back to a tailwind for active managers. With governments’ aforementioned scrutiny on mega cap tech, renewed commitment to supportive fiscal policy and central banks pledging to remain accommodative for the foreseeable future, we expect this trend to continue.

(Click on image to enlarge)

Source: Russell Investments, MSCI

Note the steady rise in correlations from 2017-2020, which coincides with a particularly challenging period for active managers. The recent drop reflects a market coming out of crisis mode and a return to bottom-up drivers of stock performance.

(Click on image to enlarge)

Source: Russell Investments, MSCI

The trend in cross-sectional volatility is also on a positive trajectory, enhancing return opportunities.

Macroeconomic outlook: More support for stock picking

A key driver for the waning fortunes of stock pickers in the late 2010s and resurgence in the COVID recovery has been interest rates. We have often said that for active management’s fortunes to turn, interest rates don’t need to rise, they just need to stop falling. As economies continue to reopen and spending ramps up, inflation has become a concern. In fact, April’s month-over-month core CPI (consumer price index) inflation increase was the steepest since 1981. U.S. 10-year Treasury yields have risen off all-time lows in 2020 and Americans are sitting on an estimated $2.2 trillion in excess savings. Supply shortages have spread from construction and lumber to technology and semiconductors.

These effects have and will likely continue to feed short-term inflation concerns, which have already resulted in rising 10-year Treasury yields in the U.S. This new environment has had a direct impact on tech names, as growth companies that rely on longer-duration earnings are disproportionately impacted by higher discount rates. Even if this short-term inflationary spike proves transitory, the economic recovery is underway and expected to be prolonged given the strength of consumer balance sheets. In other words, barring another exogenous and unpredictable deflationary shock, don’t expect interest rates to drop anytime soon.

The bottom line

Opportunities become more pronounced when coming from extreme starting points. Valuation spreads, fiscal/monetary policy, and market concentration are all coming off historically elevated levels. These factors, combined with falling cross-sectional correlations and higher-than-average volatility, contribute to our belief that the active management environment has dramatically improved and favors managers’ ability to generate returns through stock selection. Our overall fund positioning is supported by this broad market outlook while remaining broadly diversified through our multi-manager approach.

Disclosures:

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page. The information, analysis, and opinions ...

more